Mortgage Defaults and Foreclosures Rise With Elevated Interest Rates

Mortgage defaults and foreclosures are edging higher in Canada after years of sitting at record lows. The shift comes as more than 1.15 million mortgages are set to renew in 2026, leaving households with far higher payments than during the pandemic’s ultra-low-rate era.

According to the Bank of Canada, “About 60% of renewing households in 2025 and 2026 will face higher payments.” On average, 2026 renewals could result in payments approximately 20% higher than last year’s, creating financial strain for many families. OSFI and CMHC caution that delinquency rates will continue to climb, but also note that systemic risks remain contained, thanks to strong insured mortgage portfolios.

Key Takeaways

- Mortgage defaults are rising, but arrears remain below 0.5%, indicating systemic risk remains low.

- Renewals in 2026 are the main pressure point, with most households facing higher payments.

- Consumer credit stress and private lending add to market risks in Ontario and BC.

Best Mortgage Rates

Why Defaults Are Rising

Defaults don’t increase in isolation; they build when multiple pressures converge. In today’s market, four forces are pushing households closer to the edge: higher renewal costs, already stretched consumer credit, the expiration of pandemic-era low interest rates, and price pressures from US tariffs and the reconfiguration of global supply chains.

Borrowers who secured mortgages in 2020–21 at rates under 2% are now seeing renewal offers in the 4–5% range. OSFI put it plainly in its 2025 commentary that mortgage delinquencies are expected to continue to rise, particularly in large urban markets.

Consumer credit stress exacerbates this problem. Equifax Canada noted that “non-mortgage delinquencies have reached levels not seen since 2009.” Families juggling late car or credit card payments are in a weaker position to absorb higher mortgage bills.

Regional and Market Impacts

Canada isn’t experiencing a uniform rise in mortgage defaults; instead, it is concentrated in certain regions. A recent Equifax report shows Ontario remains a hotspot for financial distress, with the 90-plus days delinquency rate hitting 1.75%, which is 0.152 percentage points above the national average. Alberta also stands out, posting a delinquency rate of 1.98%, or 0.385 percentage points above the national average.

Younger Canadians are especially squeezed; those under 36 saw their average non-mortgage balance increase to more than $14,000, and their 90-plus days delinquency rate surged 19.7% year-over-year. This indicates that, despite overall delinquency levels appearing to plateau, the financial gap is widening for segments with limited headroom, particularly in high-cost regions such as Ontario and Alberta.

Defaults aren’t rising evenly. Areas with higher cost of living, steeper debt ratios, and a younger demographic facing rising non-mortgage delinquency are bearing disproportionate strain. That’s the risk behind headlines about stabilizing delinquency, which mask deeper, uneven pressures beneath the surface.

Broader Price Pressures from Tariffs and Global Supply Chains

Beyond mortgages and credit, household budgets are also being squeezed by rising prices on everyday goods. Recent US tariffs on Canadian exports, combined with the reconfiguration of global supply chains, are adding costs across food, energy, and manufactured products. These pressures act like a stealth tax on Canadian households; even if wages keep pace, essentials like groceries and fuel are consuming a larger portion of each paycheque.

The Bank of Canada has acknowledged that global trade uncertainty makes it more challenging to return inflation to its target. As long as these price shocks persist, the central bank is less likely to cut rates, which means mortgage payments will remain elevated for an extended period. For borrowers already facing renewal shock, higher household costs from tariffs and supply disruptions shrink the cushion they need to stay current on mortgages.

High interest rates got you stressed?

Find your low rate refinance with nesto today

Impact of Interest Rates on Renewals

Mortgage rates in Canada have a disproportionate impact on household budgets. A slight change in percentage points can add hundreds to monthly mortgage costs, often erasing any gains from wage growth or tax relief.

The Bank of Canada has maintained its policy rate at 2.75% since its March 12th announcement. While this avoided another rate hike, it locked borrowers into a reality of elevated costs. As the Bank itself noted, “Higher interest rates are affecting more households as their mortgages renew.”

