Canadian Monthly Mortgage Report: January 2024

Welcome to January’s nesto-meter report! As the first report of 2024, this month’s nesto-meter not only rounds up December’s numbers but also provides an overview of mortgage and housing market trends in all of 2023.

Key Highlights

- Mortgage Rates: Both fixed rates and variable rates experienced increases over the first three quarters of the year, with the fixed rate starting to decrease for the first time in over a year by the end of September 2023.

- Purchase vs. Renewal vs. Refinance: Renewals lost way to refinances in 2023, as mortgage holders faced payment shock with much higher rates at renewal.

- Purchase Timing Intent: The difference between users who are ‘just looking’ vs those who are ‘ready to buy’ decreased by 10% since the start of 2023, a clear signal that buyers on the sidelines are slowly entering the market.

- Purchase Price & Down Payments: Due to the high-interest rate environment, overall, homebuyers in 2023 shopped at lower price points and put down larger down payments.

Mortgage Rate Trends To Know

While not depicted in the graph below, in the spring of 2022, fixed rates and variable rates switched positions when variable rates increased enough to overtake fixed rates. This switch remained throughout 2023, as both fixed rates and variable rates experienced increases in the first 3 quarters of the year.

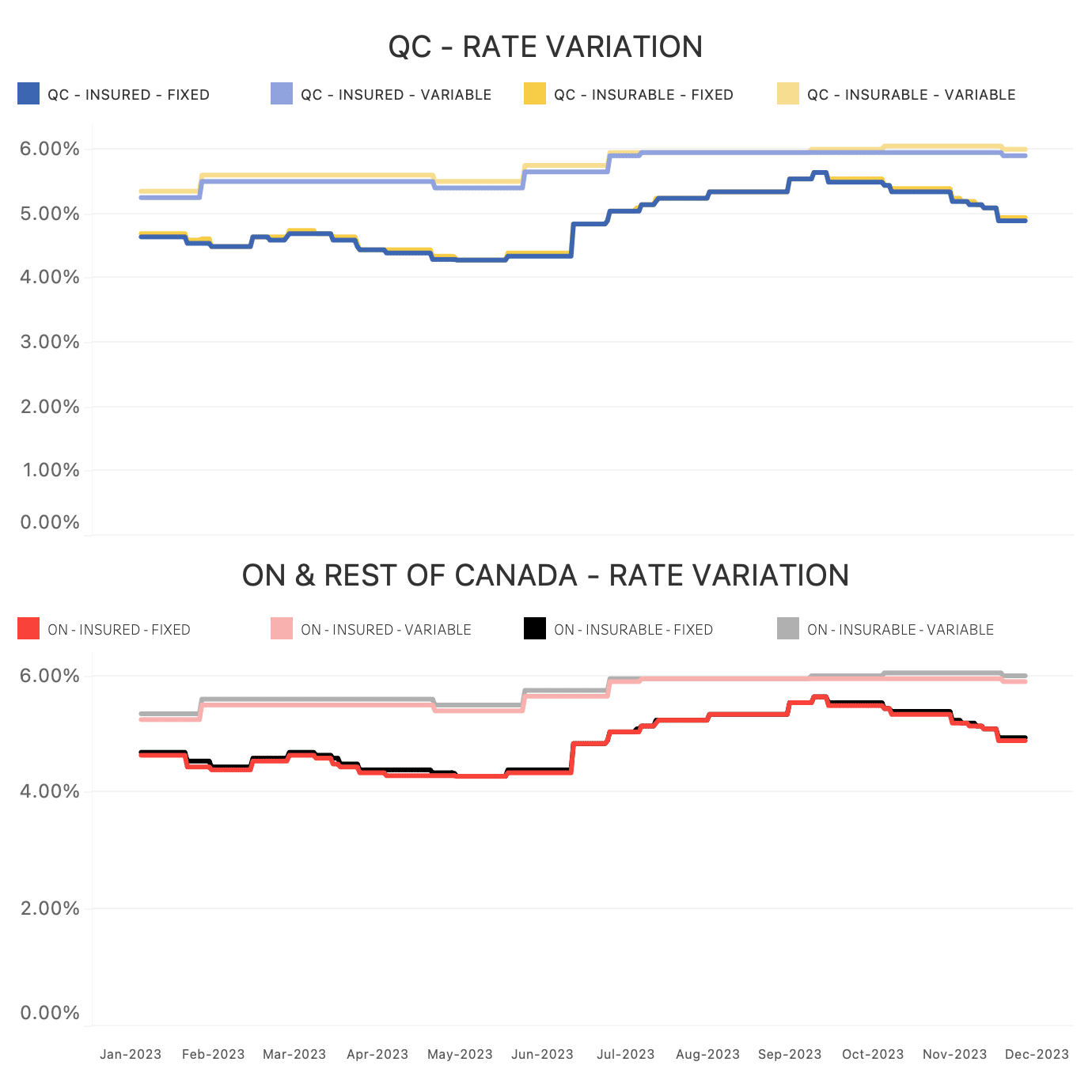

Rate Variation

Fig. 1: These graphs show the rate variances between transaction types in Quebec compared to Ontario and the rest of Canada.

As the Bank of Canada maintained the policy rate over consecutive announcements in the fall, consumer spending continued to reduce, shedding more than half of the inflationary pressures. With this, bond yields started falling in late October, pulling down nesto’s fixed rates. Lower fixed rates further supported affordability by helping borrowers qualify, cementing more home sales in December. If the current mortgage rate trends and home sales continue on this path, we could see a hotter housing market in the summer.

