What To Know About Collateral Mortgage vs. Standard Mortgage

Buying a home is one of life’s most significant financial decisions. When obtaining a mortgage, the property being mortgaged will act as a security to protect the lender’s interests in the event of default. This security is commonly referred to as collateral. A collateral mortgage is a type of security registered against a property by a lender. Unlike a traditional mortgage or a standard or conventional charge, a collateral mortgage charge secures the amount borrowed and any additional debts or credit the borrower may incur. This means the borrower’s total real estate indebtedness to the lender can be secured under one charge.

While collateral charges can offer certain benefits to lenders and borrowers, they are also complex and challenging to understand fully. This blog post will look at collateral mortgage charges and how they differ from standard or conventional mortgage charges. Whether you are a first-time homebuyer or an experienced real estate investor, understanding collateral mortgage charges can help you make more informed decisions regarding your mortgage financing.

Key Highlights

- A standard or conventional mortgage can allow for secondary financings, such as second mortgages.

- Collateral mortgages can be cost and time-effective for both borrowers and lenders.

- Collateral mortgages can also be more costly than standard mortgages, as they must be discharged before being transferred or switched to another lender.

Best Mortgage Rates

What’s A Standard Charge Mortgage?

A standard charge mortgage is where the lender registers a legal charge against the mortgaged property. This charge gives the lender a legal claim to the property if the borrower defaults. The charge is registered with specific terms and conditions, as well as the contract rate, with the land registry office. Standard charge mortgages are also known as conventional mortgages or conventional charge mortgages.

Standard or Conventional Charge Mortgage Pros and Cons

One of the main advantages of a standard charge mortgage is that it offers the lender a greater degree of flexibility on the terms and conditions of the loan. Additionally, lenders are willing to take the risk of lending behind a standard or conventional charge mortgage, such as allowing the client to arrange a second mortgage to take out equity without having to pay the penalty to discharge the first mortgage. Another advantage of a standard charge mortgage is that it can be easier to transfer the mortgage to another lender. Since the standard charge is registered against the property, the mortgage can be transferred as a switch/transfer at renewal with a new lender.

It’s important to address some disadvantages of standard charge mortgages. Standard charge mortgages can be less flexible than other types of mortgages. Since the lender has a legal charge against the property, the borrower may have limited options for making changes to the loan or accessing additional funds. Want to learn more about conventional mortgages? Check out this blog post from nesto.

What is a Collateral Charge Mortgage?

In Canada, a collateral charge is a type of mortgage where the lender registers a legal charge against the property for a total amount exceeding the actual mortgage loan amount. This means that the borrower’s total indebtedness to the lender can be secured under one charge, including the mortgage loan and any other debts or credits the borrower may incur. The collateral mortgage meaning, by definition, can be a bit more complicated to explain than a conventional or a standard mortgage.

A collateral charge can also be a re-advanceable mortgage or an on-demand loan. These other names make it easier to understand the benefits of the collateral charge mortgage. Once the collateral charge is registered as a mortgage against a property, the borrower can re-advance the loan within its limits. Until the lender discharges it, the collateral charge mortgage will remain intact even if any debts secured against it are paid off. This allows new loans or secured lines of credit (HELOCs) to be set up on-demand – without needing a credit adjudication or approval process.

Collateral Mortgage Pros and Cons

One of the main advantages of a collateral charge mortgage is that it gives borrowers greater flexibility when accessing additional funds. Since the charge secures not only the initial mortgage loan but also any other debts or credit that the borrower may incur in the future, borrowers can access additional funds without having to go through the legal process of registering a new charge against the property. Additionally, this being a re-advanceable mortgage allows borrowers to access additional funds as needed, up to a predetermined credit limit. As the borrower pays the mortgage and builds equity in the property, they can continue to access additional funds through the revolving credit (HELOC) portion of the mortgage.

The re-advanceable aspect of a collateral charge mortgage gives borrowers greater flexibility in managing their finances. Since the revolving credit (HELOC) portion of the mortgage can be used for any purpose, borrowers can fund renovations, pay off high-interest debt, or cover unexpected expenses. Another advantage is that it can help borrowers save money on interest charges. Since the mortgage’s revolving credit (HELOC) portion typically has a variable interest rate tied to the prime lending rate, borrowers may take advantage of lower interest rates over time. One of the biggest advantages is the ability to switch a revolving credit (HELOC) portion fully or partially to a mortgage (term loan). Like a mortgage, a term loan has a beginning and an end based on its repayment schedule of principal and interest.

There are also some potential disadvantages to collateral charge mortgages. For example, they cannot be switched to a different lender since the charge is registered for the total amount of indebtedness rather than just the mortgage loan amount alone. Discharging this type of charge requires moving to a new lender.

Another disadvantage is that collateral charge mortgages come with higher fees to set up or discharge than standard or conventional mortgages. When a mortgage loan is renewed, most lenders will not cover the cost of moving a collateral charge mortgage – or discharge fees to leave a lender.

