Managing Payment Shock – A nesto Guide To Mortgage Renewal

Renewing your mortgage can be an exciting yet nerve-wracking experience. Mortgage renewals can bring about significant changes in your financial obligations. As interest rates rise, the Bank of Canada has expressed growing concerns about Canada’s financial markets and the ability of households to service their debt. Mortgage holders, lenders, and the banking sector can expect to feel the impact.

We hope this article will act as a guide as we will explore the factors contributing to payment increases, the expected percentage of increase, and steps you can take to manage the potential payment shock. We’ll explore key insights from the Bank of Canada’s Financial System Review and other reliable sources to help you navigate this important financial decision.

Key Highlights

- The Bank of Canada is worried as mortgage holders face payment increases at renewal.

- Debt-service ratios, a measure of the percentage of household income allocated to debt payments, have been on the rise.

- By the end of 2026, all mortgage holders are expected to experience an increase in their payments.

- Payment increases at renewal are projected to be in the range of 20% to 40%.

Best Mortgage Rates

Bank of Canada More Worried Than Usual About Debt Repayments

The Bank of Canada’s Financial System Review highlights its concerns about household debt and the ability of borrowers to manage their financial obligations. With interest rates on the rise, the Bank is closely monitoring the impact on mortgage holders. The focus is ensuring households can continue to service their debt and avoid the impending financial stress.

Debt Service Ratios On The Rise

Debt service ratios (DSR) in mortgage lending are covered by gross debt service (GDS) and total debt service (TDS) ratios. These ratios measure the percentage of a household’s total income dedicated to mortgage payments and other debts – which have been increasing.

The median DSR on new mortgages rose from 16% to 19% in 2022, reaching the highest level in at least a decade. Additionally, the share of new mortgages with DSRs exceeding 25% jumped from 12% to 29%.

The Bank of Canada (BoC) asserts that higher DSRs reduce flexibility for borrowers, making it challenging to manage unforeseen expenses. Employment loss is one of the possible outcomes of a recession as the Bank of Canada continues hikes to its overnight rate in an effort to control inflation.

It is crucial for homeowners to carefully assess their financial situation before mortgage renewals and consider strategies to mitigate potential payment increases.

Up for renewal?

