Income Needed to Buy a Home in Quebec

Mortgage affordability in Quebec is influenced by more than just where you purchase your home or your mortgage payment. Lenders approve mortgages based on income, mortgage amount, downpayment, and debt service limits, not simply the home price or advertised rate. That means two buyers in the same city can face very different income requirements depending on the size of the mortgage they need.

We’ll explain how mortgage qualification works in Quebec and show how income requirements vary by region. We use updated home prices monthly, based on the latest data from CREA, QPAREB, and Centris, to qualify under nesto’s dynamic mortgage rates.

Key Takeaways

- Mortgage approval in Quebec is based on qualifying income, with mortgage payments calculated at stress tested rates for home purchases throughout the province.

- The income required to qualify for the same mortgage amount can vary by municipality or region due to property taxes and differences in home prices.

- Downpayment amount and mortgage insurability can materially change approval outcomes for the same loan amount.

Best Mortgage Rates

Qualifying for a Mortgage in Quebec

Details

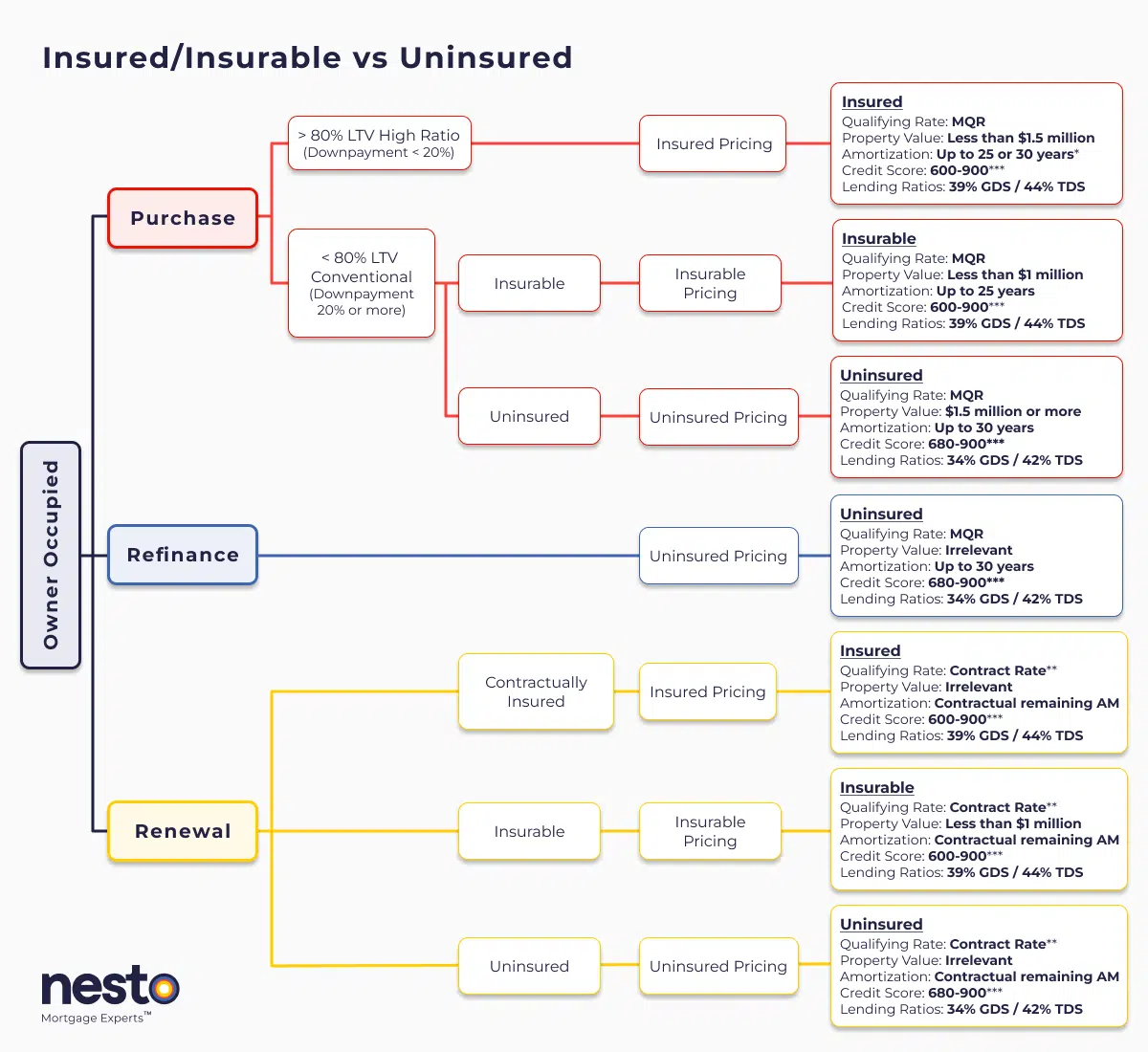

*30-year amortizations on insured purchases are limited to first-time homebuyers (FTHBs) or anyone purchasing newly built homes.

**Qualified at contract rate at renewal only if there are no increases to contractually remaining amortization or remaining balance, and the mortgage is being transferred from a federally regulated lender as outlined by the Department of Finance (DOF) as a straight switch. The Minimum Qualifying Rate (MQR) requirements have been amended by the Office of the Superintendent for Financial Institutions (OSFI). It will be used to qualify all mortgages used for purchases and refinances. The MQR does not apply to renewals if the mortgage is renewed with the current lender or switched from a federally regulated lender.

***A credit score of 600 or 650 is allowable based on the mortgage insurer, and if there is a secondary applicant with a credit score of 680 or above. Lenders may scale debt service ratios (GDS/TDS) based on applicant(s) credit score(s) or reason for purchase/renewal (primary residence vs rental property). If one applicant on a joint mortgage has a credit score below 680, the lender may apply lending ratios as low as 32% GDS and 40% TDS. All criteria in the chart above apply to an owner-occupied primary residence mortgage with nesto.