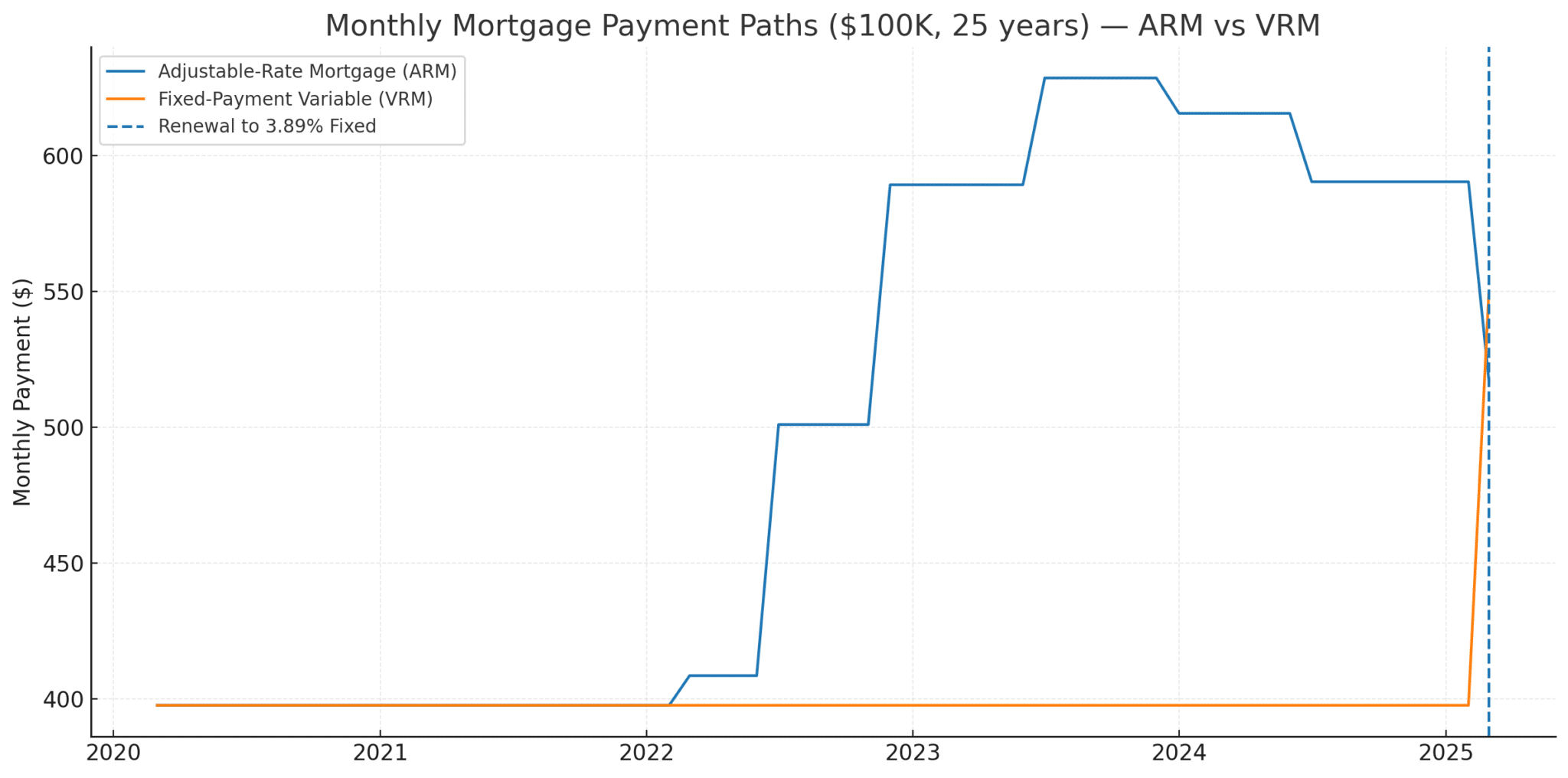

To see the payment renewal shock policymakers warn about in action, let’s consider a $100,000 adjustable-rate mortgage (ARM) with a 25-year amortization and a rate of prime –1% in March 2020, when the prime rate in Canada fell to 2.45%. This mortgage continues to follow the Bank of Canada’s policy rate adjustments until March 2025, when it is renewed into a 5-year fixed rate at 3.89%. Let’s also track the exact month-by-month changes for a fixed-payment variable-rate mortgage (VRM).