Purchases vs Renewals vs Refinances

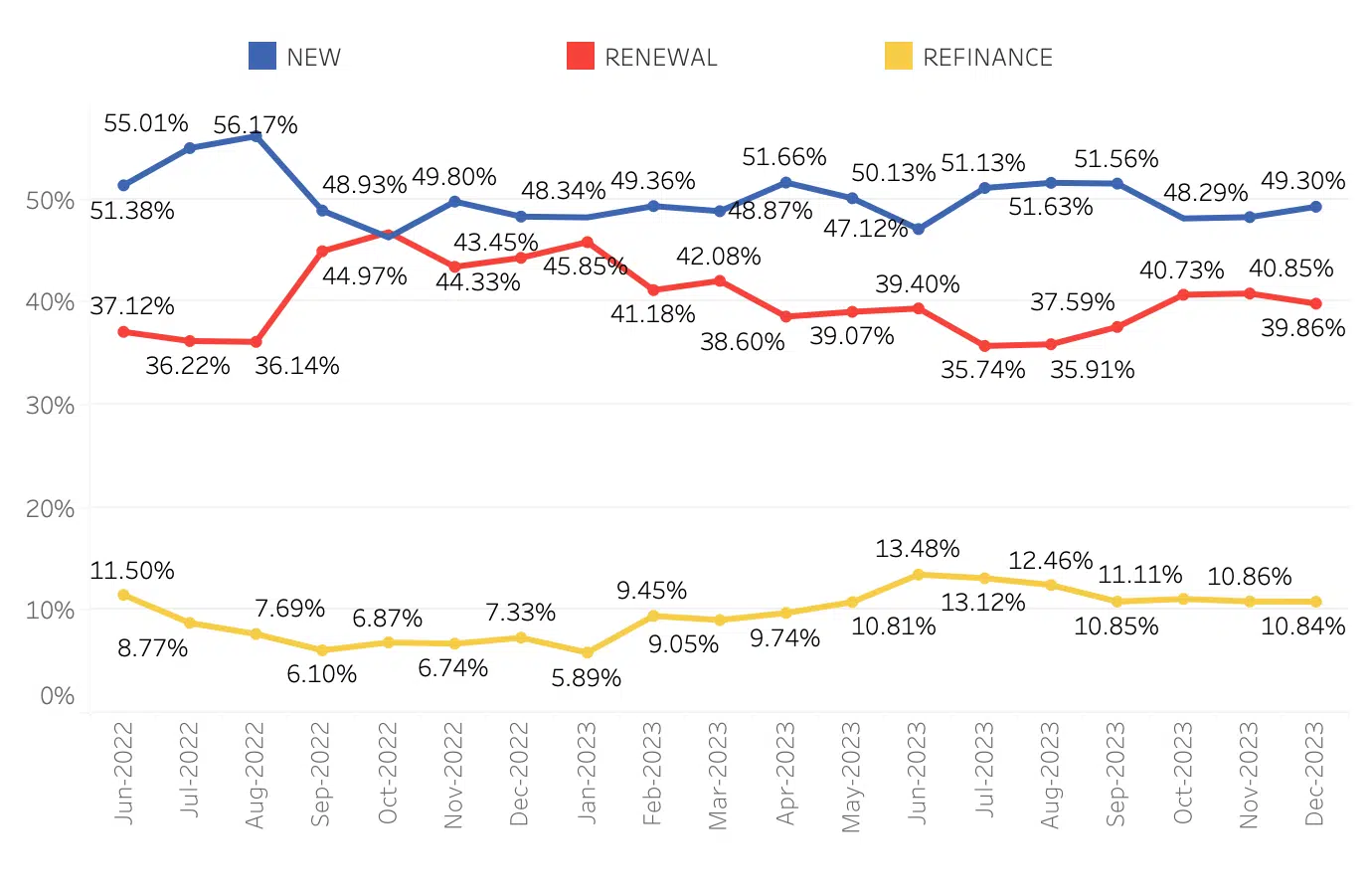

Comparing the portion of new purchases vs the portion of renewals over the course of 2023, we can see the gap between these portions gradually increasing. In January 2023, the portion of new purchases represented 49% of applications, while renewals represented 46%. By the end of the year, in December 2023, new purchases are still at 49%, but renewals have dropped down to 39%. This is in part due to the increasing portion of refinances that has seen slow but steady growth during 2023, going from 6% in January 2023 to 11% in December 2023.

Trends for the Proportion of New Mortgages, Renewals, and Refinances

Fig. 2: Trends for the proportion of purchases (new mortgages) vs. renewals vs. refinances over the last 18 months, from June 2022 to December 2023.

So, why are refinances taking over a portion of renewals? One explanation is payment shock upon renewal, where mortgage holders are faced with much higher rates than when they first got their mortgage. Unable to afford their monthly payments anymore, it’s likely that a refinance was a better financial option for these mortgage holders.

When Is The Best Time To Buy?

