Bank of Canada Maintains the Policy Rate at 2.25%

Mortgage Affordability Calculator Canada

How Much Mortgage Can I Afford in Canada

A borrower in Canada can generally afford a mortgage between 3.5 and 4.5 times their gross annual household income, assuming minimal existing debt. Lenders cap housing costs at 35% to 39% of gross income through the gross debt service (GDS) ratio, and total debt payments at 42% to 44% of gross income through the total debt service (TDS) ratio. All borrowers must also qualify under the federal mortgage stress test, which uses the higher of 5.25% or the contract rate plus 2%.

Mortgage Affordability Calculator

What Is Mortgage Affordability?

One of the first steps in searching for a home is figuring out how much mortgage you can afford. This is known as mortgage affordability.

Mortgage affordability represents the maximum mortgage and the corresponding property you can afford when including your down payment. Mortgage affordability is primarily based on your income, monthly expenses, and home-ownership expenses. Assessing your capacity to afford a home is an essential step in the qualifying process, as it clarifies whether you can comfortably afford your mortgage payments.

The easiest way to determine your capacity to carry a mortgage, and the maximum home price for which you qualify, is through nesto’s Mortgage Affordability Calculator.

How Much Mortgage Can I Afford in Canada?

In Canada, you can typically afford a mortgage between 3.5 and 4.5 times your gross annual household income, assuming minimal existing debt. A household earning $100,000 with no other debts usually qualifies for a mortgage of roughly $350,000 to $450,000. The exact number depends on your down payment, property taxes, heating costs, credit score, and whether your mortgage is insured or uninsured.

Lenders use two ratios to set your maximum mortgage: gross debt service (GDS), which caps your housing costs at 35% to 39% of your gross income, and total debt service (TDS), which caps all your debt payments at 42% to 44%. You also have to qualify under the federal mortgage stress test, which uses the higher of 5.25% or your contract rate plus 2%.

For a more exact number based on your specific situation, use nesto’s Mortgage Affordability Calculator below. It applies current lending rules automatically, including the stress test, GDS and TDS limits, and minimum down payment requirements.

How Much Mortgage Can I Afford With 20% Down in Canada?

With 20% down, your mortgage is uninsured, which means no CMHC premium but slightly tighter qualification. Most lenders cap gross debt service at 35% and total debt service at 42%. For example, a household earning $120,000 a year with no other debts and 20% down can typically afford a home in the $550,000 to $650,000 range, depending on property taxes and heating costs.

The benefit of going with 20% down is twofold: you skip the mortgage default insurance premium (which can add 2.8% to 4% to your mortgage), and you unlock longer amortizations of up to 30 years on an uninsured mortgage. The trade-off is that your maximum mortgage depends more heavily on your income, existing debt, and stress test qualification, since lenders apply stricter ratio limits without the backing of a mortgage insurer.

How Much Mortgage Can I Afford With 5% Down in Canada?

With 5% down, your mortgage must be insured through CMHC, Sagen, or Canada Guaranty. Insured mortgages allow gross debt service up to 39% and total debt service up to 44%, which means you can typically qualify for a larger mortgage than with the same income at 20% down. For example, a household earning $100,000 with no other debts and 5% down can usually qualify for a home priced between $450,000 and $500,000.

The minimum down payment is 5% on the first $500,000 of the purchase price and 10% on the portion above, up to a home value of $1.5 million. A $500,000 home requires a $25,000 down payment. A $750,000 home requires a $50,000 down payment ($25,000 on the first $500,000 and $25,000 on the remaining $250,000). You must also qualify under the federal mortgage stress test at the higher of 5.25% or your contract rate plus 2%, and you’ll pay a mortgage default insurance premium of 2.8% to 4% of the mortgage amount.

Canada Mortgage Affordability Rule of Thumb

A common rule of thumb suggests you can afford a mortgage 3.5 to 4.5 times your gross annual income, assuming minimal debt. This estimate changes based on property taxes, heating costs, condo fees, interest rates, and the mortgage stress test.

Best Mortgage Rates

How to Calculate Mortgage Affordability in Canada

Mortgage affordability in Canada is calculated using your gross income, monthly debt obligations, property taxes, heating costs, and down payment. Lenders apply gross debt service and total debt service ratios, and you must qualify under the federal mortgage stress test at the higher of 5.25% or your contract rate plus 2%.

nesto’s Mortgage Affordability Calculator applies these same qualification rules automatically. Enter your income, debts, property details, and down payment to see the maximum mortgage amount you may qualify for under current Canadian lending guidelines.

How Lenders Calculate Mortgage Affordability

Lenders determine how much mortgage you can afford using two core ratios:

• gross debt service (GDS)

• total debt service (TDS)

GDS measures the percentage of your gross income required to cover housing costs, including mortgage payments, property taxes, heating, and 50% of condo fees if applicable.