- By mid-2022, the ARM borrower was already paying almost $100 more per month than the VRM borrower, but they were still reducing their outstanding balance faster.

- By July 2023, the VRM borrower’s payment was entirely consumed by interest, with zero principal repayment, and the remaining balance had hardly moved.

- At renewal in March 2025, the ARM balance had dropped to approximately $86,000, while the VRM balance remained above $91,000. The VRM borrower also faced a sharp jump in payments when the renewal recalculation happened, reducing the remaining amortization back to 20 years.

Numbers Behind the Chart: Variable-Rate Mortgage (Fixed Payment)

| Month | Payment | Interest | Principal | Balance |

|---|---|---|---|---|

| March 2020 | $397.59 | $120.83 | $276.76 | $99,723.24 |

| April 2020 | $397.59 | $120.50 | $277.09 | $99,446.15 |

| May 2020 | $397.59 | $120.16 | $277.43 | $99,168.72 |

| June 2020 | $397.59 | $119.83 | $277.76 | $98,890.96 |

| July 2020 | $397.59 | $119.49 | $278.10 | $98,612.86 |

| August 2020 | $397.59 | $119.16 | $278.43 | $98,334.43 |

| September 2020 | $397.59 | $118.82 | $278.77 | $98,055.66 |

| October 2020 | $397.59 | $118.48 | $279.11 | $97,776.55 |

| November 2020 | $397.59 | $118.15 | $279.44 | $97,497.10 |

| December 2020 | $397.59 | $117.81 | $279.78 | $97,217.32 |

| January 2021 | $397.59 | $117.47 | $280.12 | $96,937.20 |

| February 2021 | $397.59 | $117.13 | $280.46 | $96,656.74 |

| March 2021 | $397.59 | $116.79 | $280.80 | $96,375.95 |

| April 2021 | $397.59 | $116.45 | $281.14 | $96,094.81 |

| May 2021 | $397.59 | $116.11 | $281.48 | $95,813.33 |

| June 2021 | $397.59 | $115.77 | $281.82 | $95,531.51 |

| July 2021 | $397.59 | $115.43 | $282.16 | $95,249.36 |

| August 2021 | $397.59 | $115.09 | $282.50 | $94,966.86 |

| September 2021 | $397.59 | $114.75 | $282.84 | $94,684.02 |

| October 2021 | $397.59 | $114.41 | $283.18 | $94,400.84 |

| November 2021 | $397.59 | $114.07 | $283.52 | $94,117.31 |

| December 2021 | $397.59 | $113.73 | $283.87 | $93,833.45 |

| January 2022 | $397.59 | $113.38 | $284.21 | $93,549.24 |

| February 2022 | $397.59 | $113.04 | $284.55 | $93,264.69 |

| March 2022 | $397.59 | $132.12 | $265.47 | $92,999.22 |

| April 2022 | $397.59 | $131.75 | $265.84 | $92,733.38 |

| May 2022 | $397.59 | $131.37 | $266.22 | $92,467.16 |

| June 2022 | $397.59 | $131.00 | $266.60 | $92,200.56 |

| July 2022 | $397.59 | $284.29 | $113.31 | $92,087.25 |

| August 2022 | $397.59 | $283.94 | $113.66 | $91,973.60 |

| September 2022 | $397.59 | $283.59 | $114.01 | $91,859.59 |

| October 2022 | $397.59 | $283.23 | $114.36 | $91,745.24 |

| November 2022 | $397.59 | $282.88 | $114.71 | $91,630.53 |

| December 2022 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| January 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| February 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| March 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| April 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| May 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| June 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| July 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| August 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| September 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| October 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| November 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| December 2023 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| January 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| February 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| March 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| April 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| May 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| June 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| July 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| August 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| September 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| October 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| November 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| December 2024 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| January 2025 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| February 2025 | $397.59 | $397.59 | $0.00 | $91,630.53 |