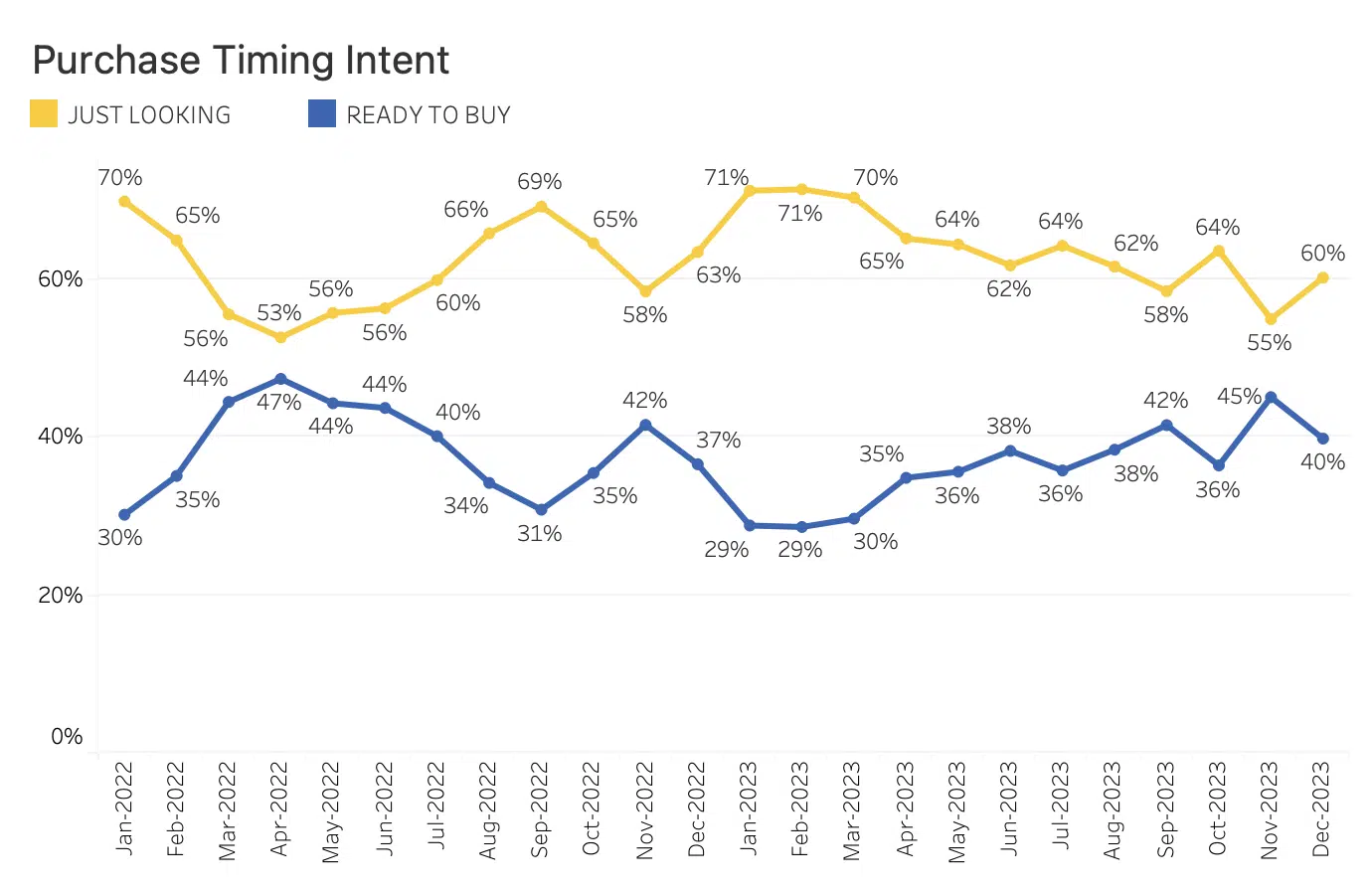

Buyer intent experienced a couple of peaks and valleys over the last 2 years, reaching the most significant gap in January 2023 with 71% of users who were ‘just looking’ and 29% of users who were ‘ready to buy’. However, looking at 2023 with a broader lens, we can note buyer intent stabilizing and trending towards a smaller gap between these two groups.

Purchase Intent: proportion of users “ready to buy” vs. “just looking”

Fig. 3: Purchase intent: proportion of users “ready to buy” vs. “just looking” in their mortgage journey with nesto, illustrated over the last 2 years from January 2022 to December 2023.

In December 2023, buyer intent was split between 60% of users who were ‘just looking’ and 40% of users who were ‘ready to buy,’ a gap 10% narrower than at the start of the year. This is a clear signal that buyers on the sidelines are slowly entering the market as forecasts predict a reduction in the BoC policy rate, which could lead to a resurgence in Canada’s tight housing market. With home prices stabilizing, it’s likely that buyers are seeing this as the most opportune time to take advantage of lower prices before the spring.

