How Much House Can I Afford In Quebec City?

Are you interested in buying a house in Quebec City? This capital city has a vibrant culture, beautiful architecture, and countless amenities. Quebec City could be the perfect place to put down roots. Before taking the plunge into homeownership, you may ask yourself: What income do I need to buy a house in Quebec City?

In this blog post, we’ll dive into what personal factors determine how much house you can afford and what financing options are available. We want you to feel empowered, so read below for guidance on determining what could be within reach.

Key Takeaways

- The benchmark price for a home in Quebec City is currently $329,200.

- Affording a home in Quebec City depends on multiple factors, including current interest rates, credit score, down payment amount, and other financial obligations.

- You can generally qualify for a mortgage of around 3.5 to 4 times your annual gross income.

Best Mortgage Rates

How Much Income Do You Need To Afford A Home In Quebec City?

There are various factors to consider when determining how much income is needed to afford a home in Quebec City. Your mortgage term could affect your mortgage rate. Current interest rates will play a significant role when determining affordability. Higher mortgage rates increase overall borrowing costs, affecting affordability meaning your dollar won’t stretch as far as when rates are lower.

Additionally, the stress test will impact the income needed to qualify as it artificially inflates your interest rate to ensure you can still afford the home if interest rates should rise.

Personal factors will also impact what you can afford, such as your credit score, down payment amount, and other debts like credit cards, student loan balances and other financial obligations. Higher credit scores and a larger down payment can give you a better chance of qualifying for a mortgage and obtaining better rates.

Typically, you can qualify for a mortgage between 3.5 to 4 times your gross annual income. According to data from CREA, the benchmark price for a home in Quebec City in April 2023 was $329,200, well below the national average of $716,083 and the provincial average of $477,117. You will need an annual income of approximately $80,000 to afford the benchmark price in Quebec City. However, your qualifying amount will be based on personal factors like your down payment and lender guidelines, such as your debt-to-income ratios.

How Much House Can I Afford With A $70,000 Salary In Quebec City?

If you’re earning a $70,000 salary in Quebec City, a general rule of thumb is that you can qualify for a mortgage of 3.5 to 4 times your annual income. With a $70,000 salary, you can likely afford a mortgage between $245,000 and $280,000.

Based on first-quarter data from Fenêtre Sur Le Marché Immobilier (FSMI), with a $70,000 salary, you could explore purchasing a condo in most of Quebec City’s metropolitan area.

If your down payment permits, you could also explore single-family homes in the Ancien Lévis area of the city.

