What Is A Home Equity Loan In Canada?

A home equity loan allows you to borrow money against the equity in your home. It can be a second mortgage, a loan, a line of credit, or a combination of secured lending products. It is often called and can be taken as a second mortgage. These secured credit facilities usually have lower interest rates than personally guaranteed, making them an attractive option for many homeowners.

We’ll cover home equity financing and how to use your home’s equity to finance home improvements and renovations, pay for post-secondary education, purchase an investment property or cottage and cover other large expenses.

Key Highlights

- A home equity loan is a type of secured debt, typically made up of hybrid mortgages and HELOCs.

- Home equity products are sold as part of a collateral charge mortgage.

- Home equity financing is less costly than unsecured credit.

Best Mortgage Rates

What Is A Home Equity Loan?

A home equity loan is a type of lending product that uses your home’s equity as collateral.

What is equity? Equity is the value or share of something owned by a person or a company. The best way to define the equity in a property or home is the difference between the value of your home and the amount of money you still owe to your mortgage lender(s). In other words, home equity is the value of your ownership stake.

Home equity products are used to access your home’s equity without having to sell your home. By completing an equity takeout (ETO) or refinancing your mortgage, you can set up a new mortgage, split up your mortgages, or set up a HELOC. These changes can make it easier to access your home equity now or in the future.

How Borrowing On Home Equity Works

Home equity financing is issued as term loans, mortgages or revolving lines of credit taken out against the value of your home, meaning that you can borrow up to the available equity in your home. A minimum of 20% equity must always be retained in your home.

Types of Home Equity Financing

There are several home equity loans available to homeowners. A home equity loan would only be considered a second mortgage if registered second rank, behind the first mortgage, although some lenders do not permit secondary financing. Depending on how the charge against the home’s title is registered, your home equity loan or line of credit (HELOC) may be part of your first mortgage if under a collateral charge.

Term Loans and Mortgages

Term loans or mortgages can be issued at fixed or variable rates and amortized over a suitable period to meet your needs. Term loans are typically unsecured (personal loans) or collateralized (car loans). Term loans are amortized over shorter periods, such as 60 or 96 months, whereas mortgages are amortized over longer periods, such as 25 or 30 years.

Term loans typically carry higher interest rates. However, they can be lowered if secured by your home’s equity. Conversely, if you have a larger term loan, such as one used to purchase a car or a mobile home, you could ask the lender to convert it to a mortgage instead. A mortgage makes payments more manageable by amortizing repayments over a longer period, and lenders can offer much lower rates than on a secured term loan.

Revolving Or Home Equity Line Of Credit (HELOC)

The equity in your home can be used to secure a home equity line of credit (HELOC) or a revolving line of credit. A revolving credit product will always come with a variable rate, whether secured or unsecured. The interest rate is a premium charged on your lender’s prime rate. It works like a credit card but without a physical card, allowing you to withdraw funds as needed.

Secured lines of credit can be used to cover significant expenses without incurring interest on unused balances. HELOCs are a great way to finance a project that may take time or has multiple vendors, such as home renovations.

Common Uses for Home Equity Financing

Home equity financing is a great way to access the equity built up in your home for various purposes. Common uses of home equity financing in Canada include debt consolidation, home renovation projects, borrowing to get ahead, education, and emergency expenses.

Debt Consolidation

Home equity financing can be a great way to pay off higher-interest debt, such as credit card debt, unsecured personal loans, and store cards, by consolidating it into a single payment. Before moving ahead with this solution, it’s best to discuss it with a mortgage expert and complete a cost analysis to ensure that it will save you time or money in the long run.

Home Renovations

Home equity financing is a great way to fund larger renovation projects, such as updating your kitchen or bathroom or adding an addition to your home. Typically, additional living space increases your property’s overall value.

Borrowing To Get Ahead

Regarding your investments, time is of the essence. Contributing to your RRSP before the end of February can save you from paying a hefty income tax bill. With a HELOC, you can use these time-saving options without visiting a bank to borrow money or emptying your chequing or savings account. Similarly, you can use your HELOC to apply a downpayment towards an investment property or for a deposit when your offer on a home is accepted. These are great ways to utilize approved low-interest credit for time-sensitive investment options.

