Mortgage Rates Forecast Canada 2026-2030

Canada’s mortgage rate forecast for 2026 suggests borrowing costs will remain relatively stable. The Bank of Canada (BoC) is largely expected to hold the policy interest rate at 2.25% throughout the year. As a result, variable mortgage rates in Canada are expected to remain unchanged, while fixed rates may increase slightly in line with Government of Canada (GoC) bond yields.

Many Canadian borrowers are coming up for renewal for the first time since interest rates began to rise in 2022, and most are likely to see significant increases in their mortgage payments. Borrowers should not expect further rate cuts in 2026 unless trade tensions with the US or global economic conditions significantly affect Canada’s economy.

Key Takeaways

- The Bank of Canada is expected to hold the policy rate near 2.25% in 2026.

- Fixed mortgage rates will likely remain stable but may rise slightly if bond yields rise.

- Many borrowers renewing mortgages in 2026 will face higher monthly payments.

Best Mortgage Rates

Why Mortgage Renewals in 2026 Could Mean Higher Payments for 33% of Borrowers

By the end of 2026, approximately 33% of Canadian mortgage holders are expected to face higher monthly mortgage payments. Approximately 75% of borrowers facing a payment increase have 5-year fixed-rate mortgages. For those with fixed-rate mortgages renewing in 2026, payment increases are expected to average around 20%. This reflects the shift from ultra-low pandemic-era rates to today’s higher borrowing costs.

The experience will differ substantially for borrowers with variable mortgages. Those with adjustable-rate mortgages (ARM) have already absorbed most of the impact of past rate hikes and, based on current expectations for 2026 interest rates, many could begin to see some payment relief.

However, borrowers with variable-rate mortgages (VRM) may experience significant changes in their mortgage payments. 10% of borrowers renewing a variable-rate mortgage are projected to see payments rise by more than 40%. In comparison, roughly 25% could see their payments fall by at least 7%. This wide range largely reflects borrowers’ strategies for managing rising rates during the tightening cycle. Borrowers who increased their monthly payments to ensure principal and interest were covered are likely to face smaller adjustments at renewal. Meanwhile, borrowers experiencing negative amortization are likely to experience larger increases in their mortgage payments at renewal.

As of mid-2026, that stress is starting to show in the data. Equifax Canada’s first-quarter 2026 Market Pulse reported that mortgage delinquency balances were up about 32% from a year earlier nationally, and 52% higher in Ontario. However, the share of mortgages 90 or more days behind remains low at roughly 0.2%. Consumer insolvencies climbed to their highest level since 2009. Statistics Canada’s national balance sheet also shows the total dollar value of mortgage interest paid by households rising as renewals take hold, even though the mortgage interest costs (MIC) component of the Consumer Price Index has eased year over year. The two series measure different data, aggregate dollars paid versus the average annual price change, so both can move at once.

Canada Mortgage Rate Forecast for 2026 (Updated July 2026)

Canada’s mortgage rate outlook for 2026 depends largely on how quickly inflation stabilizes and how the Bank of Canada responds to current economic conditions. Most economists at Canada’s largest banks expect borrowing costs to remain relatively stable over the year. However, mortgage rates could fluctuate throughout the year as economic data changes and financial markets adjust their expectations. Growth has been uneven in 2026: real GDP was essentially flat in the first quarter before rebounding 0.5% in April, the strongest monthly gain since July 2025. The Bank of Canada’s July Monetary Policy Report estimated that growth resumed in the second quarter at an annualized pace of about 2.5%, while a preliminary Statistics Canada estimate points to a further 0.1% gain in May, and Canada’s merchandise trade surplus widened to a 4-year high of about $4.2 billion. Economists surveyed by Bloomberg have trimmed their 2026 growth expectations to around 0.7%, in line with the Bank’s own July projection.

Bank of Canada Policy Rate Forecast (Variable Rates)

Forecasts from the Big 6 Banks suggest that the overnight policy rate will remain stable at 2.25% for much of the year. By the end of 2026, most major banks predict rates will end the year at the same level as they began.

| Bank | Jun | Jul | Sep | Oct | Dec |

|---|---|---|---|---|---|

| BMO | 2.25% | 2.25% | 2.25% | 2.25% | 2.25% |

| CIBC | 2.25% | 2.25% | 2.25% | 2.25% | 2.25% |

| National Bank | 2.25% | 2.25% | 2.25% | 2.50% | 2.75% |

| RBC | 2.25% | 2.25% | 2.25% | 2.25% | 2.25% |

| Scotiabank | 2.25% | 2.25% | 2.25% | 2.50% | 2.75% |

| TD | 2.25% | 2.25% | 2.25% | 2.25% | 2.25% |

Government of Canada 5-Year Bond Yield Forecast (Fixed Rates)