Buying a house with a $70k salary and great credit

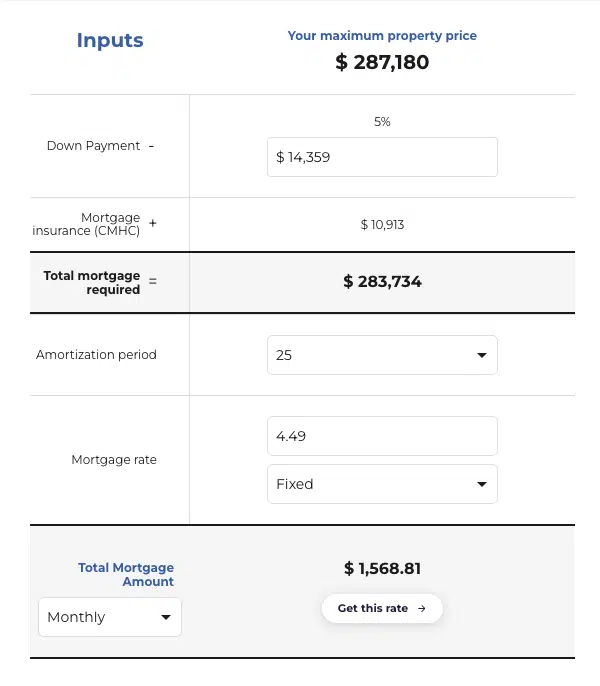

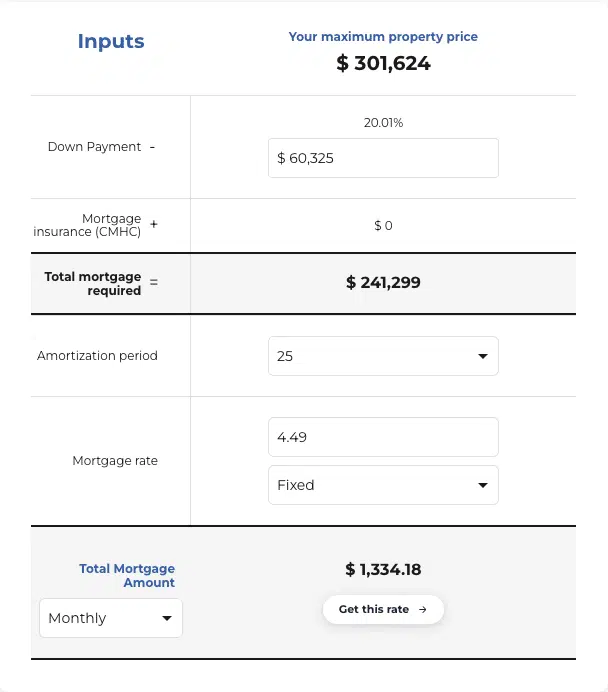

You will qualify for the best rates if you have great credit, with a credit score of at least 680 or above. With current interest rates on a $70,000 salary, you can afford a home with a maximum property price of approximately $287,000 with 5% down and $302,000 with 20% down.

To illustrate how much you can afford with a $70,000 salary and good credit, we used nesto’s mortgage affordability calculator. In this, we have run two scenarios, a 5% down payment and a 20% down payment, to highlight how affordability changes based on your available down payment. Inputs were left with estimates of $2,000 in property taxes and $100 in heating costs and assumed no other debts.

Buying a house with a $70k salary and poor credit

You may need to explore alternative lending options if you have a credit score below 660. It’s important to note that these mortgages will come with much higher interest rates. Interest rates from alternative lenders may be at least 2 to 3% higher than prime lenders and may include a 1% lender fee.

There are also options to get mortgages from private lenders, but they may have interest rates higher than 10% for applicants with poor credit. It’s also important to note that your monthly mortgage payment could double or triple with alternative or private lending as the interest rates are much higher.

The maximum property price you can afford is still approximately $302,000, as a 20% down payment is required for alternative lending. Though with this option, you may be able to extend the amortization up to 40 years, making monthly payments much more affordable. However, extended amortizations will come at the cost of paying more interest over the life of the mortgage.

How Much House Can I Afford With An $80,000 Salary In Quebec City?

If you’re earning an $80,000 salary in Quebec City, a general rule of thumb is that you can qualify for a mortgage of 3.5 to 4 times your annual income. With an $80,000 salary, you can likely afford a mortgage between $280,000 and $320,000.

Based on first-quarter data from Fenêtre Sur Le Marché Immobilier (FSMI), with an $80,000 salary, you could explore purchasing a condo in Quebec City or a single-family home in the Ancien Lévis area of the city.

If your down payment permits, you could also explore single-family homes in the city’s Beauport, La Haute Saint-Charles, and South Shore areas.

