Why Inflation Numbers Don’t Reflect the Housing Market

The pandemic has shown phenomenal growth in all types of home valuations throughout North America. Pandemic-related economic disruptions such as demand, surging building costs, and other long-term supply restrictions in the housing market have contributed to record price escalation. In this blog post, we’re going to discuss how inflation and house prices are linked, and what factors contribute to each other’s acceleration into divergent directions.

Key Highlights

- CPI does not fully capture the costs of buying a home, creating a disconnect between housing prices and shelter costs.

- Increases in house prices are not captured by inflation.

- Renting costs can surge even when housing demand and prices wane.

Best Mortgage Rates

What is the relationship between housing prices and CPI inflation?

Housing, which includes different kinds of shelter-related costs, makes up 30% of measurement in the consumer price index (CPI), which directly affects how inflation is measured by the Bank of Canada (BoC). Rising home prices directly affect household wealth and neighbourhood affordability, thus playing an important role in overall inflation.

The costs associated with housing such as owned accommodation, rent, homeowner’s replacement cost, mortgage interest, homeowner insurance & mortgage insurance, and property taxes, make up the biggest portions of the CPI.

CPI, which uses a cost approach as tallied by Statistics Canada (StatsCan), does not include the cost of buying a home or a condo, even though the shelter is the biggest component of the CPI. Owned accommodation makes up the majority of that component and has had double-digit increases nationally from early 2020 until when the BoC started increasing overnight rates. Imagine how much higher the CPI would be if it included the annual housing price gains during that same time.

Why housing price growth and inflation aren’t necessarily linked

The equity gains that come out of housing price growth are considered an asset and CPI does not measure assets. CPI measures consumer costs as part of a basket of goods and services. There are separate indices to measure new housing and mortgage interest – essentially leaving a disconnect on resale property prices as part of the CPI measurement.

As more Canadians started working from home and cash flows started increasing due to lower cost of living, costs for transportation and the need to eat out decreased. Alongside this, mortgage rates had significantly declined and costs to service a mortgage had substantially lowered and housing became more affordable.

This created demand that outweighed supply; however, as CPI was not measuring the increases in resale properties, the impact of these surging house prices was never captured. It wasn’t until supply-related disruptions due to the war in Ukraine and China’s zero COVID policy started affecting other facets of the CPI. It’s when inflation surged on consumer goods, such as fuel, natural gas, house-building supplies, lumber, tools and appliances, that it started affecting other areas of the economy.

Overall household costs are not changed much by housing price increases

Household costs remain unaffected by housing price increases as CPI, respectively, measures one and not the other. StatsCan, which measures the CPI for the federal government and its departments, including the BoC, explains that they take, similar to other developed economies, the “payments approach” to measuring housing costs. Simply put, this would be like asking, “what’s my monthly payment?” for shelter. StatsCan put out a paper back in 2015 discussing an alternative method known as the “net acquisition” approach, which includes measuring the purchase cost of housing price inflation and monitoring monetary policy.

Source: StatsCan Different aspects of shelter costs as part of the total CPI measurement.

Now, where the equation becomes skewed can be illustrated in the following example. Suppose that someone in the 1950s bought their home for $5,000 and today it is worth $900,000, they may have fully paid off their mortgage, so their shelter costs would be next to zero, and they rent out this home to someone who is paying $2000 per month which would be their shelter cost. Whereas if that person never rented it out, there would have been hardly any cost added to the CPI for shelter unless they sold it and the other person had a mortgage payment.

The CPI includes mortgage interest on a weighting of about 4%; however, during the pandemic, mortgage rates fell, causing a downward force on shelter costs. The mortgage cost to carry the home was much lower than today – to be exact, almost 8 times lower since the BoC increased the overnight rate from 0.25% to 3.75%.

Rising rent prices & available real estate can impact housing inflation numbers

As rent prices rise with demand, they directly affect the shelter costs included in the CPI, which calculates inflation. If supply reduces due to a lack of housing available, then rent prices will increase further, thus affecting inflation along with each increase. Monthly shelter costs, which include rent, will affect inflation.

As the housing supply increases and demand increases along with it, prices will increase more gradually. If supply increases and demand decreases, then prices will decrease quite rapidly. Regardless of the supply and demand of houses, the monthly shelter costs affect inflation. As the shelter costs are dependent on rental prices and those are dependent on homeowners’ costs to carry the mortgage payment, it’s a catch-22 with inflation since home price increases are not a part of this equation.

| Housing Supply | Housing Demand | Interest Rates | Housing Price | Rent | Inflation | |

| Pre-pandemic | Decreasing | Increasing | Stable | Stable Increases | Stable Increases | Stable Increase |

| Pandemic | Decreasing | Increasing | Decreasing | Surging | Surging | Surging |

| Currently | Decreasing | Decreasing | Increasing | Plunging | Surging | Surging |

CPI leaves a disconnect between house prices which move appropriately opposite to the overnight rates as the cost to carry a mortgage on a home increases when overnight rates do; however, inflation strays in the opposite direction as rents are swaying it. The above table illustrates our point on how rent prices directly impact inflation

Home buyers substitute costs depending on the current real estate market

Homebuyers will substitute costs depending on the current real estate market between owned accommodation which will account for the mortgage interest and rented accommodation which will account for the full amount of the mortgage principal repayment making up their total mortgage payment every month. As owned accommodation costs only consider the mortgage interest, the homeowner substitutes the mortgage principal repayment as part of the rented accommodation for their shelter costs.