Contractually insured mortgages are initially mortgage default insured by the borrower at the time of purchase and have not been refinanced or changed in any way that increases their remaining contractual amortization or mortgage balance. These insured mortgages are also known as high-ratio mortgages. In contrast, insurable and uninsured terms apply to conventional mortgages that are back-end bulk portfolio insured (typically lender-paid) or not.

New Purchase Qualifying Rates

Insured home purchases may be qualified using our lowest fixed rate, which will be the greater of 5.25% or 6.04%.

Insured home purchases may be qualified using our lowest variable rate, which will be the greater of 5.25% or 5.40%.

Insurable home purchases may be qualified using our lowest fixed rate, which will be the greater of 5.25% or 6.09%.

Insurable home purchases may be qualified using our lowest variable rate, which will be the greater of 5.25% or 5.40%.

Uninsured home purchases may be qualified using our lowest fixed rate, which will be the greater of 5.25% or 6.44%.

Uninsured home purchases may be qualified using our lowest variable rate, which will the greater of 5.25% or 5.85%.

Renewal (Switch or Transfer) Qualifying Rates

An insured mortgage may be qualified for renewal using the contract rate, which could be on our lowest fixed or variable insured rates, currently at 4.04% and 3.40%, respectively.

An insurable mortgage may be qualified for renewal using the contract rate, which could be on our lowest fixed or variable insurable rates, currently at 4.09% and 3.40%, respectively.

An uninsured mortgage may be qualified for renewal using the contract rate, which could be on our lowest fixed or variable uninsured rates, currently at 4.44% and 3.85%, respectively.

How Mortgage Qualification Works in Quebec

All new mortgages for purchases and refinances in Quebec must pass the federal mortgage stress test. Borrowers are qualified at the minimum qualifying rate (MQR), which is the higher of 5.25% (the federal benchmark rate) or their contract rate plus 2%, regardless of whether they choose a fixed or variable mortgage. The MQR is used solely for mortgage approval and does not reflect the contract interest rate used to calculate the borrower’s actual monthly payments.