Most forecasts from the Big 6 Banks expect bond yields to remain relatively stable through 2026. GoC 5-year bond yields are expected to rise from a low near 3% early in the year to around 3.25% by the end of 2026. As a result, fixed mortgage rates could gradually increase, although large increases are unlikely. Fixed mortgage rates in Canada may fluctuate modestly throughout the year as financial markets react to inflation and employment data, as well as shifts in global bond markets. Still, the overall trend is for rates to remain relatively stable. In early July, the 5-year GoC yield spiked to about 3.18%, a seven-week high, as renewed US-Iran tensions pushed oil and US Treasury yields up, before easing back to roughly 3.13% by July 10. The main upward pressure on Canadian fixed rates has been imported rather than domestic, a dynamic explained further below.

| Bank | Q2 2026 | Q3 2026 | Q4 2026 |

|---|---|---|---|

| BMO | 3.15% | 3.05% | 2.95% |

| CIBC | 3.00% | 3.15% | 3.25% |

| National Bank | 3.20% | 3.15% | 3.15% |

| RBC | 3.10% | 3.20% | 3.30% |

| Scotiabank | 3.01% | 3.15% | 3.25% |

| TD | 3.10% | 3.00% | 2.95% |

Will Interest Rates Go Down in 2026?

The BoC Policy Rate decreased by 100 basis points (1 basis point equals 0.01%) in 2025. The Bank of Canada is expected only to consider further rate cuts if the economy shows significant weakness in 2026.

So far, most of the Big 6 Banks expect the policy rate to hold steady through 2026. Scotiabank and National Bank are the exceptions, with both projecting the rate rising to 2.75% by the end of 2026.

Changes in Government of Canada bond yields influence fixed mortgage rates, which respond to financial market expectations. Currently, market expectations suggest that rates, in particular the 5-year fixed rate, could increase slightly.

After April’s growth rebound, economists broadly reaffirmed the hold: CIBC expects no change to the policy rate in 2026, and Capital Economics said the rebound should put the recession debate to rest while leaving any rate hikes some way off.

Will There Be a Bank of Canada Rate Hike in 2026?

Most rate analysts predict that rates will stabilize and remain constant throughout 2026. The Bank of Canada Governing Council considers the current policy rate adequate to keep inflation around the 2% target and to support the economy. However, uncertainty remains high, and the outlook could shift in response to global economic developments.

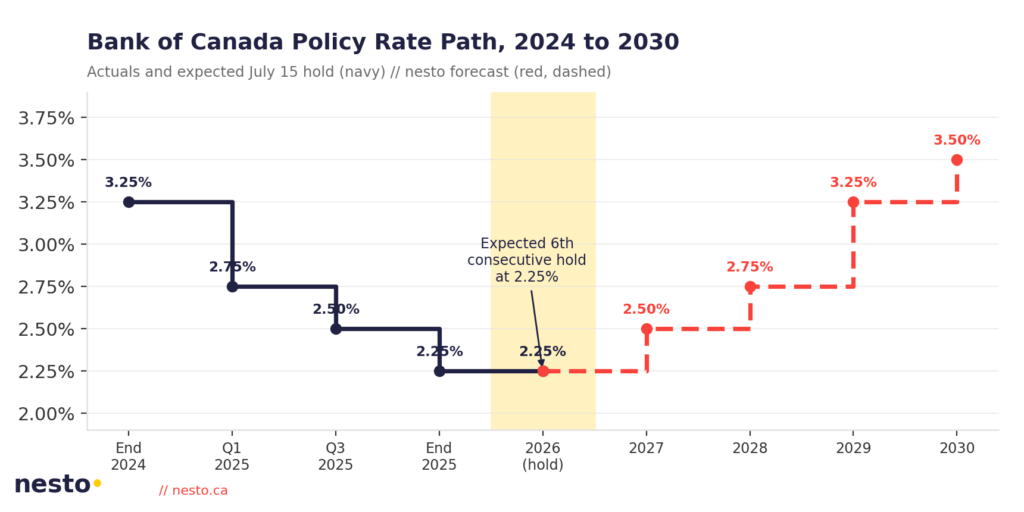

As of July 13, bond markets implied about a 91% chance of a rate hold on July 15, with the odds of a quarter-point hike climbing only gradually and reaching roughly a coin flip by the December meeting. That hold was confirmed: the Bank of Canada kept the policy rate at 2.25% on July 15 for a sixth consecutive time, alongside its quarterly Monetary Policy Report. In its June 10th Summary of Governing Council Deliberations, the Bank had signalled it would stay nimble, and its July 15 opening statement reaffirmed that stance: uncertainty remains elevated, with the re-escalation of the Middle East conflict and ongoing US trade discussions cited as the two main swing factors that could still move the Bank in either direction.