TDS measures the percentage of your gross income required to cover all debts, including housing costs, credit card debt, loans, and other obligations.

For insured mortgages with 5% down, lenders may allow up to 39% GDS and 44% TDS. For uninsured mortgages with 20% down, lenders typically apply stricter limits of 35% GDS and 42% TDS.

Gross Debt Service (GDS) Ratio

The gross debt service ratio measures the percentage of your gross income required to cover housing costs.

Housing costs include:

• Mortgage principal and interest

• Property taxes

• Heating costs

• 50% of condominium fees (if applicable)

Formula

GDS = (Mortgage Payment + Property Taxes + Heating + 50% Condo Fees) ÷ Gross Income

Qualification Limits

• Insured mortgages under 20% down: up to 39% GDS

• Uninsured mortgages 20% down or more: typically around 35% GDS

Total Debt Service (TDS) Ratio

The total debt service (TDS) ratio measures the percentage of your gross income required to cover all debts.

Total debts include housing costs plus:

• Credit cards

• Car loans

• Lines of credit

• Personal loans

• Spousal or child support payments

Formula

TDS = (All Housing Costs + All Other Monthly Debts) ÷ Gross Income

Qualification Limits

• Insured mortgages: up to 44% TDS

• Uninsured mortgages: typically around 42% TDS

Affordability Limits: 5% vs 20% Down Payment

| Feature | 5% to 19.99% Down (Insured) | 20% Down or More (Uninsured) |

|---|---|---|

| Max GDS Ratio | 39% of Gross Income | 35% to 39% (Lender dependent) |

| Max TDS Ratio | 44% of Gross Income | 42% to 44% (Lender dependent) |

| Max Amortization | 25 Years (30 for FTHB or New Builds) | 30 Years |

| Stress Test Rate | Higher of 5.25% or Rate + 2% | Higher of 5.25% or Rate + 2% |

| Price Cap | Max $1,500,000 | No Government Limit |

How the Mortgage Stress Test Affects Your Result

All federally regulated lenders must qualify borrowers at the higher of 5.25% or the contract rate plus 2%.

This means even if your actual interest rate is lower, your affordability is calculated using a higher qualifying rate. The stress test protects borrowers from future rate increases and often reduces the maximum mortgage amount you can qualify for.

In practice, most borrowers today are stress-tested at their contract rate plus 2%, because that number is higher than the 5.25% floor. The 5.25% benchmark only becomes the binding rate when mortgage rates fall below 3.25%, which is becoming rarer in the current environment.

“According to OSFI’s 2026 guidelines, the minimum qualifying rate for uninsured mortgages remains the greater of the mortgage contract rate plus 2% or a floor of 5.25%. This ensures borrowers can maintain payments if interest rates rise.” — Office of the Superintendent of Financial Institutions (OSFI)

As of July 28, 2026, nesto’s 5-year fixed insured rate is 4.09%. The stress-tested qualifying rate would therefore be [fixed_insured_q]. Your qualifying income is calculated against this higher rate, not the contract rate you’d actually be paying.

What Mortgage Can I Afford by Income?

These estimates use an insured mortgage with 5% down, a 25-year amortization, and standard GDS and TDS limits. Your actual qualifying amount will vary based on property taxes, heating costs, credit score, and existing debts.

- Gross household income of $60,000: roughly $225,000 to $275,000 mortgage

- Gross household income of $80,000: roughly $300,000 to $375,000 mortgage

- Gross household income of $100,000: roughly $350,000 to $450,000 mortgage

- Gross household income of $150,000: roughly $550,000 to $680,000 mortgage

- Gross household income of $200,000: roughly $750,000 to $900,000 mortgage

For detailed breakdowns by mortgage size, see nesto’s guides on the income needed to qualify for a $400,000 mortgage, $500,000 mortgage, or $1 million mortgage in Canada.

Income Used to Qualify for a Mortgage

Income is the foundation of your mortgage affordability calculation. Lenders will verify stable income and apply specific underwriting rules based on the type of earnings.

Employment Income

Your guaranteed hours are used for qualification. If you are a permanent part-time employee, lenders use guaranteed hours confirmed in your Letter of Employment. If you have non-permanent or variable hours, most lenders use a 2-year average of your T4 income. If income on your T4s shows a decline year over year, lenders generally use the lower-earning year rather than the 2-year average.