Homebuyers substituted shelter costs are made up of the components of the owned accommodation portion (16%) of the CPI, as well as the following: mortgage interest cost, homeowners’ replacement cost, property taxes and other special charges (such as condominium/maintenance/strata fees), homeowners’ home and mortgage insurance, homeowners’ maintenance and repairs and other owned accommodation expenses.

Relative share in the CPI basket of goods and services

| Components | Percentage (%) of CPI |

|---|---|

| Shelter | 26.8 |

| Rented accommodation | 6.4 |

| Rent | 6.2 |

| Tenants’ insurance premiums | 0.1 |

| Tenants’ maintenance, repairs and other expenses | 0.1 |

| Owned accommodation | 16.1 |

| Mortgage interest cost | 3.5 |

| Homeowners’ replacement cost | 4.8 |

| Property taxes and other special charges | 3.4 |

| Homeowners’ home and mortgage insurance | 1.3 |

| Homeowners’ maintenance and repairs | 1.4 |

| Other owned accommodation expenses | 1.6 |

| Water, fuel and electricity | 4.3 |

| Electricity | 2.4 |

| Water | 0.6 |

| Natural gas | 0.9 |

| Fuel oil and other fuels | 0.3 |

Best Mortgage Rates

Recent inflation numbers and expectations for the future

Recent inflation numbers have stabilized, but they are still not decreasing as expected with the BoC’s overnight rate surges. Canada’s housing market is receding to pre-pandemic levels as higher interest rates scare off potential buyers. However, this effect is not quite showing up in the country’s surging inflation.

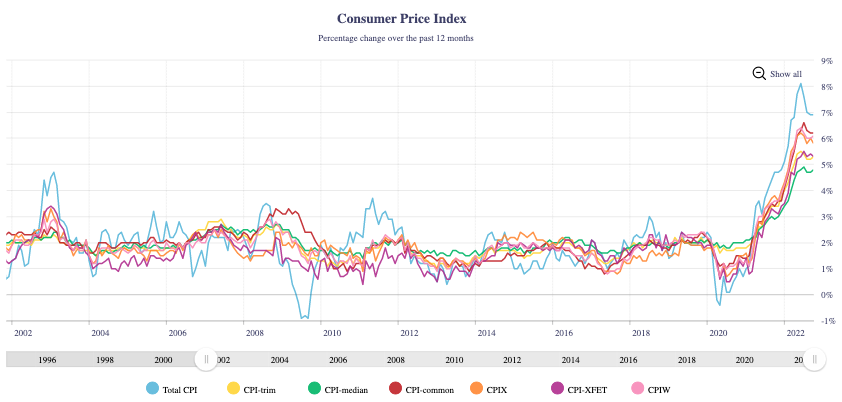

To make matters worse, the cost of owning or renting is putting more pressure on CPI, which rose to 7.4% in April and is now down to 6.9% at the end of October – the largest annual gain since 1983 and nowhere near the BoC’s 2% target. These increases are linked to the housing sector in the form of rising home energy prices and mortgage interest costs. That affects the CPI, with interest rates increasing faster than ever in history. Businesses passed on transporting goods to homeowners and rentals – as they were also affected by rising energy prices. All of these costs directly affect the CPI measurement that is affecting inflation.

Source: Bank of Canada This image shows the recent increases in all CPI measurements for Canada and breaks down the total CPI increases into the trim, medium and common CPIs separately – as well as those we are not concerned about for our purposes here.

FAQ

In this section, we answer some of our clients’ more common questions regarding inflation and home prices.

Will house prices go down with inflation?

No, house prices will move in the opposite direction as inflation – measured by the consumer price index (CPI). The Bank of Canada (BoC) will move mortgage interest rates up with inflation until they can bring inflation back to their 2% target.

What happens to the housing market when inflation goes up?

As inflation rises, so do the costs involved in owning or renting a home. One of the main costs of owning a home is mortgage interest. The BoC will increase mortgage rates to curb inflation. As mortgage interest costs keep rising, it is harder for most borrowers to pass the stress test, thus removing the incentive to purchase a home while inflation is high.

Final Thoughts

Homeownership is an asset, as well as the downpayment that homebuyers save to purchase their home. Unfortunately, these assets are not taken into account as part of the cost of homeownership – making a disconnect with inflationary measures and targets. Interestingly while home prices were skyrocketing during the pandemic, the cost of carrying such large mortgages was only measured as the mortgage interest costs while the overnight rates remained subdued.

Statistics Canada, in its CPI measurements for shelter costs, only tracks the cost of using the home and not acquiring it. The cost of using a home – considered as rent – does not rise as fast as home prices, reducing volatility in the CPI. If CPI measured house prices, and not just for newly built homes, then inflation would have risen much higher and much sooner. They would have given ample opportunity for the BoC to accelerate rate increases early in 2021, thus avoiding the current bubble in the housing market.