| March 2025 | $549.97 | $297.04 | $252.93 | $91,377.59 |

Numbers Behind the Chart: Adjustable-Rate Mortgage (Fluctuating Payment)

| Month | Payment | Interest | Principal | Balance |

|---|---|---|---|---|

| March 2020 | $397.59 | $120.83 | $276.76 | $99,723.24 |

| April 2020 | $396.49 | $120.50 | $275.99 | $99,447.25 |

| May 2020 | $395.39 | $120.17 | $275.23 | $99,172.02 |

| June 2020 | $394.30 | $119.83 | $274.47 | $98,897.56 |

| July 2020 | $393.21 | $119.50 | $273.71 | $98,623.85 |

| August 2020 | $392.12 | $119.17 | $272.95 | $98,350.90 |

| September 2020 | $391.03 | $118.84 | $272.19 | $98,078.70 |

| October 2020 | $389.95 | $118.51 | $271.44 | $97,807.26 |

| November 2020 | $388.87 | $118.18 | $270.69 | $97,536.57 |

| December 2020 | $387.80 | $117.86 | $269.94 | $97,266.63 |

| January 2021 | $386.72 | $117.53 | $269.19 | $96,997.44 |

| February 2021 | $385.65 | $117.21 | $268.45 | $96,728.99 |

| March 2021 | $397.89 | $116.88 | $281.01 | $96,447.99 |

| April 2021 | $396.73 | $116.54 | $280.19 | $96,167.79 |

| May 2021 | $395.58 | $116.20 | $279.38 | $95,888.42 |

| June 2021 | $394.43 | $115.87 | $278.57 | $95,609.85 |

| July 2021 | $393.29 | $115.53 | $277.76 | $95,332.09 |

| August 2021 | $392.14 | $115.19 | $276.95 | $95,055.14 |

| September 2021 | $391.00 | $114.86 | $276.14 | $94,779.00 |

| October 2021 | $389.87 | $114.52 | $275.34 | $94,503.66 |

| November 2021 | $388.73 | $114.19 | $274.54 | $94,229.11 |

| December 2021 | $387.61 | $113.86 | $273.75 | $93,955.37 |

| January 2022 | $386.48 | $113.53 | $272.95 | $93,682.42 |

| February 2022 | $385.36 | $113.20 | $272.16 | $93,410.26 |

| March 2022 | $409.15 | $132.33 | $276.81 | $93,133.45 |

| April 2022 | $407.93 | $131.94 | $275.99 | $92,857.45 |

| May 2022 | $406.72 | $131.55 | $275.18 | $92,582.28 |

| June 2022 | $405.52 | $131.16 | $274.36 | $92,307.91 |

| July 2022 | $497.19 | $284.62 | $212.57 | $92,095.34 |

| August 2022 | $496.04 | $283.96 | $212.08 | $91,883.26 |

| September 2022 | $494.90 | $283.31 | $211.59 | $91,671.67 |

| October 2022 | $493.76 | $282.65 | $211.11 | $91,460.56 |

| November 2022 | $492.62 | $282.00 | $210.62 | $91,249.94 |

| December 2022 | $580.69 | $414.43 | $166.26 | $91,083.68 |

| January 2023 | $579.63 | $413.67 | $165.96 | $90,917.73 |

| February 2023 | $578.57 | $412.92 | $165.65 | $90,752.07 |

| March 2023 | $590.76 | $412.17 | $178.60 | $90,573.48 |

| April 2023 | $589.60 | $411.35 | $178.24 | $90,395.23 |

| May 2023 | $588.44 | $410.55 | $177.89 | $90,217.34 |

| June 2023 | $587.28 | $409.74 | $177.54 | $90,039.80 |

| July 2023 | $625.73 | $465.21 | $160.52 | $89,879.27 |

| August 2023 | $624.61 | $464.38 | $160.23 | $89,719.04 |

| September 2023 | $623.50 | $463.55 | $159.95 | $89,559.09 |

| October 2023 | $622.39 | $462.72 | $159.66 | $89,399.43 |

| November 2023 | $621.28 | $461.90 | $159.38 | $89,240.05 |

| December 2023 | $620.17 | $461.07 | $159.10 | $89,080.95 |

| January 2024 | $605.86 | $441.69 | $164.17 | $88,916.78 |

| February 2024 | $604.74 | $440.88 | $163.86 | $88,752.92 |