Below is how to convert hourly income properly for qualification purposes:

| Hourly Rate | Number of Hours | Formula | Example |

|---|---|---|---|

| Weekly | 35, 40, or 44 hours as guaranteed every week | $/hr x weekly hours guaranteed | $15/hr x 35 hrs/wk = $525 weekly |

| Biweekly | Twice that of weekly | $/hr x 2 x weekly hours guaranteed | $15/hr x 2 x 35 hrs/wk = $1050 biweekly |

| Monthly | Weekly hours multiplied by 52 divided by 12 | $/hr x weekly hours guaranteed x 52 weeks in a year / 12 months | $15/hr x 35 hrs/wk x 52 wks / 12 months = $2275.05 monthly |

| Annually | Weekly hours multiplied by 52 | $/hr x weekly hours guaranteed x 52 weeks in a year | $15/hr x 35 hrs/wk x 52 wks = $27,300.60 annually |

Being precise matters. Overstating income can distort affordability results and lead to declined approvals later.

Bonus Income

Bonus income is added to your base salary when calculating your total qualifying income, but lenders usually require a 2-year history and will average the amounts you receive.

If your bonus income is consistent or increasing, lenders typically use the 2-year average. If total income is declining, most lenders use the lower year to remain conservative.

Example

Base salary: $50,000

Year 1 total income with bonus: $65,000

Year 2 total income with bonus: $60,000

2-year average total income: $62,500

Since income declined in Year 2, most lenders would qualify you using $60,000 instead of the average.

Self-Employed Income

If you are a sole proprietor or incorporated, lenders typically average 2 years of declared income from your T1 General and Notices of Assessment. Taxes owed to the Canada Revenue Agency must be paid in full before the mortgage commitment.

Other Income Types

The following income types may be used if documented properly and stable:

• Child or spousal support with deposit history

• Canada Child Benefit federal portion

• Canada Pension Plan

• Old Age Security

• Employer/Disability pension

• Investment income with sustainability verification

Rules vary by lender, and documentation is required to confirm stability.

Property Taxes

Property taxes are included in your GDS calculation.

For purchases, use the MLS listing or the current tax bill.

For new builds, lenders estimate between 0.50% and 1.3% of the purchase price, depending on the municipality and province.

For renewals, refinances, or private sales, use the most recent municipal property tax bill.

Higher property taxes reduce your maximum mortgage qualification.

Heating Costs

Heating costs are included in GDS.

For condos and homes up to 2,000 square feet, most lenders estimate $100 per month. Larger homes may require higher estimates.

Condominium Fees

50% of condo fees are included in your GDS ratio. Fees must be verified through the MLS, condo status certificate, or bank statements.

Higher condo fees reduce the mortgage amount you can qualify for.

Home Value

For purchases, use the purchase price.

For renewals or refinances, use a conservative estimate or municipal assessment value.

Home value determines your loan-to-value (LTV) ratio, which affects whether your mortgage is insured or uninsured.

Down Payment

Minimum down payment rules in Canada:

• 5% minimum for properties under $1.5 million (5% on the first $500,000 and 10% on the rest)

• 20% minimum for properties $1.5 million and above

With 5% down, your mortgage must be insured, which allows slightly higher debt ratios.

With 20% down, you avoid mortgage insurance premiums, but lenders may apply stricter qualification ratios.

Mortgage Interest Rate

Your interest rate affects both your monthly payment and your stress test qualification.

Fixed mortgage rates are influenced by bond yields.

Variable mortgage rates are influenced by the Bank of Canada’s policy rate.

Your minimum qualifying rate (MQR) will be the higher of 5.25% (the benchmark rate) and your contract rate plus 2%.

Mortgage Term

Fixed terms range from 1 to 10 years. Variable terms are typically limited to 3 and 5 years.

Term selection affects your interest rate but does not change your amortization.

Amortization

For purchases with less than 20% down, maximum amortization is 25 years.

For purchases and refinances with 20% or more down payment or equity, amortization may extend up to 30 years.

Longer amortization lowers payments but increases total interest paid and may affect qualification thresholds.

Exceptions apply for first-time homebuyers (FTHB) and those purchasing newly built homes, allowing up to 30-year amortizations with as little as 5% down on the first $500,000 of the purchase price and 10% down on the rest. For insured mortgages, borrowers are limited to a maximum home purchase price of $1.5 million, or less.