Best Mortgage Rates

Home Prices And Down Payments

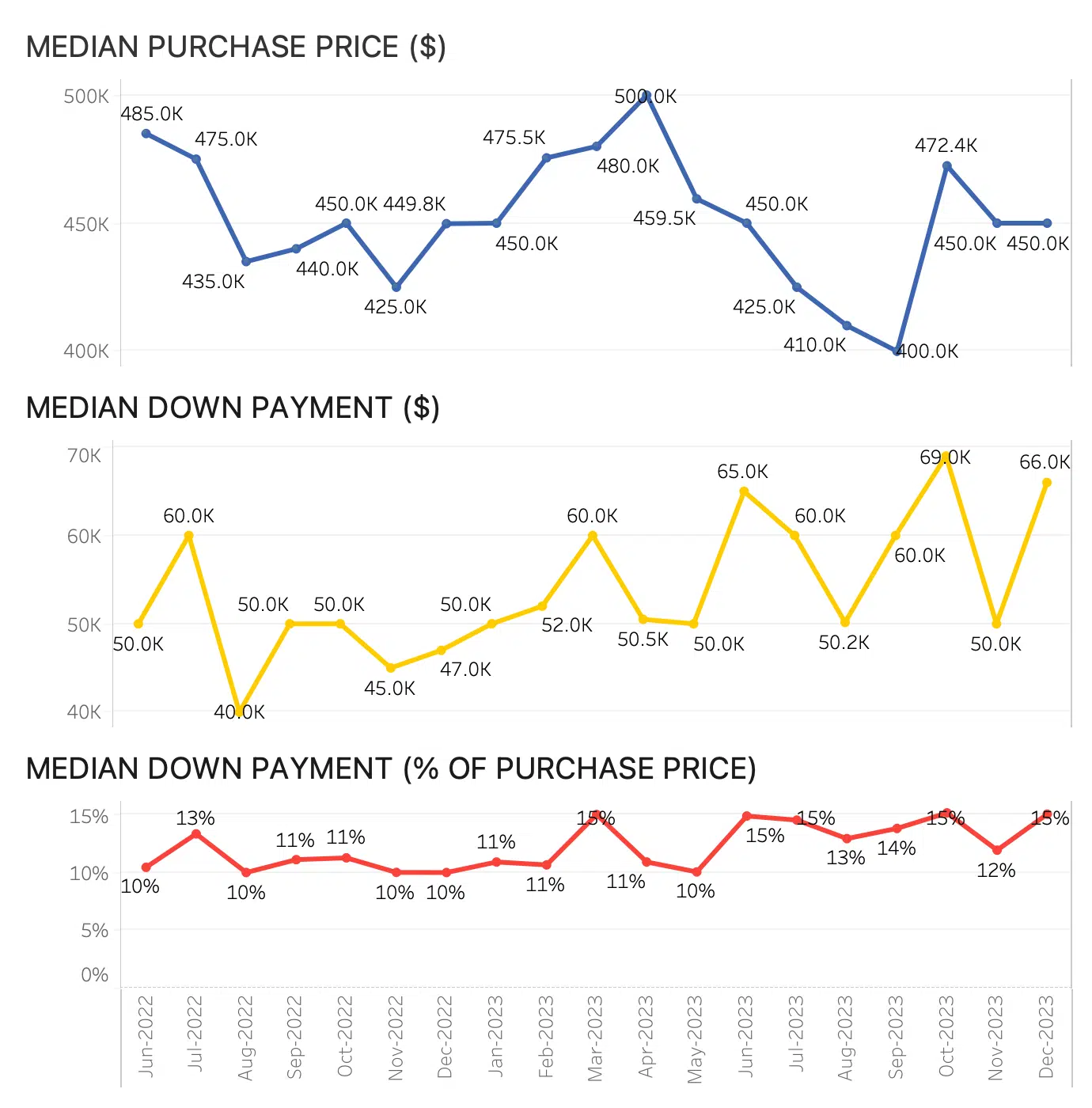

Earlier in 2023, our previous monthly reports noted how homebuyers were shopping for the absolute lowest prices while contributing larger down payments. The high interest rate environment continues to reduce affordability, leaving buyers with lower qualifying mortgage amounts.

Median Purchase Price and Median Down Payment in Canada

Fig. 4: Median purchase price and median down payment values over the last 2 years in Canada between January 2022 and December 2023.

However, later in the year, we saw purchase prices pick up again, along with down payment amounts. This is in line with the above buyer intent data, signalling a shift in purchase intent as buyer hesitance finally begins to wane.