A collateral charge can be registered for up to 125% of the property’s value. This can be both an advantage and a disadvantage. This can be advantageous if your property increases in value over time. Then, you could refinance your home without having to pay for new legal documents as long as the 80% (loan-to-value limitation of all conventional mortgages) of the new value of your property is within the registered value of the charge. However, this can also be a disadvantage as it can easily make you overleveraged. For example, your revolving credit (HELOC) portion can be set up with an automatic limit increase as any principal portion is paid down on your mortgage (term loan) within the collateral charge. Want to learn more about collateral charges? Check out this blog post from nesto.

Best Mortgage Rates

Collateral vs. standard mortgage: A visual of their differences

In this section, we have created a table to compare the similarities and differences between collateral and conventional mortgages.

| Why it matters | Standard Charge | Collateral Charge | Common to both standard and collateral charge | |

|---|---|---|---|---|

| Borrowing Limitation | To manage borrowing capacity on the facility. | The original mortgage amount cannot be extended once paid down. | Discharge fees can range from $200 to $300, plus title registration fees. The borrower pays new collateral mortgage fees ($1000 to $1500), which the lender can cover by slightly increasing the mortgage rate. | Mortgage (term loans) cannot be increased. |

| Fees | Discharge and Registration fees can vary. | Discharge fees can range from $100 to $150, plus title registration fees. The lender covers new standard mortgage fees ($200 to $500) for transfers. | Depending on the lender, an in-person visit may be required to confirm identity and due diligence. | Title registration office fees are the same. |

| Process | Who can be joined on the mortgage, and how does their mortgage impact them? | It can be completed virtually if the mortgage is being transferred at renewal with a new lender. | It may require in-person signing with a legal expert or at the bank/lender where the financing is being arranged. | The virtual process is not always possible. |

| Covenant Limitations | Who can be made joint on the mortgage, and how does their mortgage impact them? | Limited to 4 individuals on a mortgage. One of these individuals can be a corporation if the other persons on the mortgage act as security. They can be joint tenants in common (&) or joint tenants with the right of survivorship (/). | Limited to 2 individuals – these individuals must be persons and not corporations. They must be joint tenants with the right of survivorship. If one person dies, the title and obligations pass to the other. | N/A |

| Registration Limitations | How and how much can be borrowed? | Maximum limit of 95% of the property value for insured (high ratio mortgage with borrower-paid insurance premium) mortgages. Limited to one standard mortgage product (term loan). | Maximum limit of 80% of the property value for a conventional (uninsured with 20% down payment) mortgage. The charge can be registered for up to 125% of the property value. No limit on the number of products except those that the lender has set up. | Mortgages are always limited to the qualifying amount based on income and property value. |

| Flexibility | Ability to mitigate if financial situation changes. | It is possible to early renew your mortgage without a penalty through a blend and extend. Early renewal will extend your term and change the interest rate and monthly payment. | Changes can be made within the registered charge limit without a refinance. A new facility, such as revolving credit (HELOC), can be set up to make prepayments on the term loan (mortgage), thus reducing the penalty. If rates have fallen since the original collateral mortgage was set up, the penalty can be reduced by paying down the mortgage at a higher rate to set up another mortgage at a lower rate. | N/A |

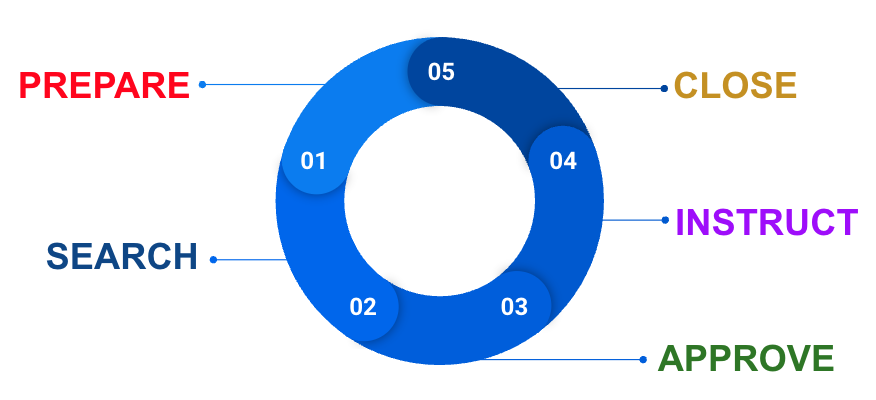

Steps for Securing a Collateral or Standard Mortgage

In this section, we’ll examine all the home-buying steps involved in obtaining a collateral mortgage and how they differ from those involved in obtaining a conventional mortgage.