Education Expenses

A home equity revolving line allows you to make timely payments for education expenses. Whether the education is for you, your spouse, or your child, the ability to make payments without consulting your bank is a significant advantage for those who proactively set up a line of credit secured by a collateral charge mortgage.

Emergency Expenses

Home equity financing can be used for unplanned emergencies through a HELOC. It can be used for unexpected bills, such as replacing a home appliance or repairing your car.

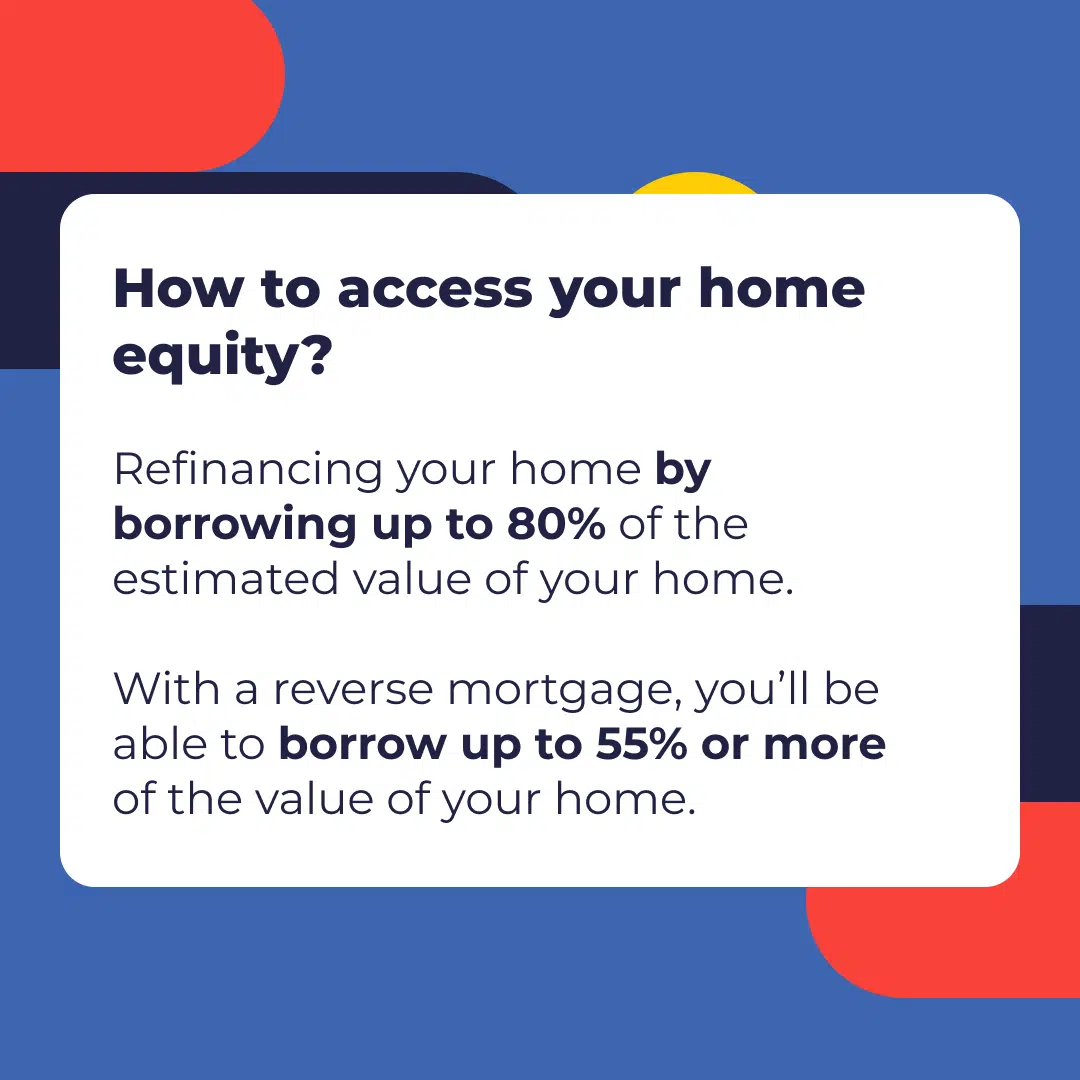

How To Access Your Home Equity

There are multiple ways to access your home’s equity – typically, they all involve refinancing your mortgage-free home or current mortgage.