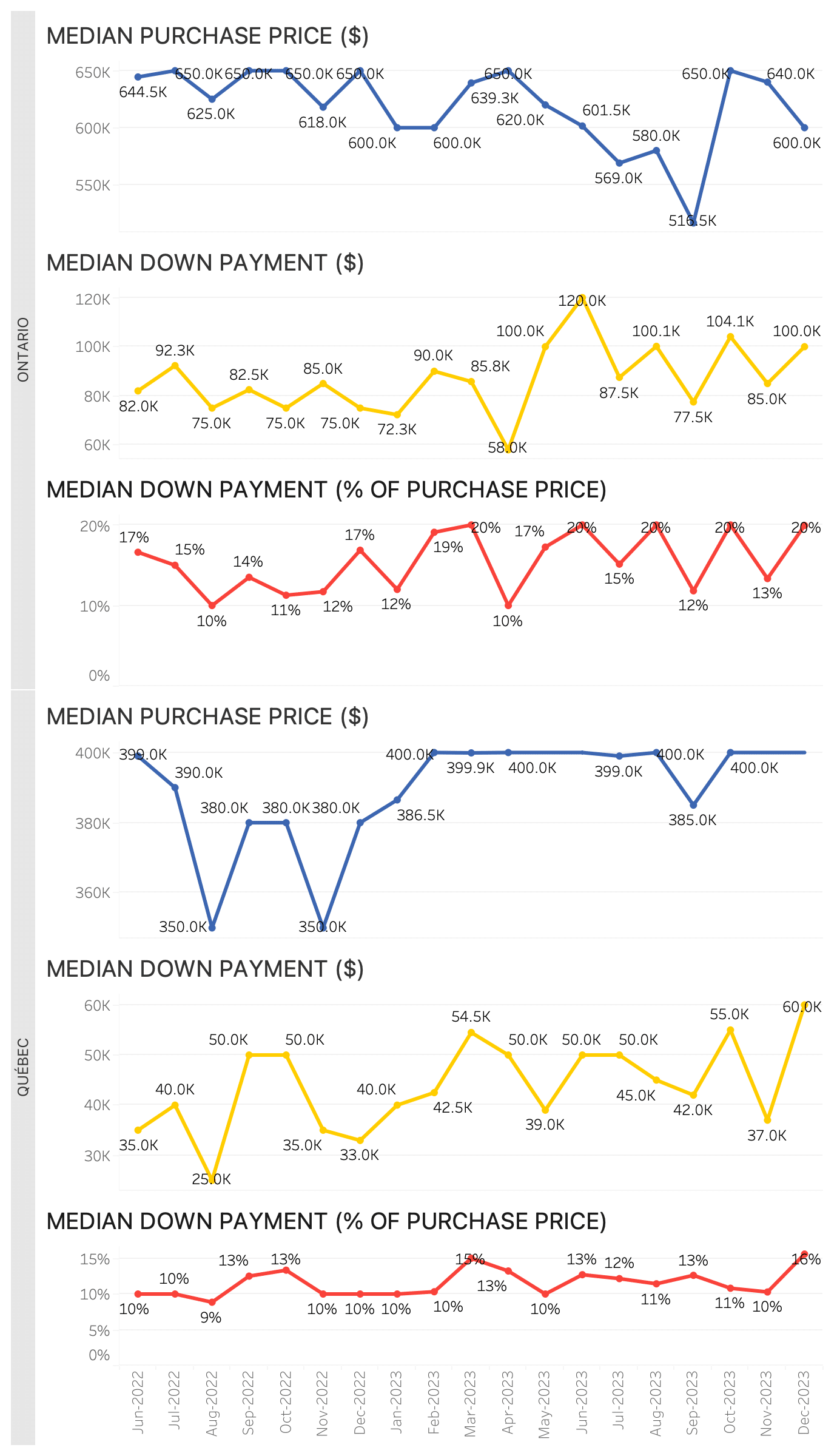

Quebec and Ontario

Fig. 5: Median purchase price and median down payment values in Ontario and Quebec over the last 2 years, between January 2022 and December 2023.

Like the national data, Ontario’s median purchase price was trending down earlier in 2023, only to recover later in the last quarter. In turn, median down payments continued to increase, as Ontario buyers (much like most of Canada) were contributing larger down payments on cheaper houses in order to mitigate unaffordability.

On the other hand, the median purchase price in Quebec remained relatively stable for most of 2023, while we can note an increasing trend in down payment value. This difference can be explained by the lower home prices in Quebec compared to Ontario.