PREPARE – This initial stage is more for understanding your financial situation and less about locking in a rate. It’s essential to understand that when lenders lock in a rate for you at this stage (preapproval), your rate will be higher as they have built in some risk for setting aside money for your mortgage. Lenders with the lowest rates, like nesto, will spend their money on keeping their rates low instead of offering a rate lock at the preapproval stage. Lenders will assess your financial situation to qualify for a mortgage without a rate lock (prequalification). This means that you’ll get a realistic idea of your affordability based on your current financial situation – with the ability to lock in your rate once you find your property (approval). Regardless if you qualify for a conventional or collateral mortgage, all lenders will need to stress test you, check your credit score and review your credit report to determine the risk you bring.

SEARCH – This is the stage where you’re searching for it all. You’re searching for a realtor, property, solicitor and documents. In the prequalification stage, a mortgage expert will help you understand approximately the amount of mortgage you’ll qualify for and what documents will be needed to confirm your downpayment, closing costs and income. This stage will prepare you to start collecting documents – with additional documents needed once you find your property (purchase agreement, MLS, copy of the deposit draft made out to the solicitor’s trust account).

Additionally, you’ll need the contact information for the realtor and solicitor ready for the next stage. If you purchase your home directly from the seller (private sale), you’ll need a copy of the most recent tax bill instead of the MLS listing and realtor. Depending on the province, if a private sale occurs, you and the seller may be required to have different solicitors for due diligence on the lender’s side.

APPROVE – Now you have found the home you want to make an offer on at this stage. You may connect with your mortgage expert to confirm any discrepancies. For instance, if you have provided an annual income but get a bonus, they need to confirm the two-year average from your T4s. You will also want to confirm the purchase price, downpayment, square footage, taxes and condo or maintenance fees, if applicable – which should all be on the MLS listing. At this point, you will provide the purchase agreement and other due diligence documents to proceed with your mortgage approval. If you have conditioned for inspection, you’ll usually have 5 days to get this done before your conditions are waived.

INSTRUCT – You’re almost done and close to having the keys to your new home. At this stage, the lender will need your waiver of the financing conditions – officially known as the notice of fulfillment (NOF). This means you have officially locked in your contract to purchase the property. Once the lender is satisfied with your NOF (also referred to as COF) and any other missing documents, they will instruct your solicitor to start preparing your legal documentation. Missing documents or additional bank statements may be needed to satisfy anti-money laundering due diligence on the source of funds. Usually, you want to give your solicitor as much time to complete their due diligence. However, sometimes issues can come up, and if you’re keeping your solicitor up to date, you should be able to close within 5 days of them being instructed.

CLOSE – This is the final stage where you’ll become a homeowner. This may require a signature at the solicitor’s office – perhaps a visit to the lender’s office/branch. Many banks offer collateral charge mortgages de facto – especially if your down payment is more than 20%. Before this process, it is crucial to have a conversation with your mortgage expert and solicitor to ensure that you’re getting the type of mortgage charge that suits your situation. Getting legal advice regarding your relationship with your partner for the mortgage would be prudent. For example, if you’re not married but buying a home together, you may wish to be tenants in common (where each owns half the home) versus joint tenants (where both parties own the home). This choice may limit your ability to purchase a home with a collateral-charge mortgage.

FAQ

What are the risks of a collateral mortgage?

The negative aspects of a collateral mortgage are that it can be more difficult to qualify or switch between lenders. Additionally, as the registered mortgage is higher than the actual amount owing – it can limit you from secondary financing.

What is a collateral mortgage loan?

A collateral mortgage is a re-advanceable real estate secured loan that can increase your borrowing capacity without re-qualifying. You can continue to borrow against your home as you pay down your mortgage or as the value of your home rises. In contrast, you would need to refinance with a conventional mortgage to borrow more money, which may incur a penalty if you haven’t completed your mortgage term.

What are the pros and cons of a collateral-charge mortgage?

Pros: If you qualify (and the lender approves), you could borrow more money (up to the registered amount) without having to register another mortgage (saving legal fees).

Cons: It costs more to set up and discharge than a standard mortgage.

What if I refinanced with a collateral mortgage?

By refinancing a collateral mortgage, you’d register a bigger mortgage amount – limited by your property’s updated value and income. Another reason to refinance would be to add or remove anyone from the title on a collateral mortgage. However, you would not need to refinance to increase your amortization. Most collateral charge agreements allow you to return to your originally approved amortization by changing your monthly payment amount.

Final Thoughts

Collateral charge mortgages can be helpful for borrowers looking for greater flexibility in accessing additional funds. For the self-employed, a collateral mortgage offers flexibility with cash flow for business operations, lifestyle needs and investment. Of course, caution is warranted when registering a collateral charge on your home. Before deciding, borrowers should consider this type of mortgage’s potential advantages and disadvantages.

A collateral mortgage may sound tempting, but for most homeowners, a conventional loan offers the simplicity and affordability they need. With its flexibility and ease of use, it’s no surprise that this is one of the top-choice mortgages today, so you can rest assured that your needs are covered.

We advise working with a mortgage expert as it can help borrowers better understand their borrowing options and make informed decisions about their mortgage strategy for their financial circumstances.