Refinancing

One way to access your home’s equity is to refinance, borrowing up to 80% of your home’s estimated value. You’ll get a new mortgage agreement when you refinance your home or mortgage. A refinance can not only let you access your home’s equity by setting up a new mortgage or a HELOC, but it can also lower your monthly payments or interest. Your interest rate will depend on prevailing rates at the time and the specifics of your mortgage. However, lowering your interest rate or increasing the amortization period could lower your monthly payment.

Reverse Mortgage

A reverse mortgage is a loan program that allows homeowners aged 55 and older to convert a portion of their home’s equity into cash. With a reverse mortgage, you’ll be able to borrow up to 55% or more of the value of your home.

A reverse mortgage can provide a financial lifeline for senior homeowners who need additional funds to cover expenses, pay off debt, help children or grandchildren with a home purchase, or make home improvements. The best part is that you can retain the equity in your home without making payments on a reverse mortgage. No minimum credit score or repayment is required to qualify for a reverse mortgage.

Best Mortgage Rates

Requirements To Access Your Home Equity

Lenders will require a good credit score and sufficient income to cover the loan’s monthly payments, which are stress-tested on a 25-year amortization. You can understand more about your credit history by reviewing your credit accounts from one of Canada’s credit bureaus. Your ability to consistently make minimum payments on time will provide a better picture of your payment history and keep you within the credit score range lenders seek. You must retain a minimum equity in your home, typically around 20%, after your mortgage refinance is complete.

Learn more about nesto’s HELOC

How To Calculate Your Home Equity

Use our refinance calculator to determine your equity. First, establish the home’s current market value, then subtract the existing balance of your mortgage. You can understand the home’s value by looking at comparable house sales in your area. However, you’ll need a home appraisal to determine its market value.

A certified home appraiser provides an unbiased evaluation of your home based on its overall condition, size, neighbourhood, key features and amenities. Once this value has been confirmed, subtract your remaining mortgage balance to determine your equity. If you need clarification, your lender can provide you with the amount owing on your mortgage.

Borrowing against your home equity is a great way to access the equity you have built up. Let’s see an example of how much home equity you could access.

Home equity loans in Canada are typically limited to 80% of your home’s valuation, less any mortgage balance you owe to the lender.

For example, if the market value of your home is $400,000 and you still owe $200,000 on your current mortgage balance.

$400,000 x 0.80 = $320,000

$320,000 – $200,000 = $120,000

You can apply for a facility of up to $120,000. Depending on what type of facility you decide on, you will either get funds disbursed as a lump sum (term loan or mortgage) or set up a HELOC to access it over time. Use nesto’s refinance calculator to determine how much equity you can access from your home.

How To Build Home Equity

The equity in your home can increase in two ways simultaneously – as you pay down your mortgage and the home’s market value increases. Building home equity is a great way to increase your long-term financial security and wealth. Here are some tips to help you build home equity before applying for a home equity loan:

Location matters – Picking a location for your new home close to amenities can mean less time and money spent out shopping. This convenience frees up more time and money for home improvements. The amenities will also add value for homebuyers in your community.

Prepayments

Small and big prepayments reduce the principal and additional interest payments you’ll need to make to pay off your mortgage sooner. Paying down your mortgage sooner will increase your home’s equity.

Renovations and improvements

By paying off your mortgage sooner, you not only build equity in your home but also free up cash flow to direct toward renovations rather than paying down your mortgage. Renovations and improvements increase your home’s value.