Fixed vs Variable Mortgage Rate Outlook in Canada

The outlook for fixed and variable mortgage rates in Canada can differ because each responds to economic forces at different times. Fixed mortgage rates tend to move first when financial markets anticipate changes in the economic outlook. Variable mortgage rates adjust after the Bank of Canada changes its policy rate.

Why Fixed and Variable Mortgage Rates Move Differently in Canada

Fixed mortgage rates are primarily influenced by the Government of Canada (GoC) bond yields of corresponding maturities. These bond yields move daily in response to global market conditions, US Treasury yields, economic growth outlooks, inflation expectations, and shifting expectations for policy rate decisions. If bond yields move in either direction, fixed mortgage rates follow.

Variable mortgage rates move more directly with the Bank of Canada’s overnight policy rate. The Bank reviews its policy rate at scheduled announcements 8 times a year, but can make unscheduled announcements at any time in response to a major or unexpected economic shock. When the policy rate changes, lenders typically adjust their prime lending rates within a day of the announcement.

As of mid-2026, that transmission has been the main upward risk to Canadian fixed rates. US headline inflation reached 4.2% in May. The US Federal Reserve held its benchmark rate at 3.50% to 3.75% on June 17th while signalling that its next move could be a hike, which has kept US Treasury yields, and by extension Canadian bond yields, elevated even though Canadian core inflation sits near the 2% target. By July 10th, that pressure had pushed the 5-year Government of Canada (GoC) bond yield back toward 3.13%.

Top Economist’s Mortgage Predictions for 2026

The Bank of Canada’s (BoC) latest Market Participant Survey, which gathers and publishes the views of senior economists and strategists in the Canadian financial market, indicates that rate cuts may have ended and will remain unchanged for the remainder of the year.

Results from the most recent Q1 2026 survey suggest we have seen the end of rate cuts. Rates are predicted to remain at 2.25% for 2026, with the first increase widely expected only in the second quarter of 2027. This 2.25% rate falls within the lower end of the neutral rate range, where interest rates neither stimulate nor restrict the economy. The Bank’s own next Market Participants Survey is scheduled for July 27, 2026.

Policy Interest Rate Forecast

| 2026 | Policy Interest Rate (median response) |

|---|---|

| June | 2.25% |

| July | 2.25% |

| September | 2.25% |

| October | 2.25% |

| December | 2.25% |

5-Year Canadian Bond Yield Forecast

| 2026 | 5-Year Canadian Bond Yield (median response) |

|---|---|

| December | 3.10% |

nesto’s Policy Interest Rate Forecast for Canada 2026

| Policy Rate | |

|---|---|

| Q2 | 2.25% |

| Q3 | 2.25% |

| Q4 | 2.25% |

July 2026 Canada Mortgage Rates Forecast

On July 15, the Bank of Canada held its target for the overnight rate at 2.25% for the sixth consecutive decision, leaving the prime rate unchanged at 4.45%. The backdrop looks steadier than it did in the spring: growth rebounded to an estimated 2.5% in the second quarter, and unemployment held at 6.5% in June, within the 6.5% to 7% range it has occupied since late 2024. Inflation is the piece still working itself out. The Middle East conflict has kept oil prices volatile, pushing headline inflation to 3.2% in May, while core measures remained closer to 2%. The Bank expects inflation to ease to about 2.5% in the second half of 2026 and return to the 2% target by early 2027. Governor Tiff Macklem put it plainly:

We will not let higher oil prices become persistent inflation.

Unlike recent statements, the Bank dropped its explicit language on possible consecutive hikes or a trade-driven cut, a sign it now sees the risks as more balanced than pointed in either direction. Bond markets price a high probability of no change on September 2, with a 11% probability of a 25-basis-point hike. By October 28, markets imply a 40% chance of a hike. Read the full Opening Statement and our post-announcement mortgage strategy breakdown for what this means for Canada’s mortgage rates forecast.

Bank of Canada Interest Rate Expectations for 2026

On July 15, the Bank of Canada held the policy rate at 2.25% for a sixth consecutive time, exactly as every one of the 36 economists in a July Reuters poll had expected. The decision came alongside the Bank’s quarterly Monetary Policy Report, which showed a more constructive read of the economy than the April report: after stalling for much of the past year, GDP growth is estimated to have resumed in the second quarter at an annualized pace of about 2.5%, even though the Bank held its full-year 2026 growth projection at 0.7%, rising to 1.8% in both 2027 and 2028. June’s Labour Force Survey, the Bank’s last major economic read before the meeting, had already pointed to a labour market that is steadying rather than deteriorating, and with the Bank’s core inflation measures near the 2% target, the Bank is widely expected to keep the policy rate on hold for much of the rest of 2026.