Lenders then apply gross and total debt service ratios, which measure how housing costs and total monthly debts compare to household income. These debt service ratios tighten or loosen depending on whether a mortgage is insured, insurable, or uninsured.

| Transaction Type & Limitation | Minimum GDS | Minimum TDS |

|---|---|---|

| Credit score (FICO) for the lowest-score borrower (between 650 and 680) | 32 | 40 |

| Uninsured refinance or uninsured purchase of a property valued at $1.5 million or more | 35 | 42 |

| Insured purchase with a down payment of less than 20% (also applies to insurable mortgages for new purchases and renewals) | 39 | 44 |

Insured, Insurable, and Uninsured Mortgages in Quebec

Mortgage structure, specifically the loan-to-value (LTV) ratio, expressed as the borrower’s downpayment compared to the mortgage amount they need, plays a major role in affordability.

Insured mortgages, with downpayments under 20%, allow higher qualifying ratios and often support higher approvals at the same income level. Insurable mortgages meet insurer standards with a 20% downpayment and can still be more cost-effective with more flexible LTV ratios, but are limited to properties priced below $1M.

Uninsured mortgages avoid insurance premiums but are subject to tighter ratio limits. In Quebec, mortgage default insurance premiums are subject to the QST provincial sales tax, which must be paid upfront and cannot be added to the mortgage balance, affecting the total required for closing costs.

Mortgage Default Insurance Requirements

Mortgage default insurance is mandatory for downpayments under 20%, impacting your mortgage qualifying amount and monthly costs. Default insurance often applies to higher-LTV loans, making high-ratio mortgages more affordable. Due to limitations on amortization periods, these mortgages require a smaller downpayment despite having a higher monthly payment.

| Loan-to-Value | Premium (25-year Amortization) | Premium (30-year amortization) |

|---|---|---|

| 80.01% to 85% | 2.80% | 3.00% |

| 85.01% to 90% | 3.10% | 3.30% |

| 90.01% to 95% | 4.00% | 4.20% |

Quebec Housing Affordability Snapshot

The average home price in Quebec is currently $547,800. Based on lender qualifying rules, the income needed to buy an average-priced home in the province ranges from $93,854 to $112,378, depending on mortgage structure and downpayment.

Monthly mortgage payments for an average-priced Quebec home range between $2,055 and $2,644, reflecting insured, insurable, and uninsured options.

Income Needed for Common Mortgage Amounts in Quebec

Looking at affordability by mortgage balance helps answer some of the most common borrower questions more directly.

The qualifying income for each $100,000 mortgage balance in Quebec typically ranges from $23,478 to $29,325, making the mortgage balance as important as location when assessing affordability.

For example, the qualifying income required for a $200,000 mortgage in Quebec depends on the mortgage type and amortization period. Under today’s stress test assumptions, required income for a $200,000 mortgage in Quebec ranges between $43,878 and $55,221, depending on whether the mortgage is insured, insurable, or uninsured.

For a $700,000 mortgage, qualifying monthly payments under the stress test range between $4,570 and $3,865, depending on insurability and amortization.

Income Needed Across Québec Cities and Regions

Mortgage rules are applied consistently across Quebec, but prices and property taxes vary by region, which affects income requirements even for the same mortgage size.

Income Needed to Buy an Average-Priced Home in Québec

| Region | Average Home Price | Lowest Income Needed | Highest Income Needed |

|---|---|---|---|

| Montreal | $594,200 | $104,438 | $124,832 |

| Québec City | $445,400 | $78,484 | $93,794 |

| Gatineau | $493,648 | $85,134 | $101,890 |

| Sherbrooke | $545,255 | $94,132 | $112,651 |

| Saguenay | $362,815 | $67,014 | $79,837 |

| Trois-Rivières | $444,910 | $79,200 | $94,584 |

| Mauricie | $324,600 | $59,198 | $70,583 |

| Estrie | $476,600 | $87,799 | $104,618 |

| Centre-du-Québec | $342,900 | $59,812 | $71,528 |

How Downpayment Scenarios Affect Mortgage Amounts in Quebec

Downpayment choices directly determine how much you need to borrow; higher downpayments reduce the mortgage amount, while lower downpayments increase leverage and default insurance requirements across Quebec.