Buying a house with an $80k salary and great credit

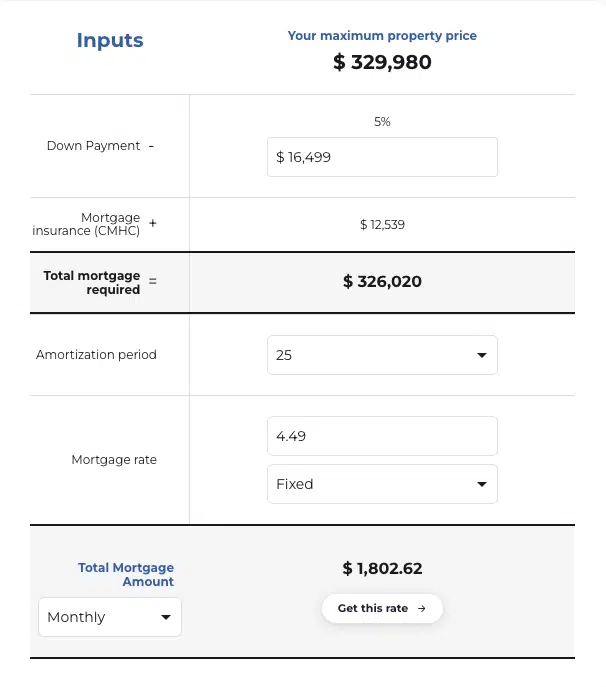

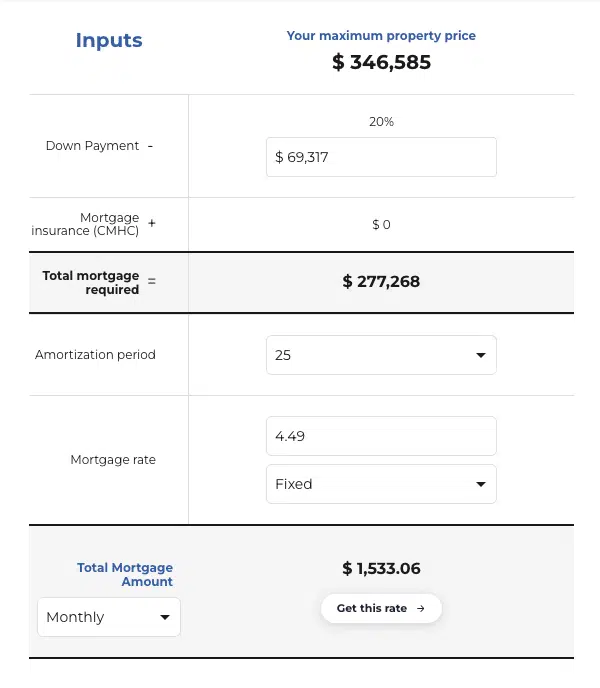

You will qualify for the best rates if you have great credit, with a credit score of at least 680 or above. With current interest rates on an $80,000 salary, you can afford a home with a maximum property price of approximately $330,000 with 5% down and $347,000 with 20% down.

To illustrate how much you can afford with an $80,000 salary and good credit, we used nesto’s mortgage affordability calculator. In this, we have run two scenarios, a 5% down payment and a 20% down payment, to highlight how affordability changes based on your available down payment. Inputs were left with estimates of $2,000 in property taxes and $100 in heating costs and assumed no other debts.

Buying a house with an $80k salary and poor credit

You may need to explore alternative lending options if you have a credit score below 660. It’s important to note that these mortgages will come with much higher interest rates. Interest rates from alternative lenders may be at least 2 to 3% higher than prime lenders and may include an additional 1% lender fee.

There are also options to get mortgages from private lenders, but they may have interest rates higher than 10% for applicants with poor credit. It’s also important to note that your monthly mortgage payment could double with alternative or private lending as the interest rates are much higher.

Buying a home with an $80,000 salary and poor credit won’t affect your qualifying mortgage amount as it will still be around $347,000, as a 20% down payment is required for alternative lending. Though with this option, you may be able to extend the amortization up to 40 years, making monthly payments much more affordable. However, extended amortizations will come at the cost of paying more interest over the life of the mortgage.

How Much House Can I Afford With A $90,000 Salary In Quebec City?

If you’re earning a $90,000 salary in Quebec City, a general rule of thumb is that you can qualify for a mortgage of 3.5 to 4 times your annual income. With a $90,000 salary, you can likely afford a mortgage between $315,000 and $360,000.

Based on first-quarter data from Fenêtre Sur Le Marché Immobilier (FSMI), with a $90,000 salary, you could explore purchasing a condo in Quebec City or a single-family home in the Charlesbourg, Beauport, La Haute Saint-Charles, Ancienne-Lorette, Île-d’Orléans, South Shore, Chutes-de-la-Chaudière-Ouest, Chutes-de-la-Chaudière-Est, and Ancien Lévis area of the city.