| March 2024 | $617.67 | $440.07 | $177.60 | $88,575.32 |

| April 2024 | $616.43 | $439.19 | $177.25 | $88,398.07 |

| May 2024 | $615.20 | $438.31 | $176.89 | $88,221.18 |

| June 2024 | $613.97 | $437.43 | $176.54 | $88,044.65 |

| July 2024 | $587.36 | $399.87 | $187.49 | $87,857.16 |

| August 2024 | $586.11 | $399.02 | $187.09 | $87,670.07 |

| September 2024 | $584.86 | $398.17 | $186.69 | $87,483.37 |

| October 2024 | $583.62 | $397.32 | $186.30 | $87,297.08 |

| November 2024 | $582.37 | $396.47 | $185.90 | $87,111.18 |

| December 2024 | $581.13 | $395.63 | $185.50 | $86,925.68 |

| January 2025 | $579.90 | $394.79 | $185.11 | $86,740.57 |

| February 2025 | $578.66 | $393.95 | $184.71 | $86,555.85 |

| March 2025 | $519.51 | $280.59 | $238.92 | $86,316.93 |

Today’s Best Mortgage Rates as of July 31, 2026

Mortgage Strategies to Reduce Risk

While rising payments are unavoidable for many, borrowers are not powerless. By adjusting how they structure their mortgage, or even planning for renewal early, households can significantly reduce stress. Strategies vary depending on whether you’re buying, renewing, or refinancing.

For Homebuyers

Homebuyers today face higher borrowing costs, but tools exist to make mortgages more manageable.

- Insured mortgages: By using mortgage insurance, buyers may qualify for lower mortgage rates and reduce their monthly payment despite paying a premium. Insured mortgages are especially valuable in high-cost regions.

- Longer amortizations: Extending the amortization to 30 years reduces monthly payments, providing households with breathing room, even if it means paying more interest over the long term.

For Renewers

For those already in the market, renewal is where the most pressure is being felt. Planning can prevent painful surprises.

- Shop early: Securing a rate hold months in advance can shield borrowers from unexpected increases.

- Switch lenders without re-qualifying: An option available to insured lending, OSFI recently confirmed that uninsured borrowers can switch lenders at renewal without re-qualifying if their debt service costs remain unchanged. Removal of the stress test when switching mortgages between lenders boosts competition and creates opportunities for better deals.

- Budget for higher costs: Using the BoC’s estimate of 10% higher payments as a guide, households should run their numbers well before renewal to see how their finances will adapt.

For Refinancers

Refinancing is increasingly being used as a financial survival tactic rather than a tool for equity withdrawal.

- Re-amortize: By extending the remaining amortization, payments can be brought back into a manageable range.

- Consolidate debt: Wrapping higher-interest credit cards or personal loans into a mortgage often reduces total monthly obligations, even though the long-term costs may be higher.

- Expect more scrutiny: Lenders are tightening requirements as defaults rise. Files that were approved in 2021 may now be subject to additional questions or terms and conditions.