As a result, any rate adjustments in 2026 are expected to be gradual and measured, aimed at fine-tuning rather than delivering broad-based relief or tightening. For mortgage borrowers, this indicates that while borrowing costs may edge lower for some over time, they are unlikely to return to pre-pandemic lows.

The Bank of Canada has also pushed back on recession fears, describing the economy as weak and in excess supply but not in recession. Among the big banks, RBC expects no policy rate moves in 2026, with the Bank beginning to raise rates in 2027.

Bank of Canada 2026 Rate Announcement Schedule

| Date | BoC Rate Decision (%) | Target Rate |

|---|---|---|

| January 28 | No Change | 2.25% |

| March 18 | No Change | 2.25% |

| April 29 | No Change | 2.25% |

| June 10 | No Change | 2.25% |

| July 15 | No Change | 2.25% |

| September 2 | TBD | TBD |

| October 28 | TBD | TBD |

| December 9 | TBD | TBD |

Bank of Canada 2025 Rate Announcement Schedule

| Date | BoC Rate Decision (%) | Target Rate |

|---|---|---|

| January 29 | -0.25 | 3.00% |

| March 12 | -0.25 | 2.75% |

| April 16 | No Change | 2.75% |

| June 4 | No Change | 2.75% |

| July 30 | No Change | 2.75% |

| September 17 | -0.25 | 2.50% |

| October 29 | -0.25 | 2.25% |

| December 10 | No Change | 2.25% |

What Affects the Bank of Canada’s Future Rate Decisions?

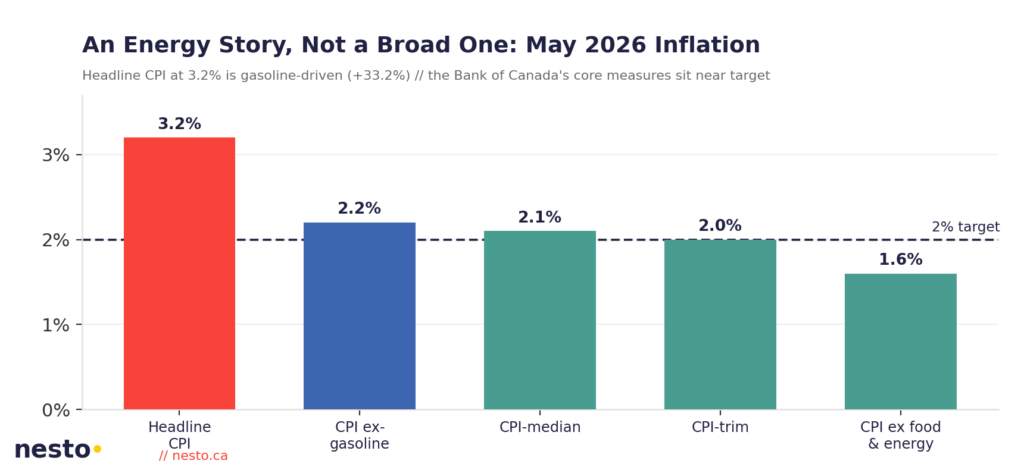

Inflation

Inflation rose 3.2% year-over-year, up from the 2.8% increase in April. Higher gasoline prices drove this increase due to the conflict in the Middle East. Supply uncertainty from the conflict put upward pressure on gasoline prices for the third consecutive month. Gasoline prices rose 33.2%, up from 28.6% in April. Excluding gasoline, CPI rose 2.2% in May, up from 2.0% in April. The Bank’s preferred core measures stayed near target, with CPI-trim at 2.0% and CPI-median at 2.1%, and CPI excluding food and energy at 1.6%, so the headline jump was largely an energy story rather than broad-based inflation. Shelter inflation eased to 1.7% and mortgage interest costs stayed slightly below last year’s levels. That is why the Bank has said it is looking through the oil-driven spike. The Bank’s July Monetary Policy Report confirmed that view, expecting CPI inflation to stay elevated in June before easing gradually and returning to around 2% in early 2027, provided oil and gasoline prices behave as assumed.

Inflation is the most important driver of the BoC’s rate decisions. To achieve its 2% inflation target, the BoC must adjust its policy interest rates to control inflation.

When inflation rises above this target, the Bank of Canada (BoC) increases the policy rate. In turn, commercial banks and lenders raise their prime rates, which directly affect loan and mortgage rates. This discourages borrowing and spending, supporting the BoC’s efforts to return inflation to its 2% target.