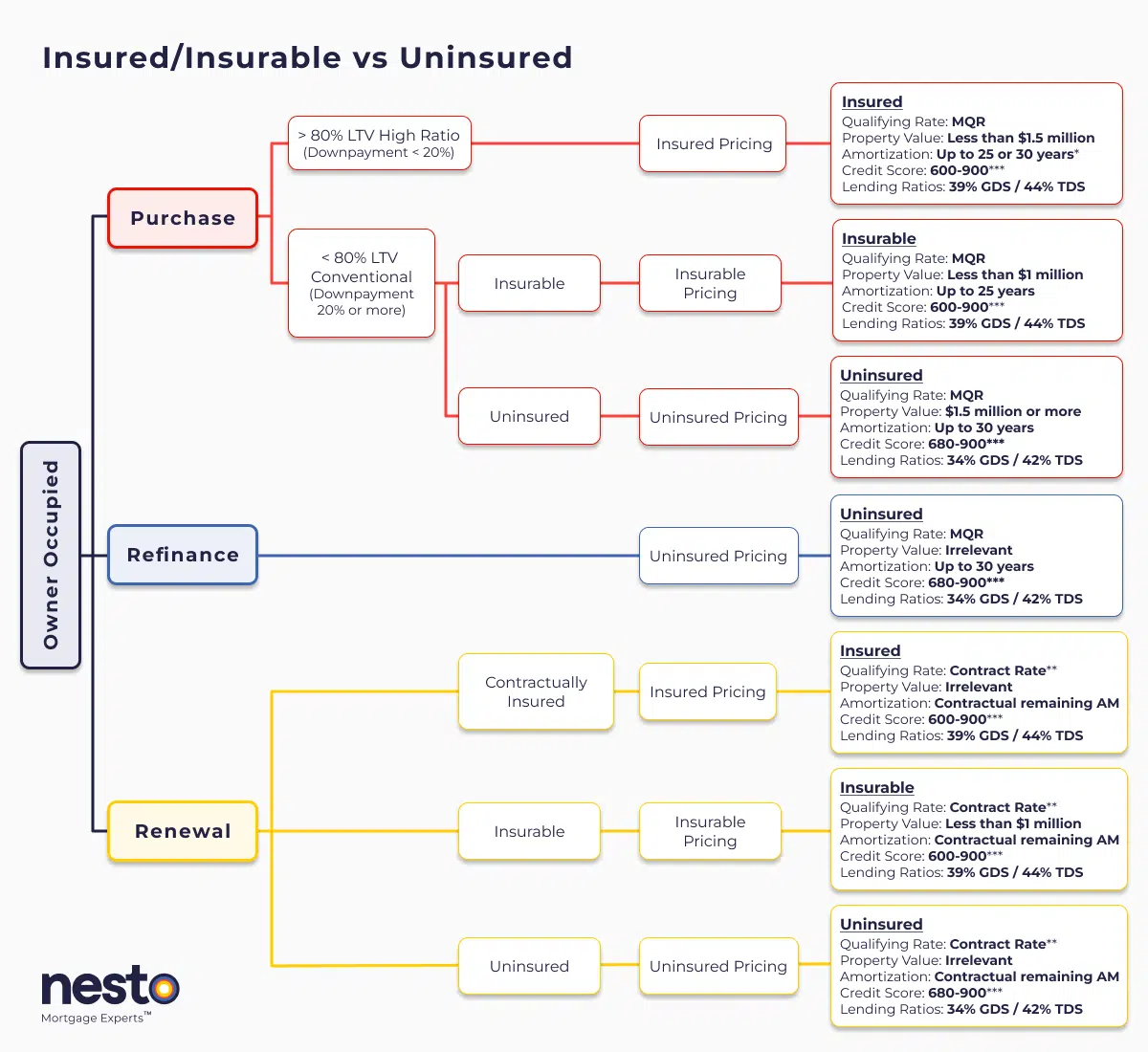

Qualifying Requirements for Insured vs. Insurable vs. Uninsured Mortgages

Insured, insurable, and uninsured mortgages in Canada each have different qualifying requirements, ratio limits, and rate treatments. Insured mortgages (less than 20% down) offer the most flexible ratios but require a CMHC, Sagen, or Canada Guaranty premium. Insurable mortgages (20% or more down, property under $1.5M, 25-year amortization) are bulk-insured by the lender and usually get the best rates. Uninsured mortgages (20% or more down, or any refinance) carry slightly tighter ratios because the lender absorbs all the risk.

Details

*30-year amortizations on insured purchases are limited to first-time homebuyers (FTHBs) or anyone purchasing newly built homes.

**Qualified at contract rate at renewal only if there are no increases to contractually remaining amortization or remaining balance, and the mortgage is being transferred from a federally regulated lender as outlined by the Department of Finance (DOF) as a straight switch. The minimum qualifying rate (MQR) requirements have been amended by the Office of the Superintendent for Financial Institutions (OSFI). It will be used to qualify all mortgages used for purchases and refinances. The MQR does not apply to renewals if the mortgage is renewed with the current lender or if it is switched from a federally regulated lender. In today’s rate environment, your contract rate plus 2% is the binding qualifying rate for almost all borrowers. The 5.25% OSFI floor only becomes binding if mortgage rates fall below 3.25%, which is rare in the current market.

***A credit score of 600 or 650 is allowable based on the mortgage insurer, and if there is a secondary applicant with a credit score of 680 or above. Lenders may scale debt service ratios (GDS/TDS) based on applicant(s) ‘ credit score(s) or the reason for purchase/renewal (primary residence vs. rental property). If one applicant on a joint mortgage has a credit score below 680, the lender may apply lending ratios as low as 32% GDS and 40% TDS. All criteria in the chart above apply to an owner-occupied primary residence mortgage with nesto.