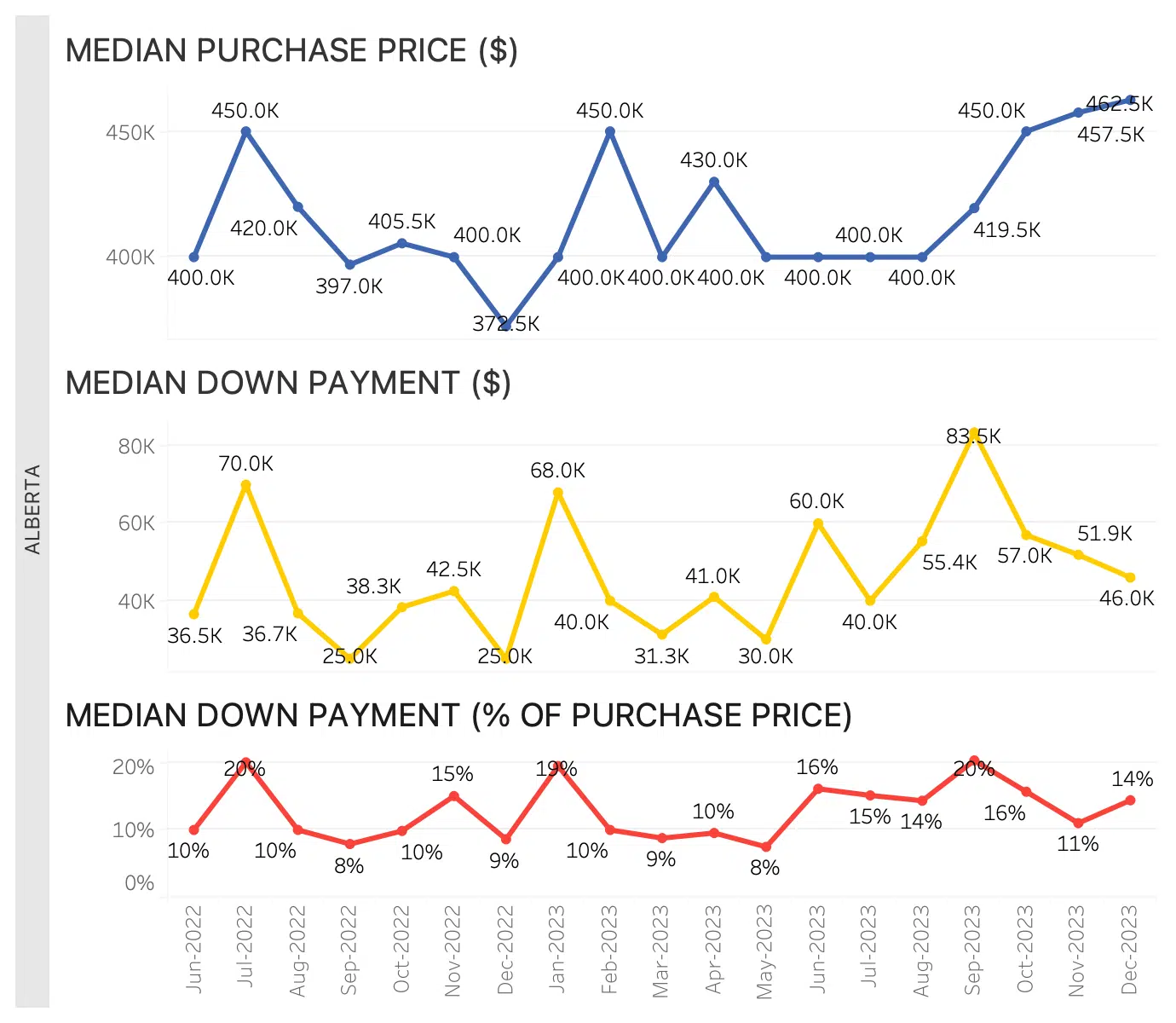

Alberta

Fig. 6: Median purchase price and median down payment values in Alberta over the last 2 years, between January 2022 and December 2023.

In contrast, Alberta’s home buying trends moved in the opposite direction in 2023, with both median purchase price and median down payment gradually increasing. When compared to the rest of Canada, housing affordability was in much better shape in Alberta in 2023. We surmise this contrast between buyers in Alberta and other parts of Canada is likely due to a tighter market as more Canadians continue to move to Alberta.

Final Thoughts

The numbers from the last quarter of 2023 serve as a preview of what the 2024 market is going to look like. As the Canadian economy slowly continues to recover from the high interest rate environment of the past 20 months or so, it’s clear that buyers on the sidelines are gearing up to enter the market in 2024. With talks of potential rate cuts and an overall decrease in home prices, it’s no surprise that buyers are returning to the market.

Best Mortgage Rates