If inflation falls below the 2% target, the BoC might lower the policy interest rate to stimulate the economy. Lenders, in turn, decrease their prime rates to encourage borrowing and spending.

Consumer Price Index (CPI) Release Dates 2026

| Date | CPI (Year-over-Year Change) |

|---|---|

| January 19 | +2.4% |

| February 26 | +2.3% |

| March 16 | +1.8% |

| April 20 | +2.4% |

| May 19 | +2.8% |

| June 22 | +3.2% |

| July 20 | TBD |

| August 17 | TBD |

| September 14 | TBD |

| October 19 | TBD |

| November 16 | TBD |

| December 14 | TBD |

Employment

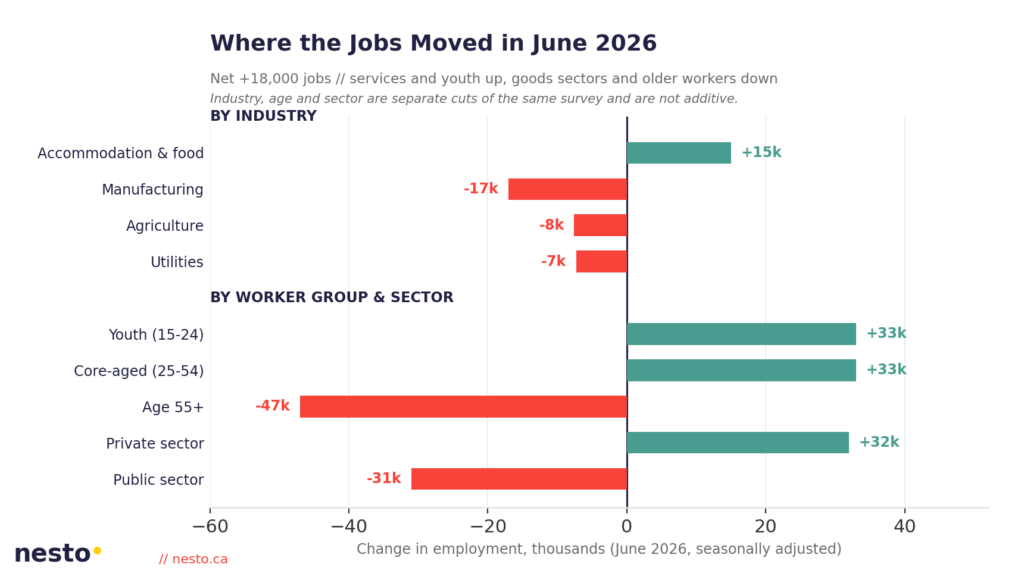

Canada added 18,000 jobs in June 2026, and the unemployment rate slipped to 6.5% from 6.6% in May, according to Statistics Canada’s Labour Force Survey released July 10. It was the second straight monthly decline in the jobless rate, matching January’s level and marking the lowest reading in nearly two years, well down from last year’s peak of 7.1%. As this was the Bank of Canada’s last major economic report before the July 15 decision, it carried extra weight, and it pointed to a labour market that is steadying rather than strengthening. The Bank’s own July Monetary Policy Report confirmed the 6.5% June rate and noted the unemployment rate has hovered in a range of 6.5% to 7% since the end of 2024.

The gain was modest by historical standards, sitting below the 10-year average monthly increase of about 27,000, and the composition was soft. Almost all of the growth came from part-time work, and the employment rate edged up just 0.1 percentage points to 60.8% while the participation rate held at 65.0%. Full-time employment among workers aged 25 and older, the segment most tied to mortgage demand, actually slipped by about 7,000. Total hours worked still rose 0.2% on the month and were up at roughly a 0.9% annual rate across the second quarter, another signal that economic growth rebounded last quarter.

Younger workers did most of the lifting. Youth aged 15 to 24 added 33,000 jobs, mostly part-time, and their unemployment rate fell 0.7 percentage points to 12.7%, following a 0.9-point drop in May. A friendlier summer-student market helped: the jobless rate for returning students was 15.3%, down from 17.4% a year earlier, though it ranged widely, from 8.2% for those aged 20 to 24 to 30.6% for 15- and 16-year-olds. Several economists tied the strength in hospitality hiring to the FIFA World Cup that Canada co-hosted in June, with accommodation and food services adding 15,000 jobs for a third straight monthly gain, concentrated in Quebec and Ontario.

The weak spots were the tariff-exposed sectors of the economy. Manufacturing shed 17,000 positions and is now down roughly 61,000 since its January 2025 peak, as US tariffs continue to weigh on the sector. Construction fell by about 13,000, and agriculture and utilities also lost jobs. The public sector gave back 31,000 positions, offset by a 32,000 gain in private-sector employment. Over the past year, employment has increased by 99,000, with growth concentrated in the private sector.