Contractually insured mortgages are initially mortgage-default insured by the borrower at the time of purchase and have not been refinanced or changed in any way that increases their remaining contractual amortization or mortgage balance. These insured mortgages are also known as high-ratio mortgages. In contrast, insurable and uninsured terms apply to conventional mortgages that are back-end bulk portfolio-insured (typically lender-paid) or not.

New Purchase Qualifying Rates

Insured home purchases qualified for our lowest fixed rate. In today’s rate environment, your stress-tested qualifying rate is 6.09% (your contract rate plus 2%). If mortgage rates fall below 3.25%, the OSFI floor of 5.25% becomes binding instead.

Insured home purchases qualified for our lowest variable rate. In today’s rate environment, your stress-tested qualifying rate is 5.40% (your contract rate plus 2%). If mortgage rates fall below 3.25%, the OSFI floor of 5.25% becomes binding instead.

Insurable home purchases qualified for our lowest fixed rate. In today’s rate environment, your stress-tested qualifying rate is 6.09% (your contract rate plus 2%). If mortgage rates fall below 3.25%, the OSFI floor of 5.25% becomes binding instead.

Insurable home purchases qualified for our lowest variable rate. In today’s rate environment, your stress-tested qualifying rate is 5.45% (your contract rate plus 2%). If mortgage rates fall below 3.25%, the OSFI floor of 5.25% becomes binding instead.

Uninsured home purchases qualified for our lowest fixed rate. In today’s rate environment, your stress-tested qualifying rate is 6.64% (your contract rate plus 2%). If mortgage rates fall below 3.25%, the OSFI floor of 5.25% becomes binding instead.

Uninsured home purchases qualified for our lowest variable rate. In today’s rate environment, your stress-tested qualifying rate is 5.85% (your contract rate plus 2%). If mortgage rates fall below 3.25%, the OSFI floor of 5.25% becomes binding instead.

Renewal (Switch or Transfer) Qualifying Rates

An insured mortgage may be eligible for renewal at the contract rate, which may be our lowest fixed or variable insured rate, currently 4.09% and 3.40%, respectively.

An insurable mortgage may be eligible for renewal at the contract rate, which may be our lowest fixed or variable insurable rate, currently 4.09% and 3.45%, respectively.

An uninsured mortgage may be renewed at the contract rate, which may be our lowest fixed or variable uninsured rate, currently 4.64% and 3.85%, respectively.

Refinance Qualifying Rates

All refinances are considered uninsured transactions. In today’s rate environment, your stress-tested qualifying rate on our lowest uninsured fixed or variable rates is 6.64% and 5.85%, respectively (your contract rate plus 2%). If mortgage rates fall below 3.25%, the OSFI floor of 5.25% becomes binding instead.

Maximum Debt Ratio Limits and Mortgage Insurance

Mortgage default insurance is mandatory when your down payment is less than 20%. Insurance protects lenders against borrower default and allows higher qualifying debt ratios.

In Canada, mortgage insurance providers include:

• Canada Mortgage and Housing Corporation (CMHC)

• Sagen (GW)

• Canada Guaranty (CG)

Mortgage insurance is not available for:

• Properties valued at or above $1.5M

• Refinances

Typical Prime Lending Guidelines:

Insured Purchase under $1.5 million

Credit score: 680+

Max GDS: 39%

Max TDS: 44%

Uninsured Purchase over $1.5 million

Credit score: 680+

Max GDS: 35%

Max TDS: 42%

Refinances

Credit score: 680+

Max GDS: 35%

Max TDS: 42%

Guidelines vary by lender and borrower profile.

Determining Your Down Payment in Canada

Your down payment determines whether your mortgage is insured or uninsured and directly affects your qualifying ratios.

Minimum Down Payment Rules

• 5% on the first $500,000

• 10% on the portion above $500,000

• 20% minimum for properties valued at $1.5 million or more

To avoid mortgage insurance premiums entirely, you must make a down payment of at least 20%.

Example

Purchase price: $750,000

5% of the first $500,000 = $25,000

10% of the remaining $250,000 = $25,000

Minimum down payment = $50,000

A larger down payment reduces your mortgage size but does not eliminate stress test requirements. All new purchases and refinances must pass the federal mortgage stress test.

How Home Prices and Property Taxes Affect Mortgage Affordability in Canada

Home prices and property taxes work together to determine how much income you need to qualify for a mortgage. A higher purchase price increases your mortgage payment, while higher property taxes increase your GDS ratio. Since both are included in lender affordability calculations, they directly affect the maximum mortgage you can qualify for.