Role of the Bank of Canada and Regulators

The Bank of Canada has acknowledged that its interest rate policy is restricting households’ budgets. “About 60% of renewing households in 2025 and 2026 will face higher payments.” The higher interest payments are a deliberate trade-off to make the central bank’s monetary policy effective, placing stress on household budgets to cool inflationary pressures.

At the same time, CMHC and private insurers offer a more reassuring view. CMHC reported insured arrears at 0.30% in Q1 2025, while Canada Guaranty’s delinquency rate was 0.13%. As CMHC summarized, “Mortgage delinquency rates have increased in Ontario and British Columbia but remain low overall.”

FSRA reminds us in it’s most recent Private Lending Report that private borrowers face a different reality: “This increase in the mortgage delinquency rate underscores the growing financial strain on individuals who rely on Non-Bank Lenders, many of whom may struggle with higher interest rates, short-term financing, limited refinancing options, and a lack of an exit strategy to transition back to a traditional mortgage.” This helps explain why stress is emerging more rapidly in certain market segments.

Foreclosures vs. Power of Sale in Canada

The process for recovering a property after default depends on where you live. In Ontario, New Brunswick, Prince Edward Island, and Newfoundland and Labrador, lenders typically use the power of sale, which allows them to sell the home without going to court. For borrowers, that means timelines are shorter than expected, especially with private lenders who may act quickly once payments are missed. In Québec, Alberta, British Columbia, Manitoba, Saskatchewan, and Nova Scotia, as well as in the territories, the process is a judicial foreclosure, which requires court approval.

Frequently Asked Questions (FAQ) About Rising Mortgage Delinquencies and Foreclosures

Will mortgage defaults cause a housing crash in Canada?

Mortgage defaults are rising, but they remain low by historical standards. CMHC reports arrears at a rate below 0.5%, and private mortgage insurers, such as Canada Guaranty, report an even lower delinquency rate.

What happens if I can’t make my mortgage payment?

Contact your lender immediately. Options may include deferrals, capitalizing payments, refinancing, or adjusting terms. Communicating with your mortgage lender and acting early can help avoid power-of-sale enforcement.

How much will my payments rise at renewal?

The BoC estimates renewers in 2026 will face payments about 20% higher than last year’s, with most households seeing increases.

What’s the difference between foreclosure and power of sale?

Foreclosure is a judicial (court) process, rare in Canada. Power of sale is a more common, expedited process that allows lenders to sell the property without court involvement.

Are insured mortgages safer from default risk?

Insured portfolios historically show much lower arrears. CMHC’s insured arrears were just 0.30% in Q1 2025, compared with higher rates among private lenders.

Final Thoughts

Mortgage defaults and delinquencies are climbing as Canadians face higher renewal rates, but they remain historically low and concentrated in specific markets. The actual household stress continues to unfold over 2026, when most borrowers face higher monthly payments due to payment shock at renewal.

For borrowers, preparation is the best defence. Homebuyers can lean on insured products and longer amortizations, renewers can shop early and avoid the mortgage stress test to switch lenders. Those looking to refinance can focus on re-amortization or debt consolidation.

To find the mortgage best suited to your unique needs and financial situation, connect with nesto mortgage experts. We’ll help you navigate renewal costs, compare your options, and build a long-term strategy to protect your home and finances.

Why Choose nesto

At nesto, our commission-free mortgage experts, certified in multiple provinces, provide exceptional advice and service that exceeds industry standards. Our mortgage experts are salaried employees who provide impartial guidance on mortgage options tailored to your needs and are evaluated based on client satisfaction and the quality of their advice. nesto aims to transform the mortgage industry by providing honest advice and competitive rates through a 100% digital, transparent, and seamless process.

nesto is on a mission to offer a positive, empowering and transparent property financing experience – simplified from start to finish.

Contact our licensed and knowledgeable mortgage experts to find your best mortgage rate in Canada.