Wages picked up. Average hourly wages rose 3.3% from a year earlier to $37.20, up from 3.0% in May; a separate series for permanent employees ran hotter at about 3.7%, so the figure you cite depends on the series. Regionally, Quebec had one of the lowest unemployment rates in the country at 5.4%, with the Montreal area easing to 5.9%, while Ontario held at 7% and British Columbia dipped to 6.5%.

Economists read the report as directionally encouraging but far from a boom. RBC’s Nathan Janzen noted the improvement was led by the pullback in youth unemployment on a better summer job market, and the bank expects the jobless rate to drift lower through the year as population growth slows. Scotiabank’s Derek Holt argued the 6.5% rate overstates the slack: measured using stricter US labour-force concepts, he estimates Canada’s rate would be closer to 5.1%, which would put the country near full employment. BMO’s Douglas Porter graded the report as decent but not robust and reaffirmed that the Bank should stay on hold at the July decision and through the rest of the year, a call the Bank’s July 15 hold bore out. Either way, the takeaway for rates is the same. A steadying jobs market gives the Bank of Canada little reason to cut, while lingering slack and soft goods-sector hiring give it little reason to hike, which is why almost every economist expected, and got, a hold on July 15.

BoC rate decisions aim to support maximum sustainable employment levels, maintain output growth, keep inflation predictable and stable, and stimulate the economy. For the economy to maintain inflation at the 2% target, it needs to maintain its maximum sustainable level of employment. This means the economy operates at its highest productive capacity and can sustain itself without triggering inflation.

When employment falls below the maximum sustainable level, people cannot find work and their earnings and savings decline. This affects spending habits, pushing inflation lower, possibly below the 2% target. When employment exceeds this level, employers struggle to find enough workers to meet demand, driving prices and wages higher and increasing inflation. Finding the right balance between inflation and the employment rate is challenging, as both are measured using data from the previous month rather than in real time.

The US Economy

The latest data from the US Bureau of Labor Statistics show that US headline CPI rose 4.2% year over year in May, a multi-year high largely driven by energy costs, while core CPI, excluding food and energy, was 2.9%. On June 17th, the US Federal Reserve held its benchmark rate at 3.50%-3.75% and, in a more hawkish set of projections, signalled that its next move could be a hike rather than a cut. That stance, under new Fed Chair Kevin Warsh, has kept US Treasury yields elevated. Since Canadian bond yields tend to track US Treasury yields, this backdrop is a key reason Canadian fixed mortgage rates are facing upward pressure, even though domestic inflation remains near target. The Bank of Canada’s July Monetary Policy Report put US growth at about 2.5%, driven mainly by strong consumption and booming AI-related investment, and flagged that US bond yields have risen while Canadian yields have been little changed, a differential that has contributed to the Canadian dollar’s depreciation.

Tariffs and How They Influence Interest Rates in Canada

Trade tensions and tariff announcements may seem far removed from mortgage rates, but they play a direct role in shaping borrowing costs. Since early 2025, the US has imposed significantly higher tariffs on Canadian goods. Recent trade tensions between the US and Canada add a layer of complexity for inflation and monetary policy decisions. The Bank of Canada often responds by keeping policy rates higher for longer or delaying planned rate cuts to prevent consumer prices from climbing further.

The picture grew more uncertain over the summer. On July 1, the US declined to renew CUSMA (also known as USMCA) for a further 16-year term at its first joint review, leaving the agreement in force until 2036 but subject to annual reviews and a longer stretch of trade uncertainty for Canadian exporters. Around the same time, renewed US-Iran tensions sent oil prices swinging, with benchmark crude jumping about 7% in the week of July 8 after a period of relative calm. The Bank of Canada’s July 15 Monetary Policy Report noted that, despite the now-annual CUSMA reviews, more Canadian businesses report finding ways to navigate through the uncertainty, and that government spending is also contributing to higher economic activity over the projection.

Here’s why tariffs matter for Canadian mortgage rates:

- These tariffs increase the costs of imported materials and intermediate goods (for example, metals, automotive parts, and machinery) used in Canadian production. Higher costs translate into stronger inflationary pressures, which in turn can make the Bank of Canada (BoC) more reluctant to cut its policy rate.

- Tariffs on Canadian exports to the US, such as steel, lumber, or manufactured goods, raise costs and slow demand for Canadian producers. This slowing demand for Canadian products can lead to weaker business investment, lower exports, and a hit to Canada’s overall economic growth, moderating the impact of retaliatory import tariffs on inflation.