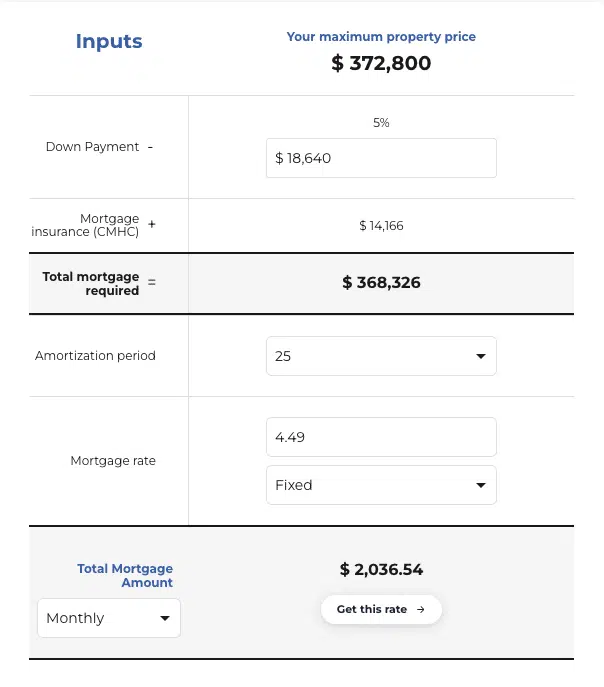

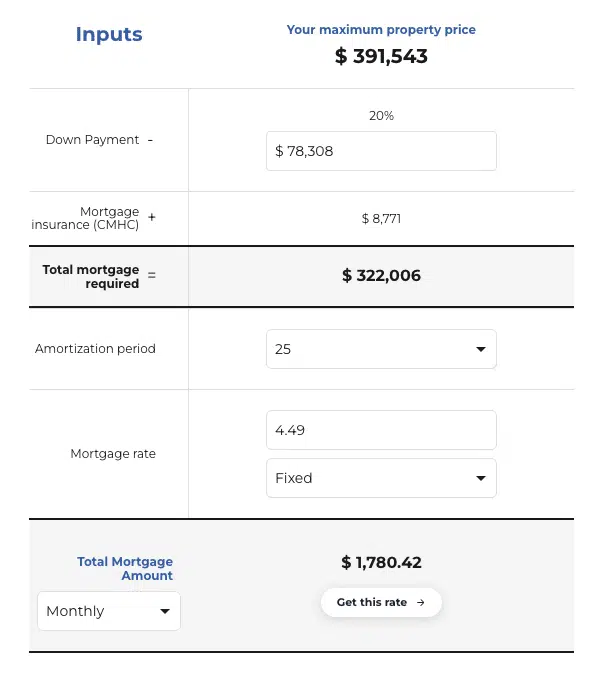

Buying a house with a $90k salary and great credit

You will qualify for the best rates if you have great credit, with a credit score of at least 680 or above. With current interest rates on a $90,000 salary, you can afford a home with a maximum property price of approximately $373,000 with 5% down and $392,000 with 20% down.

To illustrate how much you can afford with a $90,000 salary and good credit, we used nesto’s mortgage affordability calculator. In this, we have run two scenarios, a 5% down payment and a 20% down payment, to highlight how affordability changes based on your available down payment. Inputs were left with estimates of $2000 property taxes and $100 heating costs and assumed no other debts.

Buying a house with a $90k salary and poor credit

You may need to explore alternative lending options if you have a credit score below 660. It’s important to note that these mortgages will come with much higher interest rates. Interest rates from alternative lenders may be at least 2% to 3% higher than prime lenders and may include a 1% lender fee.

There are also options to get mortgages from private lenders, but they may have interest rates as high as 10% for applicants with poor credit. It’s also important to note that your monthly mortgage payment could double with alternative or private lending as the interest rates are much higher.

Buying a home with a $90,000 salary and poor credit won’t affect your qualifying mortgage amount, as it will still be around $392,000, as a 20% down payment is required for alternative lending. Though with this option, you may be able to extend the amortization up to 40 years, making monthly payments much more affordable. However, extended amortizations will come at the cost of paying more interest over the life of the mortgage.

How Much House Can I Afford With A $100,000 Salary In Quebec City?