Mortgage affordability is not based solely on home price. It is based on:

• Purchase price

• Down payment

• Property taxes

• Heating costs

• Debt service ratios

• Stress test qualification

Even in cities with moderate home prices, higher property tax rates can reduce your qualifying power.

Average Home Prices and Estimated Monthly Property Taxes by Region

The table below shows benchmark home prices across Canada alongside estimated monthly property taxes. Both figures are used in mortgage qualification calculations.

| Province / City | Average Home Price | Property Tax Rate | Estimated Monthly Property Tax |

|---|---|---|---|

| Canada | $665,600 | 1% | $555 |

| British Columbia | $887,100 | 0.29% | $214 |

| Alberta | $516,600 | 0.71% | $306 |

| Saskatchewan | $385,900 | 1.33% | $428 |

| Manitoba | $398,700 | 1.38% | $458 |

| Ontario | $753,300 | 1.26% | $791 |

| Quebec | $550,400 | 0.71% | $326 |

| New Brunswick | $342,600 | 1.58% | $451 |

| Nova Scotia | $431,700 | 1.6% | $576 |

| Prince Edward Island | $382,100 | 1.59% | $506 |

| Newfoundland | $358,000 | 1.07% | $319 |

| Victoria | $890,100 | 0.44% | $326 |

| Vancouver | $1,099,100 | 0.3% | $275 |

| Calgary | $572,500 | 0.66% | $315 |

| Edmonton | $423,900 | 1.01% | $357 |

| Regina | $356,400 | 1.55% | $460 |

| Saskatoon | $448,400 | 1.34% | $501 |

| Winnipeg | $403,200 | 1.38% | $464 |

| Guelph | $725,000 | 1.4% | $846 |

| Hamilton | $737,400 | 1.43% | $879 |

| Kitchener | $642,000 | 1.36% | $728 |

| London | $561,100 | 1.68% | $786 |

| Mississauga | $953,400 | 1.04% | $826 |

| Ottawa | $632,200 | 1.23% | $648 |

| Toronto | $940,800 | 0.76% | $596 |

| Kingston | $549,900 | 1.55% | $710 |

| Windsor | $586,600 | 2.1% | $1,027 |

| Central Quebec | $357,900 | 0.7% | $209 |

| Estrie | $513,000 | 1.18% | $504 |

| Gatineau | $557,339 | 0.73% | $339 |

| Mauricie | $326,800 | 0.99% | $270 |

| Montreal | $596,300 | 0.9% | $447 |

| Quebec City | $444,600 | 0.85% | $315 |

| Saguenay | $397,065 | 1.12% | $371 |

| Sherbrooke | $586,883 | 0.76% | $372 |

| Trois-Rivieres | $452,065 | 0.92% | $347 |

| Fredericton | $360,100 | 1.87% | $561 |

| Moncton | $384,100 | 1.36% | $435 |

| Saint John | $358,700 | 2.12% | $634 |

| Halifax | $561,300 | 0.61% | $285 |

| St. John’s | $423,600 | 0.91% | $321 |

Affordability Impact Summary

Higher home prices increase your mortgage size and monthly payment. Higher property taxes increase your housing costs in the gross debt service ratio. Together, they determine the minimum income required to qualify under the mortgage stress test.

Example

A $900,000 home with $300 in monthly property taxes will require significantly less qualifying income than a $900,000 home with $800 in monthly property taxes, even if the mortgage amount is identical.

This is why location matters as much as purchase price when assessing affordability.

How Property Taxes Affect Your GDS

Property taxes are added directly to your monthly housing cost when calculating your gross debt service ratio:

GDS = (Mortgage Payment + Property Taxes + Heating + 50% Condo Fees) ÷ Gross Income

An increase of $200 per month in property taxes increases the required qualifying income by approximately $6,000 to $8,000 annually, depending on your ratio limits.

Mortgage Qualifying on a 25 Year Amortization

This table shows monthly stress-tested mortgage payments over a 25-year amortization, along with the average annual income required to service those payments on average-priced homes across Canada.

| Province / City | Actual Mortgage Payment (25Y) | Stress-Tested Payment (25Y) | Income Needed (Qualifying) |