Home Financing Scenarios Affecting Downpayment and Mortgage Amounts

| Scenario | Downpayment Needed | Mortgage Needed |

|---|---|---|

| Minimum Downpayment | $29,780 | $518,020 |

| 10% Downpayment | $54,780 | $493,020 |

| 20% Downpayment | $109,560 | $438,240 |

We’re curious…

Are you a first-time buyer?

Frequently Asked Questions (FAQ) About Mortgage Affordability in Quebec

Can I afford a mortgage with student loans in Quebec?

Student loans are included in total debt service calculations. Required monthly payments reduce the mortgage amount you can qualify for, particularly for uninsured mortgages with tighter ratio limits. Typically, each $100 increase in monthly car or student loan payments reduces the qualifying mortgage amount by approximately $20,00

How does the mortgage stress test work in Quebec?

Borrowers must qualify at the minimum qualifying rate (MQR), which is the higher of 5.25% or their contract rate plus 2%. The qualifying rate is used only for mortgage approval of home purchases and refinances, not to calculate the actual monthly payment borrowers can expect to pay.

How much house can I afford on a $100k salary in Quebec?

Affordability depends on the mortgage amount, downpayment, and other debts. In lower-priced regions, a $100k income may support a larger purchase, but approval is always based on stress-tested ratios.

For example, the income requirement to qualify for a $100,000 mortgage balance typically ranges from $23,478 to $29,325. You can use this as a factor to assess how much you’ll qualify for a $100,000 income.

How much income do I need for a $300k mortgage in Quebec?

Under current stress-test rules, the qualifying income for a $300k mortgage ranges from $64,279 to $81,118, depending on the mortgage type and amortization. Typically, you’ll need slightly less income to qualify for a $300K mortgage in Quebec, as the above figures are based on Canada’s 1% average property tax rates, while Quebec has an average property tax rate as low as 0.71%.

How much mortgage can I afford with 20% down in Quebec?

A 20% downpayment reduces the loan size and avoids insurance premiums, but if it is an uninsured mortgage, then it’ll face tighter debt service limits, which can reduce maximum approval amounts.

Typically, you’ll qualify for a mortgage amount of 4 to 5 times your household income. Based on Quebec’s average home price of $547,800 currently, a 20% downpayment would set you back $109,560, and you’ll need to qualify for a mortgage balance of $438,240 if you’d like to buy the average-priced home in the province.

Final Thoughts

Mortgage affordability in Quebec depends on more than home prices or interest rates alone. Lenders’ approvals for mortgages are shaped by how income, mortgage balance, downpayment structure, and regional costs work together under stress-test rules. Looking only at home prices or interest rates can give an incomplete picture, while comparing affordability by both location and mortgage amount helps clarify what lenders will realistically approve.

Understanding these mechanics puts borrowers in a stronger position to make suitable choices. Small adjustments can meaningfully affect qualifying income and long-term affordability. Changing the downpayment approach, selecting a different amortization, or structuring the mortgage more efficiently can help you qualify for your home. These decisions are rarely one-size-fits-all and should reflect your full financial situation, not just the purchase price.

Working with a mortgage expert helps translate this practical, clear information so you can move forward confidently with a mortgage strategy tailored to your financial circumstances. Reach out and nesto mortgage experts will take the time to understand your goals and structure a mortgage that fits your needs and Quebec’s lending environment.

Why Choose nesto

At nesto, our commission-free mortgage experts, certified in multiple provinces, provide exceptional advice and service that exceeds industry standards. Our mortgage experts are salaried employees who provide impartial guidance on mortgage options tailored to your needs and are evaluated based on client satisfaction and the quality of their advice. nesto aims to transform the mortgage industry by providing honest advice and competitive rates through a 100% digital, transparent, and seamless process.

nesto is on a mission to offer a positive, empowering and transparent property financing experience – simplified from start to finish.

Contact our licensed and knowledgeable mortgage experts to find your best mortgage rate in Canada.

Ready to get started?

In just a few clicks, you can see our current rates. Then apply for your mortgage online in minutes!