If you’re earning a $100,000 salary in Quebec City, a general rule of thumb is that you can qualify for a mortgage of 3.5 to 4 times your annual income. With a $100,000 salary, you can likely afford a mortgage between $350,000 and $400,000.

Based on first-quarter data from Fenêtre Sur Le Marché Immobilier (FSMI), with a $100,000 salary, you could explore purchasing a condo in Quebec City or a single-family home in the Charlesbourg, Beauport, La Haute Saint-Charles, Ancienne-Lorette, Île-d’Orléans, South Shore, Chutes-de-la-Chaudière-Ouest, Chutes-de-la-Chaudière-Est, and Ancien Lévis area of the city.

If your down payment permits, you could also expand your search and look for single-family homes in the Les Rivières, Northern Periphery, or La Jacques-Cartier areas of the city.

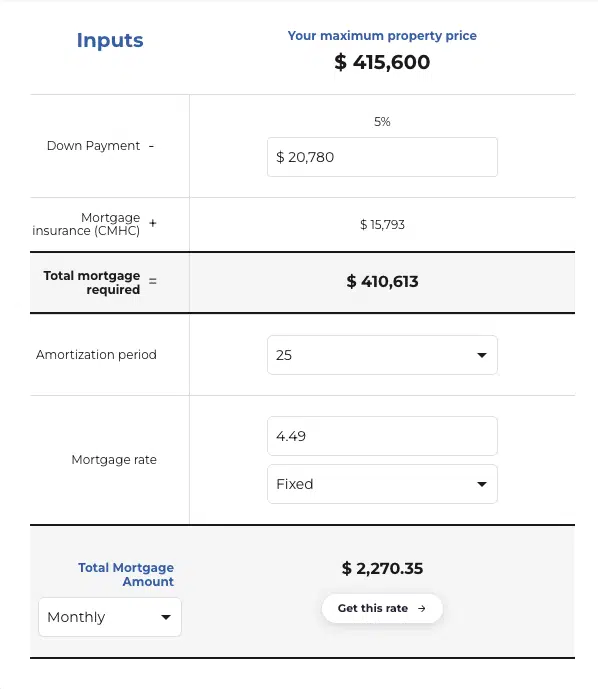

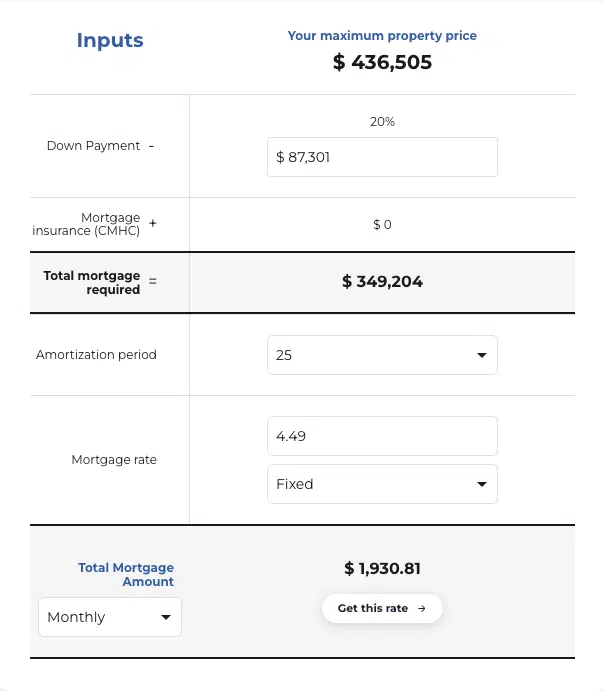

Buying a house with a $100k salary and great credit

You will qualify for the best rates if you have great credit, with a credit score of at least 680 or above. With current interest rates on a $100,000 salary, you can afford a home with a maximum property price of approximately $416,000 with 5% down and $437,000 with 20% down.

To illustrate how much you can afford with a $100,000 salary and good credit, we used nesto’s mortgage affordability calculator. In this, we have run two scenarios, a 5% down payment and a 20% down payment, to highlight how affordability changes based on your available down payment. Inputs were left with estimates of $2000 property taxes and $100 heating costs and assumed no other debts.