Download our report below to find out how rising rates can impact your renewal

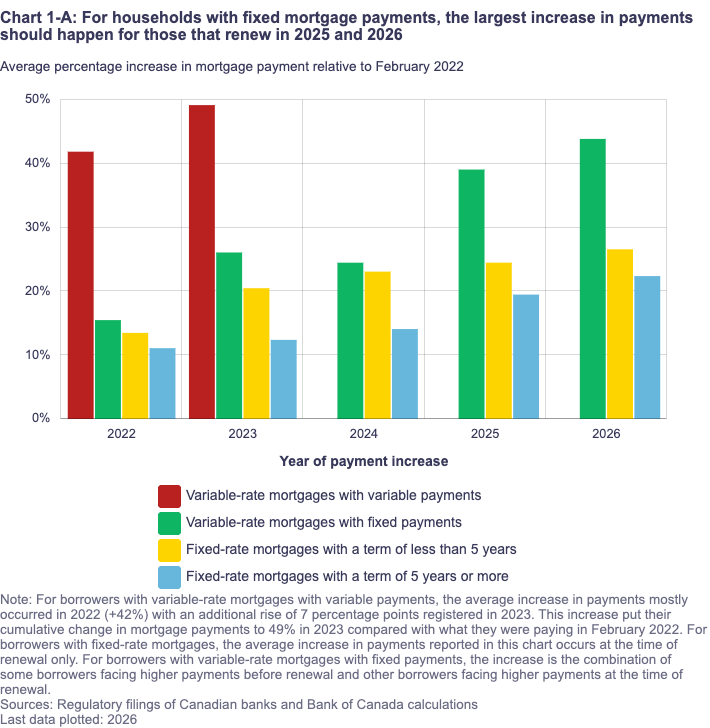

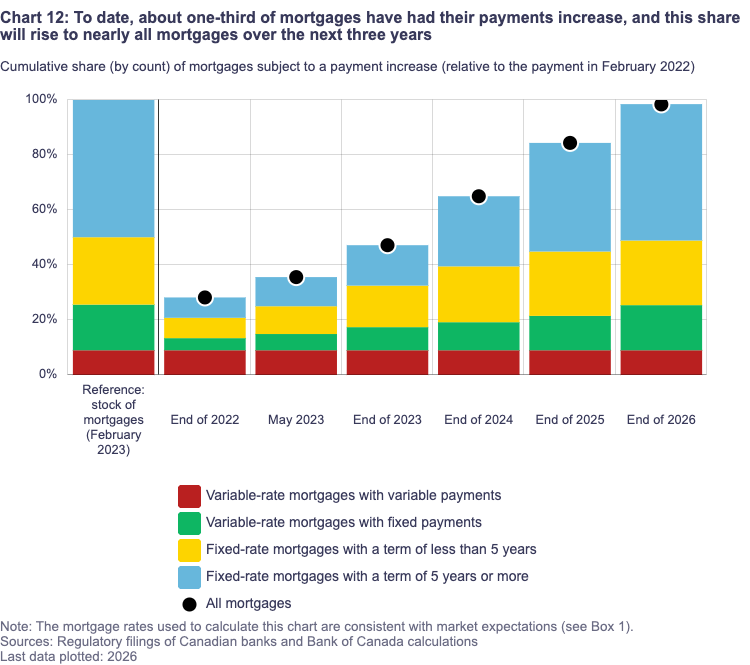

Every Mortgage Holder Will Be Paying More by 2026

According to the Bank of Canada, all mortgage holders are expected to experience an increase in their mortgage payments by the end of 2026. The size of the increase will depend on the type of mortgage and the previous interest rate obtained.

- Fixed-rate mortgages: Most will face renewal by or before 2026, with payment increases expected to be 20% to 25%.

Variable-rate mortgages: Adjustable-rate borrowers have already experienced payment increases, with some seeing their payments surge by more than 50%. Variable-rate mortgage borrowers with static monthly payments must increase their payments by an average of 40% to maintain their original amortization schedule.

20% to 40% Payment Increase Expected at Renewals

The Bank of Canada’s projections indicate that mortgage payments could increase by 20% to 40% at renewal. This increase results from higher interest rates, steadily rising due to the Bank’s efforts to combat inflation. Mortgage holders must be prepared for the potential impact on their monthly budgets.

Renewing a mortgage can come with a hefty price tag.

- Payment increases are expected to range from 20% to 40% for fixed- and variable-rate mortgage holders.

- This means homeowners previously paying $2,500 per month could see their payments rise to $3,000 or even $3,500 monthly.

It’s important to note that the exact payment increase will depend on the interest rate offered at renewal. For example, if the previous rate was 3%, the new rate might be 2 % higher, resulting in a significant payment increase.

Best Mortgage Rates

Financial Stresses Appearing

The impact of higher mortgage payments is already evident, with signs of financial stress emerging, particularly among recent homebuyers. The decline in house prices has reduced homeowner equity, adding to some borrowers’ financial pressure. The combination of higher debt-service ratios and lower home equity reduces household flexibility in the event of added financial stress, such as a reduction in income.

Managing Mortgage Renewals and Payment Increases

Renewing your mortgage and managing potential payment increases require careful consideration. Here are some strategies to help you navigate this process:

1. Start planning early

Begin preparing for your mortgage renewal well in advance to give yourself ample time to explore options, assess your financial situation, and make necessary adjustments. Review your current mortgage terms, including interest rates and payment schedules, and compare them to the rates offered by other lenders.

2. Assess your financial situation

Evaluate your financial health and determine how much of a payment increase you can afford. Consider your current income, expenses, and any other debts you may have. This assessment will help you gauge your financial capacity and inform your decision-making process.