- Uncertainty around trade and tariff threats can also increase the risk premium investors demand on Canadian-dollar assets. This tends to widen the gap between global interest rates, US yields, and Canadian yields, resulting in higher long-term mortgage rates in Canada.

- If trade talks progress and tariffs are eased, inflationary pressures may ease, and the BoC may gain more flexibility to reduce borrowing costs.

Impact on Canadian Mortgages

Tariff-related price pressures can ripple through the economy, affecting all types of borrowers. When tariffs increase the cost of imported goods and materials, they often feed into broader inflation, which could prompt the BoC to keep borrowing costs elevated for longer.

For first-time homebuyers, higher inflation can make it harder to qualify for a mortgage, increase the total cost of borrowing and push monthly payments higher. Lenders may tighten qualification ratios, further limiting how much buyers can borrow.

For renewers, elevated interest rates mean limited opportunities for meaningful rate relief at renewal. Many borrowers coming off historically low rates may see noticeable increases in monthly payments as fixed and variable rates remain elevated.

For refinancers, higher borrowing costs can reduce or eliminate the benefit of consolidating high-interest debt or tapping into home equity. Until inflation pressures linked to tariffs ease, homeowners may find fewer favourable options when restructuring their mortgage.

What Canada’s Mortgage Rate Forecast Means for Borrowers

Higher borrowing costs have already weighed on consumer demand, and mortgage rates are expected to remain relatively stable throughout 2026. Bond yields may still experience periodic upticks, especially if economic data remains better than expected. This could limit the speed at which lenders adjust their fixed mortgage rates.

Mortgage renewals will remain a significant source of pressure in 2026. A large share of borrowers will be renewing mortgages taken out when the Bank of Canada policy rate was at or below 1%. For these households, renewal rates will be materially higher than they have been, increasing the risk of a mortgage payment shock.

This adjustment is expected to place ongoing strain on household budgets and could continue to dampen housing demand, particularly among fixed-rate borrowers facing sharp payment resets. However, rising costs could also tame the inflation outlook as shelter and mortgage interest costs feed into Canada’s CPI.

Fresh data shows how this is playing out for Canadian mortgage holders and borrowers. The Bank of Canada’s Financial Stability Report estimates that a minority of borrowers, roughly 4% nationally and closer to 9% in the Toronto area, may not qualify to refinance at 2027 rates and prices. However, most can still renew with their existing lender. Being unable to refinance is not the same as defaulting; it will just leave households carrying on without a solution to their tight credit obligations. Household debt relative to disposable income also remained elevated at 179.6% in the first quarter, marking its sixth consecutive quarterly increase, leaving less room to absorb higher payments.

Mortgage Rate Predictions 2027 to 2030

While it’s nearly impossible to predict the exact path of interest rates, most economists broadly agree that interest rates are likely to stabilize as inflation remains under control and within the target range. Higher borrowing costs will touch more households, particularly as borrowers who locked in historically low rates continue to renew at much higher rates. This renewal wave is expected to weigh on household budgets and temper housing demand and inflation, as shelter and mortgage interest costs feed into the consumer price index (CPI).

Looking beyond 2026, the outlook is shaped by slower rate cuts and a gradual normalization of rates, with modest adjustments reflecting economic conditions rather than the emergency policy measures to which we have become accustomed. This sets the stage for a multi-year environment in which mortgage rates remain closer to historical norms, making long-term planning more essential than short-term rate timing. Consensus forecasts see the Bank holding the policy rate at 2.25% through 2026 before beginning to raise it in the second quarter of 2027, with RBC, for example, projecting a series of quarter-point increases through 2027.

Canada Policy Interest Rate Forecast 2027

| Bank | Q1 2027 | Q2 2027 | Q3 2027 | Q4 2027 |

|---|---|---|---|---|

| BMO | 2.25% | 2.25% | 2.25% | 2.25% |

| CIBC | 2.25% | 2.50% | 2.75% | 2.75% |

| National Bank | 2.50% | – | – | 2.75% |

| RBC | 2.50% | 2.75% | 3.00% | 3.25% |

| Scotiabank | 3.00% | 3.00% | 3.00% | 3.00% |

| TD | 2.25% | 2.25% | 2.25% | 2.25% |

Government of Canada 5-Year Bond Yield Forecast 2027

| Bank | Q1 2027 | Q2 2027 | Q3 2027 | Q4 2027 |

|---|---|---|---|---|

| BMO | 2.90% | 2.95% | 2.95% | 2.95% |

| CIBC | 3.30% | 3.35% | 3.40% | 3.45% |

| National Bank | 3.10% | – | – | 3.05% |

| RBC | 3.40% | 3.45% | 3.50% | 3.50% |

| Scotiabank | 3.35% | 3.35% | 3.35% | 3.35% |

| TD | 2.90% | 2.90% | 2.90% | 2.90% |

Bank of Canada Market Participants Survey Quarterly Forecast 2027 to 2028

The Bank of Canada’s forecast extends to 2027 and 2028, providing an outlook for future interest rates.