|---|---|---|---|

| Canada | $3,279 | $3,985 | $142,747 |

| British Columbia | $4,370 | $5,311 | $173,077 |

| Alberta | $2,545 | $3,093 | $107,640 |

| Saskatchewan | $1,901 | $2,310 | $87,320 |

| Manitoba | $1,964 | $2,387 | $90,625 |

| Ontario | $3,711 | $4,510 | $166,172 |

| Quebec | $2,711 | $3,295 | $114,481 |

| New Brunswick | $1,688 | $2,051 | $80,064 |

| Nova Scotia | $2,127 | $2,584 | $100,307 |

| Prince Edward Island | $1,882 | $2,287 | $89,038 |

| Newfoundland | $1,764 | $2,143 | $78,843 |

| Victoria | $4,385 | $5,329 | $177,076 |

| Vancouver | $5,415 | $6,580 | $213,986 |

| Calgary | $2,820 | $3,427 | $118,220 |

| Edmonton | $2,088 | $2,538 | $92,137 |

| Regina | $1,756 | $2,134 | $82,890 |

| Saskatoon | $2,209 | $2,684 | $101,079 |

| Winnipeg | $1,986 | $2,414 | $91,614 |

| Guelph | $3,572 | $4,340 | $162,647 |

| Hamilton | $3,633 | $4,414 | $165,944 |

| Kitchener | $3,163 | $3,843 | $143,721 |

| London | $2,764 | $3,359 | $130,602 |

| Mississauga | $4,697 | $5,708 | $204,117 |

| Ottawa | $3,114 | $3,785 | $139,467 |

| Toronto | $4,635 | $5,632 | $194,706 |

| Kingston | $2,709 | $3,292 | $126,224 |

| Windsor | $2,890 | $3,512 | $142,715 |

| Central Quebec | $1,763 | $2,143 | $75,426 |

| Estrie | $2,527 | $3,071 | $113,093 |

| Gatineau | $2,746 | $3,337 | $116,171 |

| Mauricie | $1,610 | $1,956 | $71,569 |

| Montreal | $2,938 | $3,570 | $126,676 |

| Quebec City | $2,190 | $2,662 | $94,662 |

| Saguenay | $1,956 | $2,377 | $87,619 |

| Sherbrooke | $2,891 | $3,513 | $122,618 |

| Trois-Rivieres | $2,227 | $2,706 | $97,011 |

| Fredericton | $1,774 | $2,156 | $86,674 |

| Moncton | $1,892 | $2,299 | $87,223 |

| Saint John | $1,767 | $2,147 | $88,648 |

| Halifax | $2,765 | $3,360 | $115,248 |

| St. John’s | $2,087 | $2,536 | $90,988 |

25 Year Table Summary

Shorter amortization increases monthly payments and income required to qualify, but reduces total interest paid over time.

Mortgage Qualifying on a 30 Year Amortization

This table shows monthly stress-tested mortgage payments over a 30-year amortization, along with the average annual income required to service those payments on average-priced homes across Canada.

| Province / City | Actual Mortgage Payment (30Y) | Stress-Tested Payment (30Y) | Income Needed (Qualifying) |

|---|---|---|---|

| Canada | $2,968 | $3,756 | $134,473 |

| British Columbia | $3,956 | $5,006 | $162,049 |

| Alberta | $2,304 | $2,915 | $101,217 |

| Saskatchewan | $1,721 | $2,178 | $82,523 |

| Manitoba | $1,778 | $2,250 | $85,669 |

| Ontario | $3,360 | $4,251 | $156,808 |

| Quebec | $2,455 | $3,106 | $107,639 |

| New Brunswick | $1,528 | $1,933 | $75,805 |

| Nova Scotia | $1,925 | $2,436 | $94,940 |

| Prince Edward Island | $1,704 | $2,156 | $84,288 |

| Newfoundland | $1,597 | $2,020 | $74,392 |

| Victoria | $3,970 | $5,023 | $166,010 |

| Vancouver | $4,902 | $6,202 | $200,322 |

| Calgary | $2,553 | $3,231 | $111,103 |

| Edmonton | $1,890 | $2,392 | $86,868 |

| Regina | $1,589 | $2,011 | $78,460 |

| Saskatoon | $2,000 | $2,530 | $95,505 |

| Winnipeg | $1,798 | $2,275 | $86,601 |

| Guelph | $3,233 | $4,091 | $153,635 |

| Hamilton | $3,289 | $4,161 | $156,777 |

| Kitchener | $2,863 | $3,623 | $135,740 |

| London | $2,502 | $3,166 | $123,627 |

| Mississauga | $4,252 | $5,380 | $192,265 |

| Ottawa | $2,819 | $3,567 | $131,608 |

| Toronto | $4,196 | $5,309 | $183,010 |

| Kingston | $2,452 | $3,103 | $119,388 |

| Windsor | $2,616 | $3,310 | $135,423 |

| Central Quebec | $1,596 | $2,020 | $70,977 |

| Estrie | $2,288 | $2,895 | $106,716 |

| Gatineau | $2,486 | $3,145 | $109,243 |

| Mauricie | $1,457 | $1,844 | $67,507 |

| Montreal | $2,659 | $3,365 | $119,264 |

| Quebec City | $1,983 | $2,509 | $89,135 |

| Saguenay | $1,771 | $2,241 | $82,683 |

| Sherbrooke | $2,617 | $3,312 | $115,322 |

| Trois-Rivieres | $2,016 | $2,551 | $91,392 |

| Fredericton | $1,606 | $2,032 | $82,197 |

| Moncton | $1,713 | $2,167 | $82,447 |

| Saint John | $1,600 | $2,024 | $84,189 |

| Halifax | $2,503 | $3,167 | $108,270 |

| St. John’s | $1,889 | $2,390 | $85,722 |

30 Year Table Summary

A longer amortization lowers monthly payments and may increase qualification flexibility, but total borrowing costs increase over time.