Buying a house with a $100k salary and poor credit

You may need to explore alternative lending options if you have a credit score below 660. It’s important to note that these mortgages will come with much higher interest rates. Interest rates from alternative lenders may be at least 2% to 3% higher than prime lenders and may include a 1% lender fee.

There are also options to get mortgages from private lenders, but they may have interest rates as high as 10% for applicants with poor credit. It’s also important to note that your monthly mortgage payment could double with alternative or private lending as the interest rates are much higher.

Buying a home with a $100,000 salary and poor credit won’t affect your qualifying mortgage amount, as it will still be around $437,000, as a 20% down payment is required for alternative lending. Though with this option, you may be able to extend the amortization up to 40 years, making monthly payments much more affordable. However, extended amortizations will come at the cost of paying more interest over the life of the mortgage.

Best Mortgage Rates

Average Salary In Quebec City

The average annual salary for someone living in Quebec City is $55,921. Entry-level roles start at an average annual salary of $38,864, with the most experienced workers making an annual salary of around $132,158. The gross (before tax) average household income currently sits at $93,800.

Factors To Determine Your Home Affordability

Your Credit Score

Your credit score gives lenders an overall picture of your ability to repay all debts consistently and is a strong indicator of your overall financial health. Lenders will use your credit score to assess the amount of risk in lending you money. Generally, the better your credit score, the easier it is to qualify for a mortgage and get a better interest rate.

Your Debt-to-Income Ratio

Debt-to-income ratios test borrowers’ ability to service their total and household debts. There are two ratios Gross Debt Service, or GDS – which measures the ability to manage household debt, and Total Debt Service or TDS – which measures the ability to manage the GDS plus any other debts. On the high-ratio default-insured mortgage side, CMHC guidelines limit the GDS to a maximum of 39% and TDS to a maximum of 44% of the borrower’s income.

Your Savings

How much you have saved and how much you plan to put down as a down payment will affect your affordability and monthly payments. A larger down payment of 20% or more of the purchase price will mean you have a smaller mortgage and lower payments, while a smaller down payment of anything less than 20% will mean you have a larger mortgage and higher monthly payments. You will also be required to purchase mortgage default insurance if you put down less than 20%.

Your Neighbourhood Preferences

Home prices can vary depending on the location, so your preferred neighbourhood may have more expensive homes for sale when compared to other areas of the city. Checking comparables and exploring other neighbourhoods and the real estate they offer can be a great option to find more affordable homes. Sometimes, expanding your search to a few streets can be enough to see a price difference.

Home Financing Options In Quebec City

Choosing A Mortgage Lender

Choosing a lender is just as important as shopping for a home. Lenders can be anything from financial institutions, banks, and credit unions to individuals that provide mortgages. Each lender will have criteria for approval that will vary depending on the type of lender, how they are regulated and their risk appetite. Depending on your qualifying factors, the type of lender you choose may be either a prime, subprime, or private lender.

Choosing To Self-Finance Your Mortgage

If you have the funds to do so and want to avoid going the traditional mortgage route and paying interest, you could pay cash for a home in Quebec City. Of course, this would require that you have significant savings available to purchase the home mortgage free. But the best part is that you won’t have to pay any interest on this money!

Final Thoughts

With benchmark prices currently at $329,200, Quebec City may be one of the more affordable urban centres left to explore if you are looking to purchase a home. Getting a pre-approval or pre-qualification before you start your search can help you figure out exactly how much you could afford so you can start shopping and stay within budget. Speak with one of nesto’s commission-free mortgage experts, who will help guide you through your mortgage financing process.

Why Choose nesto

At nesto, our commission-free mortgage experts, certified in multiple provinces, provide exceptional advice and service that exceeds industry standards. Our mortgage experts are salaried employees who provide impartial guidance on mortgage options tailored to your needs and are evaluated based on client satisfaction and the quality of their advice. nesto aims to transform the mortgage industry by providing honest advice and competitive rates through a 100% digital, transparent, and seamless process.

nesto is on a mission to offer a positive, empowering and transparent property financing experience – simplified from start to finish.

Contact our licensed and knowledgeable mortgage experts to find your best mortgage rate in Canada.