| 2027 | Policy Interest Rate (median response) |

|---|---|

| January | 2.25% |

| March | 2.50% |

| Q2 | 2.50% |

| Q3 | 2.50% |

| Q4 | 2.75% |

| 2028 | |

| Q1 | 2.75% |

| Q2 | 2.75% |

| 2027 | 5-Year Canadian Bond Yield (median response) |

|---|---|

| December | 3.28% |

nesto’s Policy Interest Rate Forecast for Canada 2027 to 2030

| Policy Rate | |

|---|---|

| Q1 2027 | 2.50% |

| Q2 2027 | 2.50% |

| Q3 2027 | 2.50% |

| Q4 2027 | 2.50% |

| Q1 2028 | 2.75% |

| Q2 2028 | 2.75% |

| Q3 2028 | 2.75% |

| Q4 2028 | 2.75% |

| Q1 2029 | 3.00% |

| Q2 2029 | 3.00% |

| Q3 2029 | 3.00% |

| Q4 2029 | 3.25% |

| Q1 2030 | 3.25% |

| Q2 2030 | 3.25% |

| Q3 2030 | 3.25% |

| Q4 2030 | 3.50% |

We’re curious…

Are you a first-time buyer?

Frequently Asked Questions (FAQ) About Mortgage Rate Forecasts in Canada

Will mortgage interest rates go down in 2026?

The Bank of Canada held its policy rate at 2.25% on July 15, 2026, for a sixth consecutive time, and mortgage rates are expected to remain stable for the rest of the year rather than decline.

How much will interest rates rise in the next 5 years?

Most forecasts indicate that interest rates will remain within a more normalized range rather than increase or decrease significantly. However, it is difficult to predict how rates will change over the next five years, as domestic and foreign inflationary pressures influence the BoC’s decisions to raise or lower rates. One of the most significant factors in the long-term inflation battle is the cost of living, which will continue to rise as our population grows and ages.

How will my mortgage payment be affected if it comes up for renewal in 2026?

For most borrowers renewing in 2026, mortgage payments are likely to be higher than at the time of origination. Borrowers who locked in fixed rates in 2021 should expect noticeable increases in their payments. Those with fixed rates could see an increase of approximately 20%. In comparison, those with variable rates could see increases ranging from 7% to 40%, depending on whether they took an adjustable-rate mortgage (ARM) or a variable-rate mortgage (VRM).

When is the best time to get a mortgage?

The best time to get a mortgage is when your finances are stable, your credit is strong, and you have saved enough for a down payment and closing costs. Mortgage rates can change quickly and are difficult to predict with accuracy, so timing the market is rarely a reliable move.

Should I wait for rates to drop before buying?

Waiting for mortgage rates to drop can be risky because forecasts can change, and lower rates are not guaranteed. Lower rates can also increase buyer demand and push home prices higher. If you buy when you are financially ready, and mortgage rates decline, you may be able to switch from a variable rate to a fixed rate, choose a shorter-term fixed rate, blend your mortgage, or refinance to take advantage of lower borrowing costs.

Final Thoughts

Mortgage rates will fluctuate, as they have since the invention of mortgages. Ultimately, it’s not the rate that matters, but how much of your disposable income goes toward servicing this obligation. Your goal should be to keep your mortgage payments predictable, manageable within your budget, and feasible over the long term, aligning with your unique needs and long-term financial plans. In the market, rates are expected to stabilize and are unlikely to return to historic lows; flexibility, predictability, and long-term planning matter more than short-term timing of rates.

Mortgage decisions in today’s rate environment require more than guesswork. Reach out to nesto mortgage experts for transparent advice to help you navigate your rate options and long-term mortgage planning.

Why Choose nesto

At nesto, our commission-free mortgage experts, certified in multiple provinces, provide exceptional advice and service that exceeds industry standards. Our mortgage experts are salaried employees who provide impartial guidance on mortgage options tailored to your needs and are evaluated based on client satisfaction and the quality of their advice. nesto aims to transform the mortgage industry by providing honest advice and competitive rates through a 100% digital, transparent, and seamless process.

nesto is on a mission to offer a positive, empowering and transparent property financing experience – simplified from start to finish.

Contact our licensed and knowledgeable mortgage experts to find your best mortgage rate in Canada.