Closing Costs and Cash Requirements

In addition to your down payment, buyers must have funds available to cover closing costs. These typically range from 1% to 4% of the purchase price and may include:

• Legal fees

• Land transfer tax

• Title insurance

• Home inspection

• Appraisal fees

Buyers must also provide a deposit when submitting an offer to purchase, often around 5% of the purchase price. The deposit forms part of the down payment.

Closing costs cannot be borrowed and do not count toward your minimum down payment requirement.

How to Increase Your Mortgage Affordability

There are several ways to increase your mortgage affordability and boost your buying power to ensure you’re viewed as a responsible borrower in the eyes of lenders. Here are some of the recommendations to increase your affordability:

Reduce Outstanding Debt: Lower credit card balances and loan payments to improve your total debt service (TDS) ratio.

Improve Your Credit Score: A minimum score of 680 is typically required for insured mortgages. Scores above 720 often qualify for better mortgage rates and options.

Increase Your Down Payment: A larger down payment lowers your loan size, but ensure you maintain sufficient savings after closing.

Consider A Lower Purchase Price: Lower home values reduce required income and strengthen approval.

Extend Amortization Where Eligible: A longer amortization lowers monthly payments but increases total interest costs.

We’re curious…

Are you a first-time buyer?

Frequently Asked Questions (FAQ) About Calculating Mortgage Affordability in Canada

How much mortgage can I afford in Canada?

In Canada, most borrowers can afford a mortgage between 3.5 and 4.5 times their gross annual household income, assuming minimal existing debt. A household earning $100,000 typically qualifies for $350,000 to $450,000.

The exact amount depends on your down payment, property taxes, heating costs, credit score, and whether your mortgage is insured or uninsured. Lenders cap housing costs at 35% to 39% of gross income and total debt payments at 42% to 44%, and you must qualify under the federal stress test at the higher of 5.25% or your contract rate plus 2%.

Does a car loan affect how much mortgage I can afford?

A car loan significantly reduces mortgage affordability because it is included in the total debt service (TDS) ratio calculation. For every $100 of monthly car loan payments, your maximum qualifying mortgage amount may decrease by approximately $12,000 to $15,000.

How do I calculate mortgage affordability in Canada?

To calculate mortgage affordability, add your monthly mortgage payment, property taxes, heating costs, and 50% of condo fees, then divide this total by your gross monthly income. This result is your gross debt service (GDS) ratio, which should generally stay below 39% for mortgage approval.

What is the “Rule of Thumb” for mortgage affordability?

The Canadian mortgage affordability rule of thumb is to multiply your gross annual household income by 4. This estimate assumes a 5% down payment and moderate existing debt levels, though the mortgage stress test may lower this multiple for some borrowers.

How do mortgage lenders check affordability?

Lenders verify your income through employment documents or tax filings, assess property taxes and heating costs, calculate your gross and total debt service ratios, and confirm that you qualify under the mortgage stress test before issuing approval.

What income do I need to qualify for a mortgage in Canada?

You need sufficient income to keep your gross debt service ratio within lender limits, typically up to 39% for insured mortgages and around 35% for uninsured mortgages. In practice, many borrowers qualify for a mortgage of 3.5 to 4.5 times their gross annual income, depending on their debt levels and stress test requirements.

Does the mortgage stress test reduce how much I can afford?

The mortgage stress test can reduce your maximum borrowing capacity. In Canada, borrowers must qualify at the higher of 5.25% or their contract rate plus 2%. Even if your actual rate is lower, lenders calculate affordability using the higher qualifying rate, which can reduce the mortgage amount you qualify for by 10% to 20%.

However, borrowers are no longer required to pass the stress test when switching lenders at renewal. As long as they do not increase their remaining amortization (buy time) or mortgage balance (buy money), their mortgage renewal may be qualified at the contract rate offered by their new lender.

Why Choose nesto

At nesto, our commission-free mortgage experts, certified in multiple provinces, provide exceptional advice and service that exceeds industry standards. Our mortgage experts are salaried employees who provide impartial guidance on mortgage options tailored to your needs and are evaluated based on client satisfaction and the quality of their advice. nesto aims to transform the mortgage industry by providing honest advice and competitive rates through a 100% digital, transparent, and seamless process.

nesto is on a mission to offer a positive, empowering and transparent property financing experience – simplified from start to finish.

Contact our licensed and knowledgeable mortgage experts to find your best mortgage rate in Canada.