3. Seek professional advice

Consult with mortgage professionals, such as brokers or financial advisors, who can provide expert guidance to tailor your financial plan to your needs. They can help you navigate the renewal process, explain various mortgage options, and assist in finding the best solution for your long-term financial goals and situation.

4. Consider refinancing

Refinancing your mortgage may be an option to explore if you anticipate challenges with payment increases. By refinancing, you can secure a lower interest rate or extend the amortization period, reducing your monthly payments. However, it’s essential to carefully evaluate the costs and benefits of refinancing before deciding.

5. Explore mortgage relief options

Financial institutions, including major Canadian banks such as CIBC, BMO, RBC, TD, Scotiabank, National Bank, and Desjardins, may offer mortgage relief options to help borrowers manage payment increases. Stay informed about the relief programs available and consider discussing potential solutions with your lender.

6. Shop around for the best rates

Take advantage of the competitive mortgage market by shopping for the best rates and terms. Online platforms such as nesto can help you compare multiple mortgage lenders and brokers and find the most suitable renewal options based on your needs. Lenders like nesto can also help you find the best rates without bundling your financial services.

7. Consider shorter-term mortgage options

Instead of opting for the popular 5-year term, consider shorter-term mortgage options. With a 1- to 3-year term, you can protect yourself from potential rate increases and take advantage of lower rates if the market shifts in your favour. However, remember that variable-rate mortgages still carry rate risks regardless of the term length.

8. Review your trigger rate

If you have a variable-rate mortgage, familiarize yourself with your trigger rate. This rate determines when your lender may contact you to discuss options if your monthly payments no longer cover the interest owed. Understanding your trigger rate can help you plan and make informed decisions about your mortgage.

9. Negotiate with your current lender

Before switching mortgage lenders, try negotiating with your current lender. Present your research on competitive rates and terms to see if they are willing to match or improve their renewal offer. Keep an open mind to discussing options that could reduce your payment increase.

10. Be proactive and stay informed

Stay proactive and informed about changes in the mortgage market, interest rates, and government regulations. Monitor your financial situation regularly and adjust your financial plans accordingly. Being proactive will help you make informed decisions and manage potential payment increases effectively.

Frequently Asked Questions

Welcome to our Frequently-Asked Questions (FAQ) section, where we answer the most popular questions designed and crafted by our in-house mortgage experts to help you make informed mortgage financing decisions.

Which mortgage holders are most affected by prime rate increases?

Prime rate increases impact all mortgage holders, but the specific effects will vary based on the type of mortgage and the interest rate at the start of the term. Fixed-rate mortgage holders will face higher payments at renewal, while variable-rate mortgage holders may have already experienced increased payments as interest rates have risen.

How much are mortgage payments expected to increase in Canada?

Mortgage payments are projected to increase by 20% to 40% at renewals, depending on the type of mortgage and the previous interest rate obtained. Fixed-rate mortgage holders can expect increases of 20% to 25%. In comparison, variable-rate mortgage holders with fixed monthly payments may need to increase their payments by an average of 40% to maintain their original amortization schedule.

What percentage of mortgages are being amortized negatively in Canada?

Around a quarter of Canadian mortgages are now negatively amortized. Negative amortization occurs when the monthly payment is insufficient to cover the interest owed, adding unpaid interest to the loan balance. However, borrowers must understand their specific mortgage terms and payment structures to avoid negative amortization.

Final Thoughts

As mortgage rates rise, mortgage renewals can significantly increase monthly payments. Borrowers must understand the potential impact on their finances and proactively manage their payment shock at renewal. Borrowers can confidently navigate the renewal process by knowing the projected payment increases, exploring different mortgage options, and seeking professional advice.

Remember, each lender may have unique offerings, so shopping around and comparing renewal offers can help you find the best solution for your financial needs. Be proactive, informed, and prepared to ensure a smooth transition and continued financial stability. Reach out to nesto’s mortgage experts to see how we can help you understand changes to your mortgage payment at renewal.