Renting out a portion of your home – By renting out a portion of your home, you can apply the extra cash flow towards paying down your mortgage or improving/renovating portions of your home. Both of these options will increase your home’s equity.

Shopping around for the best rate – You could reduce your overall interest payments by completing a cost analysis each time your mortgage term finishes and comes up for renewal, or mortgage rates drop. You don’t have to stop at your mortgage. You could shop for other necessities to lower your monthly carrying costs. You might be able to switch your insurance, phone company, grocery store, or internet provider. Reducing your other obligations could free up extra cash to become mortgage-free faster.

While investing in home improvements is generally a good idea, its market value ultimately depends on several external factors. Housing demand, household debt, inflation and unemployment, among other things, all play a role in the economy’s overall health, which, in turn, impacts the state of the real estate market and, ultimately, your home’s value.

How To Qualify For A Home Equity Loan

Home equity loan requirements vary depending on the type of credit facility you choose. Your lender will assess the amount of available equity and evaluate your financial position based on your credit score and debt-to-income ratio (DTI).

Lenders set out different conditions to determine the amount they’ll lend to you. The maximum amount is up to 80% of your home’s value. To improve your chances of obtaining the maximum amount, should you need it, ensure that your credit score is high (680 or above) and that your gross debt service (GDS) ratio is below 35%.

Your lender will also assess your property’s loan-to-value ratio (LTV) to help determine the amount. LTV is calculated by dividing your home’s appraised or market value by your current mortgage balance. As a rule of thumb, your LTV should be 80% or less; if you only have a HELOC under your home equity plan, you’re limited to 75% LTV.

Frequently Asked Questions (FAQ) About Home Equity Loans in Canada

What is home equity?

Your home’s market value minus your mortgage balance equals your home equity. In other words, home equity is the value of your ownership stake.

How do you build home equity?

By making your monthly payments, you pay down the mortgage balance, thereby increasing your equity (the less you owe, the more equity you have). Your mortgage payments are applied to both the loan principal and interest. As the loan amount decreases, a larger portion of each payment will be applied to principal, and your equity will increase accordingly. Additionally, the increase in your home’s value also increases your equity.

What types of lenders offer home equity loans?

Several lenders offer Home equity loans, including banks, credit unions, virtual lenders, mortgage finance companies and mortgage brokers. Each will have different qualification requirements and terms and conditions, so you will need to shop around and compare features.

Does home equity hurt your credit?

Taking out a home equity loan or line of credit can positively or negatively impact your credit score, depending on how you use it. If you use the loan responsibly and make payments on time, you may see an increase in your credit score. If you choose a HELOC as your home equity credit facility, you must be careful not to exceed 33% of your limit. Taking out a term loan or a mortgage is best if you need to use the full amount.

Is a HELOC or a mortgage better for a home equity loan?

A HELOC is flexible and can be reused over time or used to make smaller payments on longer-term projects, such as home renovations. Mortgages are more suitable when you need a large sum of money simultaneously. Using your HELOC beyond 33% of its credit limit could negatively affect your credit score. With a mortgage, your credit score remains unaffected as long as you make payments on time.

Final thoughts

There is a need for intelligent decision-making when evaluating and leveraging home equity options. Evaluating a product’s pros and cons can help you make the most suitable choice for your unique needs. Whether it’s a hybrid mortgage or a HELOC, the right combination of these products can be beneficial. Additionally, paying down your mortgage or investing in renovations are great ways to increase your home’s equity.

Reach out to our nesto mortgage experts to find the most suitable mortgage strategy for you.

Why Choose nesto

At nesto, our commission-free mortgage experts, certified in multiple provinces, provide exceptional advice and service that exceeds industry standards. Our mortgage experts are salaried employees who provide impartial guidance on mortgage options tailored to your needs and are evaluated based on client satisfaction and the quality of their advice. nesto aims to transform the mortgage industry by providing honest advice and competitive rates through a 100% digital, transparent, and seamless process.

nesto is on a mission to offer a positive, empowering and transparent property financing experience – simplified from start to finish.

Contact our licensed and knowledgeable mortgage experts to find your best mortgage rate in Canada.